Focus on community engagement – AEP Headquarter, Ohio. Source: 4D Infrastructure

Atmos Energy gas distribution training centre - Plano, Texas. Source: 4D Infrastructure

1. Trip agenda

|

Company |

Sector/Topic |

Location |

|

Black Hills Energy |

Integrated Utility |

New York City, NY |

|

Consolidated Edison |

Integrated Utility |

New York City, NY |

|

Eversource Energy |

Integrated Utility |

New York City, NY |

|

Entergy Corp |

Integrated Utility |

New York City, NY |

|

One Gas |

Gas Utility |

New York City, NY |

|

PG&E Corp |

Integrated Utility |

New York City, NY |

|

Pinnacle West Capital |

Integrated Utility |

New York City, NY |

|

Public Service Enterprise Group |

Integrated Utility |

New York City, NY |

|

CMS Energy |

Integrated Utility |

New York City, NY |

|

Duke Energy |

Integrated Utility |

New York City, NY |

|

Excelon Energy |

Integrated Utility |

New York City, NY |

|

NextEra Energy |

Integrated Utility |

New York City, NY |

|

National Grid |

Transmission/Distribution |

New York City, NY |

|

Plains All American |

Midstream oil & gas |

New York City, NY |

|

First Energy |

Electricity Transmission/Distribution |

Akron, OH |

|

American Electric Power (AEP) |

Integrated Utility |

Columbus, OH |

|

Southern Company |

Integrated Utility |

Atlanta, GA |

|

Oneok |

Midstream oil & gas |

Tulsa, OK |

|

Williams Co |

Midstream oil & gas |

Tulsa, OK |

|

Atmos Energy |

Gas Utility |

Plano, TX |

|

Targa Resources |

Midstream oil & gas |

Houston, TX |

|

Kinder Morgan |

Midstream oil & gas |

Houston, TX |

2. Introduction

In late February / early March 2020, 4D Infrastructure (4D) Senior Investment Analyst, Peter Aquilina, travelled to the US to meet with Utility and Midstream Oil & Gas management teams in 4D’s investment universe. Peter spent the majority of the first week abroad meeting utility management teams in New York (attending the Morgan Stanley Energy and Utility Conference); the Mid West; and Atlanta, GA.

The second week of the trip was spent in Oklahoma and Texas meeting midstream management teams. These meetings coincided with the novel coronavirus (COVID-19) influenced dispute between OPEC and OPEC+ countries which saw global oil and gas prices plunge, pushing equity markets lower, with midstream companies’ share prices particularly punished. We give credit to the companies for meeting with us during this very difficult time. We subsequently published a Global Matters article The impact of the oil shock on North American midstream assets, which addressed this event. As such, this piece won’t focus on the oil price dynamics that played out.

Companies from across the US attended the Morgan Stanley Global Energy and Power Conference in New York, with only a couple of late withdrawals as a result of travel fears associated with COVID-19 – which in hindsight was a wise decision, as it seems the virus was much more prevalent in the US at the time than information sources were indicating. While attending the conference, Peter met with 13 utility companies and a midstream oil & gas company. During the remainder of the trip Peter met with an additional four utility companies. The key themes discussed by utility management teams and conference attendees focused on:

- Environmental, Social, and Governance (ESG) – primarily efforts to transition to a carbon free economy;

- Bills and customer satisfaction – defining regulatory relationships; and

- Democratic primary elections – views of various Democrat candidates and what ramifications their election could have for the Energy industry.

3. ESG

Standard charging station at shopping centre - Atlanta, Georgia. Source: 4D Infrastructure

Utilities are considered central to achieving the global target of restricting global temperature rises to ‘well below 2 degrees Celsius above pre-industrial levels’ and to pursue efforts to limit the temperature increase even further to 1.5 degrees Celsius in line with the Paris Climate Agreement. As such, there is considerable focus of investors on the ‘E’ component of the ESG principles in relation to utilities investment.

Utility management teams highlighted that it seems the focus of investors on ESG issues had intensified over the past 6-12 months, exemplified by the announcement by BlackRock in January 2020 of its intention to place sustainability at the centre of its investment approach. In response, nearly all the utilities spoken to indicated that while ESG had always been part of management responsibilities, they had stepped up their ESG efforts over the past 12 months, especially with regard to the environment, including:

- adopting more ambitious environmental targets;

- increasing transparency/reporting of actual environmental measures; and/or

- elevating strategic oversight and monitoring of ESG issues to executive management and Boards.

