Given China’s global importance, the event will be closely monitored by both domestic and global audiences looking for, among other things, clarity on leadership changes, the CCP’s view on the current domestic and international economic environment, COVID management, global tensions (including Russia’s invasion of Ukraine), and long-term CCP policy direction.

What is the National Congress?

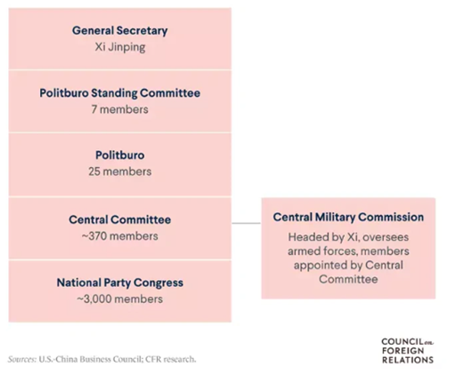

The National Congress is an assembly held by the CCP every five years. The meeting draws together close to 2,300 selected CCP delegates representing the Party’s estimated 90 million members. The delegates include incumbent top CCP leaders, cabinet ministers, senior military generals and so-called ‘grassroots’ representatives (such as workers, scientists, entrepreneurs and farmers). Attendees are required to elect candidates to senior party positions, consider the General Secretary’s report (a report on the execution of policies since the last Congress, and an outline of party priorities for the next five years) and decide on potential amendments to the CCP’s constitution. While there is no concrete timeframe, the meeting typically lasts about a week.

Key agenda items for the 20th Congress

Critical party positions decided

The Party’s general secretary, premier and military commission appointees are all decided during the Congress. Additionally, delegates will elect members to the Central Committee, a body composed of the top decision-makers in the Party, state, and society. The Committee is then tasked with appointing members to the 25-member Politburo, the top leadership body of the CCP. The Politburo then decides on membership of the seven-member Politburo Standing Committee (PSC), the Party apex, which is mandated to conduct policy discussions and make decisions on major issues when not in session.

Chinese leader, President Xi Jinping, to face re-election

Mr Xi is looking for an unprecedented third term as leader, and is widely expected to be re-elected. As he is 69 years old, a third term would break the unwritten ‘seven up, eight down’ rule; those aged 67 or younger are eligible for another term, while those 68 and above are expected to step down. A further provisional rule stipulates officials should stay no longer than two five-year terms in a single position; however, this does not apply to the position of president.

Speculation is also high as to who will be appointed to China’s other top governing roles, as thirteen members of the Politburo (including four within the PSC) will be aged 68 and over at the opening of the Congress. This should provide some crucial insight into Mr Xi’s ultimate successor.

COVID policy to be reviewed

China has maintained the world’s most draconian COVID containment measures – a clear outlier as the rest of the world shifts from pandemic to endemic. While China has one of the lowest virus-related death tolls globally, its commitment to its ‘Zero-COVID’ policy has hindered the domestic economy and caused significant global supply chain disruptions.

COVID strategy dynamics will be watched closely at the Congress, as the easing of restrictions represents a major catalyst for global markets and, importantly for us, listed infrastructure names. While we do not anticipate the Zero-COVID policy to be abandoned during the Congress, we will be looking for signposts that may stipulate a more pragmatic COVID management strategy going forward. These could either be direct, such as reducing mandatory quarantine times, or indirect, through the CCP’s approach to vaccination distribution and other treatment methods, addressing low vaccination rates among the elderly population, improving public health infrastructure or shifting its stance on city lockdowns.

Chinese economy to be reviewed

At the start of this year, officials had set an ambitious target of ‘around 5.5%’ GDP growth. For the first half of the year, the economy grew just 2.5%, having navigated headwinds in the form of COVID, droughts, a deteriorating property market and global economic pressures. The Central Government responded by employing targeted policy tools to stimulate the economy and support vulnerable businesses and people. In May, Bloomberg estimated that China’s total pledged stimulus for 2022 had amounted to RMB35.5 trillion (US$5.3 trillion). Similar measures saw China maintain positive GDP growth in both 2020 and 2021 of 2.3% and 8.1% respectively. However, in July, officials abandoned the growth target, saying instead it would ‘strive to achieve the best results possible’.