The generation of electricity contributes approximately 33% of carbon emissions in the US. It is widely understood that in order to achieve the Paris Agreement’s goal of limiting global temperature increases to 2 degrees Celsius or less, generation of electricity must be carbon neutral by 2050 – that is, any small proportional amount of carbon released in generation needs to be offset or captured. One thing nearly all utility management teams admitted is that this challenge of carbon neutrality cannot be practicably met with the cost and capability of technology as it is today. In other words, companies must assume some improvement in technology AND a lowering in its cost to feasibly implement carbon neutrality by 2050, while ensuring electricity affordability for customers and a reasonable return for shareholders.

The required advance in technology predominantly relates to battery technology, as this is instrumental in solving the intermittency of renewable generation but is currently too expensive to implement at scale and doesn’t provide sufficient longevity of energy storage. That is, there is both a financial issue and a capability issue with the current technological solution.

Different utility companies have responded to this challenge in different ways, including:

- State level mandates: Some utilities that operate in states which have legislated carbon reduction targets are at a minimum required to adopt the carbon reduction mandate of the state. To some degree this takes the difficult economic decisions away from the utility management teams. This is the case for companies such as Edison International in California which is required to achieve carbon neutrality by 2045; and Eversource, based in Massachusetts, which is required to achieve carbon neutrality by 2050 (state target) but has actually committed as a company to outperform this and achieve the goal by 2030. The company hasn’t provided full costing as to how they will deliver net neutrality in the coming decade, but their plan incorporates offshore wind generation, solar generation, energy efficiency measures, investment in significant battery/storage capacity and implementation of Electric Vehicle (EV) charging infrastructure. While companies in this category are currently able to take steps to transition to carbon neutrality without disrupting reliability or excessively inflating customer bills, this will be tested as the obvious sources of carbon reduction subside. At this point the state’s legislated carbon mandate still needs to be met, and without improvements in technology there may need to be a trade-off by increasing customer bills significantly.

- Comfortable in committing to the Paris Accord: Certain utility management teams are comfortable that the trajectory of development in battery storage and other types of technology is such that as and when it is needed, it will be capable of removing the intermittency of renewable generation sources at a reasonable cost in order for them to achieve carbon neutrality. These companies are potentially more accustomed to the technology, like NextEra Energy, or are generally just more inclined to adopt the aspirational target as a signal of intention, rather than an actual visible plan of carbon transition. For example, CMS Energy stated this was its intention in adopting the carbon neutrality target by 2040, even though it only has detailed generation transition plans out to 2035 as outlined in its Integrated Resource Plan (IRP) approved by the regulator in Michigan. Without a detailed plan there is obviously a greater risk of failing to achieve the carbon neutrality, and this can only be assessed closer to the targeted date. The counter argument to this approach is that current management teams are unlikely to be around to be held responsible for achievement (or not) of the target.

- Committing to what is visibly achievable: Other utility management teams such as Southern Company, American Electric Power (AEP) and First Energy also have ambitious carbon reduction targets, but are concerned in committing to what they call ‘the last mile’ of carbon transition. This usually represents moving from an 80-90% reduction in carbon emissions relative to pre-industrial levels (usually 2005 levels), to carbon neutrality. Their concern is that the requirement for additional battery capacity or less proven carbon capture technology to facilitate the transition to neutrality would be too risky/expensive to implement, and/or would result in poor reliability of service due to an excessive reliance of intermittent renewable generation. They are increasingly being pressured to adopt a carbon neutrality target by the investment community and other stakeholders because of the commitment being made by other companies. The support of regulatory bodies for required investment is obviously a major consideration in making and delivering upon commitments.

What is clear from all the discussions had with the utilities is that the ‘E’ in ESG is becoming increasingly important. Challenging targets are in place (carbon neutrality) towards which all the utilities are in some way moving, which 4D views as very positive. Success (or not) will be dependent on technological advancements, technological cost reductions and management execution (look for the quality companies). What is also clear, however, is that this success cannot be viably measured until we are a lot closer to specified neutrality deadlines (minimum 10 years away).

4. Bills and customer satisfaction – the cornerstones of regulatory relationships

Another theme that was widely addressed by the management teams of utility companies in meetings was the need to get the operational and regulatory framework right. This requires companies to balance customer bills (bills are kept affordable, which usually means increases are kept below inflation or 2-3%) with customer satisfaction (are customers satisfied with the service they receive from the utility company). Importantly, customer satisfaction is often heavily influenced by the reliability of service, and more recently the carbon reduction achievements of the utility. Both of these are influenced by utilities’ investment programs, which need to incorporate sufficient mechanisms to efficiently recover costs and earn the utility a sufficient return on investment.

These factors are determined by the regulatory bodies in various states – so both the utility and the regulator need to play their part in ensuring a positive, affordable experience for the customer. This is based on a shared vision of customer service; trust established by a long track record of service and operational capability by the utility; and significant evidence of bottom-up, least cost analysis determining best solutions for customers. This is obviously a time-consuming process for management, but is central to winning the support of regulators in delivering projects for the benefit of customers. Importantly, a number of utilities outlined that they had successfully lobbied for improved regulatory mechanisms or outcomes, such as:

- First Energy was allowed to decouple rates and revenues in Ohio, removing volume volatility related risk;

- AEP successfully lobbied the Oklahoma Corporation Commission (OCC) for investment trackers to improve recoupment of investment in the state and reduce regulatory lag;

- Southern Company outlined that it was able to discuss outstanding issues with the Georgia Public Service Commission (GPSC) to achieve a constructive regulatory outcome in its most recent rate case in December 2019. This included sensitive issues such as nuclear construction recovery tariffs, after failing to come to a settlement with the regulatory staff; and

- Atmos Energy continues to efficiently recover investment in replacing old/deteriorated gas pipes and earns strong regulatory ROEs across jurisdictions with minimum lag in recovery.

There are obviously examples where utility companies have not received constructive regulatory outcomes, or are experiencing difficult regulatory environments – mainly because the utility-regulator relationship has been violated or broken down due to particular events or poor working relationships. Some examples include:

- Consolidated Edison (ConEd) recently agreed a settlement with regulatory staff on an allowed ROE of 8.8% and equity ratio of 48%. This is the lowest return allowance in the US, and some 60bps below the average. Historically, regulatory incentives assisted the company in achieving more reasonable returns, although the incentive thresholds are seen as much more challenging this time around. Management outlined that the regulatory/legislative environment was becoming more punitive in the state of New York, and regulatory/legislative relationships had been strained in part as a result of electric power outages and perceived safety failures as a gas operator in the state;

- Pinnacle Northwest (PNW) has struggled with its regulatory relationship in Arizona based on political lobbying by the company, and reports of poor customer satisfaction. After a number of poor regulatory outcomes and penalties, the company has reshaped its executive management team, and is making steps to repair the regulatory relationship; and

- Duke Energy has historically had a strong relationship with regulatory bodies in the Carolinas – for example, the company has been allowed to earn an equity return on coal ash remediation costs and recover those costs over a relatively short period. These costs have since increased in quantum, putting upwards pressure on customer bills. There are also new commissioners on the North Carolina Utilities Commission (NCUC), which may take a different view on recovery. The NCUC recently rejected Dominion’s ability to earn a return on these same costs, and there are investor fears this may also apply to Duke at its next rate case.

5. Democratic primary elections

As at the time of the conference, there were seven Democrat candidates still in the race for nomination. Of these, the most likely candidates to win were the more left-leaning Bernie Sanders, and a more central, moderate candidate in Joe Biden. It was very early in the process, but already the investment community and utility companies were trying to figure out what influence the mandates of these candidates would have on the operations, strategy, and investment returns of utility companies in general, and their business in particular; and whether any of them would have the popularity to beat sitting President Trump at the November 2020 elections.

Varying mandates of the Democratic candidates

Sanders has adopted an aggressive climate carbon transition strategy, while Biden’s is more moderate. Sanders’ strategy includes the following proposals.

- Sanders has adopted a ‘Green New Deal’, which proposes spending $16.3 trillion to transition to a carbon neutral society by 2030 while supporting displaced workers from traditional carbon intensive generation sources.

- Nuclear and natural gas are off the table, as is carbon capture. Sanders has called for an end to new nuclear approvals or license renewals until a reasonable solution is found for nuclear waste. In February 2020, he also introduced legislation to ban fracking (the main method to drill natural gas in the US) by blocking federal permits for infrastructure.

- Quite radically, Sanders called for criminal prosecution on fossil fuel companies and their leaders – although it’s thought that even a Sanders-led government would not get the required votes for such drastic legislation.

- To have the climate strategy passed through the Houses, Sanders wants to reform rather than eliminate the filibuster regime. Filibuster is the Senate process of continually talking (sometimes meaninglessly) and blocking debate on legislation to be passed unless affirmative votes representing 60% are received to ‘bust’ the filibuster and allow the debate/vote.

In contrast to the above, Biden proposes spending US$1.7 trillion and achieving carbon neutrality in the US by 2050. He believes there is a role to play for natural gas as a transitional fuel source and refused to declare a ban on fracking. He supports innovation in nuclear power, and therefore sees a role for it in providing carbon-free power (currently nuclear power constitutes approximately half of US clean energy).