The Congress will thoroughly examine the current international and domestic situation, and formulate action plans and fundamental policies to rejuvenate economic growth. This should see more aggressive stimulus, and initiatives to streamline investment and promote consumption.

Benefits for infrastructure development

Throughout the year, a series of stimulus measures have been announced in an attempt to mitigate domestic and global challenges. While measures vary, the mainstays have been fiscal policies boosting infrastructure investment and other initiatives, such as enabling a less obstructed/accelerated path from planning through to procurement.

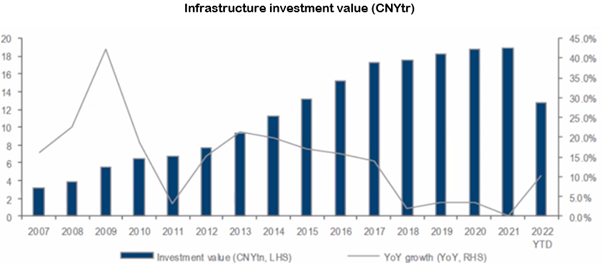

The Central Government has announced more than CNY1.1 trillion (US$140 billion) of financial support to boost infrastructure investment this year. According to the National Bureau of Statistics (NBS), China’s infrastructure investment increased by 8.3% year-on-year from January to August. Along with policy incentives, strong financial support and sufficient project reserves, the growth rate is forecast to accelerate further and grow by 10% to 15% for the full year of 2022. Given infrastructure investment typically accounts for about 15% of China’s GDP, economists anticipate infrastructure investment could drive 1.5%-2% of real GDP growth.

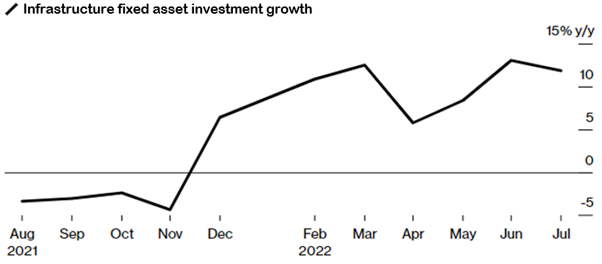

Source: Daiwa. China’s Infrastructure investment growth is predicted to be 12-13% for full-year 2022 based on fiscal support and pro-infrastructure investment measures

Source: Goldman Sachs Group. China's infrastructure investment has accelerated significantly over the past 12 months amid strong policy support and reliance on the sector for economic support

We view stimulus and policies supporting infrastructure investment as tailwinds for the listed sector. These will provide new development opportunities, accelerate the planning/construction of existing projects and facilitate access to lower-cost funding. There are also other indirect benefits, such as stronger network integration and improved logistics chains supporting efficiencies. While the immediate focus of the infrastructure investment push is to provide short-term support to the economy, over the longer term the investment contributes towards China’s ambition of becoming a more urbanised, high-income economy. This, in turn, is expected to boost consumption and fuel more significant investment in infrastructure.

Conclusion

The upcoming 20th National Congress meeting will see the formulation of action plans and fundamental policies. We don’t anticipate any significant shift in policy dynamics, but view policy direction as critical for setting the tone for economic recovery and guiding market expectations. Any key policy decisions made likely won’t be formalised until the ‘Two Sessions’ annual parliamentary meeting that typically takes place in early March. However, confirmation of personnel, including the likely re-election of President Xi Jinping, should lead to some clarity, better policy coordination and more efficient implementation.

We expect support for infrastructure will be reiterated as both a near-term stimulus measure and a long-term structural thematic. Investments in transportation, logistics, communications, utility systems and public facilities play a vital role in improving living standards and stimulating domestic demand. We continue to see this as an exciting investment opportunity.

The content contained in this article represents the opinions of the authors. This commentary in no way constitutes a solicitation of business or investment advice. It is intended solely as an avenue for the authors to express their personal views on investing and for the entertainment of the reader.