Implications for gas utilities

New era electrical transmission spacers - AEP Headquarters, Ohio. Source: 4D Infrastructure

Management teams of utility companies generally try not to get involved in ‘party politics’ or even intra party politics, for fear of ending up on the wrong side of the winning candidate. In discussions with most management teams, this ‘neutrality’ was maintained. However, in some small group discussions, certain management teams admitted to being concerned with the detrimental impact that Sanders’ climate strategy and economic policies could have on their own business. This was obviously especially the case for natural gas distribution utilities, which had concern for their own assets’ utilisation in a Bernie Sanders future; and the increased cost of gas without fracking, and impact on customer bills.

The underlying view of management teams was that Sanders was unlikely to get the required support in the Senate to implement his radical climate strategy even if he was to become President. Also, they believed there was potentially some grandstanding being undertaken by all candidates – they are aware that the oil/gas fracking industry in the US directly employs approximately three million people (according to National Geographic: How Has Fracking Changed Our Future?) and is estimated to save US consumers and industry approximately $103 billion per year in avoided gas costs (Californian Independent Petroleum Organisation).

These concerns around the future of gas in energy provision were highlighted by National Grid and its recent issues with its gas distribution operations in New York. The company had developed long-term gas supply plans based around the development of a new transmission pipeline connection which was applying for state permitting – notoriously difficult on the east coast in recent years, due at least in part to the political/ideological opposition to gas. National Grid implemented a moratorium on new customer connections until the pipe was available and the supply issue could be remedied. New York State Governor Cuomo (a Democrat candidate) threatened withdrawal of National Grid’s license to operate in the state unless short-term plans to avoid the moratorium were implemented, and National Grid removed the moratorium in November 2019. Longer term, the strategy of a new supply transmission pipeline may not change, but further consultation is required with all stakeholders to ensure other power supply alternatives have been fully tested and stakeholder input is considered.

The aftermath

President Trump is one of the most – if not the most – polarising presidents in US history. People may have different views about his effectiveness as President over the past four years, but he does represent the status quo. Undoubtedly, the share market had performed well up to late February 2020 and so investors seem to have the view that he presents a low risk option to the economy and markets in general. At the time of the Morgan Stanley conference, there was a view that none of the Democratic candidates had broad enough support outside their core constituencies to actually displace Trump in the November elections.

Fast forwarding to the time of publishing these trip notes, following wins across a number of states in primary elections (one big day is called ‘Super Tuesday’, in which a number of states elect their preferred running candidate) Joe Biden is now the very likely favourite to win the Democratic primary candidacy. Also, as a result of COVID-19 and its associated impact on the US economy, the US share market index as represented by the S&P500 has fallen by 24% (as at 31 March 2020) from its peak, and given away most of the gains it achieved through Trump’s term (since November 2016). Trump has been accused of being complacent, arrogant and untruthful through the unfolding of COVID-19 in the US, and it seems Biden may be gaining some ascendency as a result of perceived mismanagement of the virus by Trump. We believe it is too early to call, but expect the progression of COVID-19 across the US, the associated national and regional economic impact, and the government’s management of the situation to have significant ramifications for the November election outcome.

6. Second week in Southern states

Peter’s second week of travel in the US was based in Oklahoma and Texas, and mainly involved meetings with oil & gas midstream companies. A lot went on in this week as news of the impact of COVID-19 on the western world developed, and disagreements at the Organization of Petroleum Exporting Countries (OPEC) meeting resulted in significant reductions to global crude oil prices.

As mentioned in the introduction, a report on demand/supply side drivers and impact on prices is outlined in greater detail in our recent Global Matters article The impact of the oil shock on North American midstream assets. In summary, in light of the market sell-off of energy and midstream companies resulting from weak crude prices following the expected short-run demand/supply imbalance, 4D reviewed the extent to which our investment companies are exposed to the weak commodity price; and undertook downside scenario testing to understand the potential for financial distress and resulting valuation impact. Our conclusions are as follows.

- Our initial thesis that these assets do exhibit the fundamental characteristics of infrastructure assets remains intact. However, we continue to consider this on a case-by-case basis or asset-by-asset assessment to ensure we are exposed to the names offering the highest quality/value opportunity.

- The sector will be subject to ongoing price volatility until the market can recognise the disconnect between select company earnings and commodity pricing, which should play out over time. For example, Canadian operator Pembina Pipeline reaffirmed its FY20 EBITDA guidance post price shock.

- Certain sub-sectors of the midstream value chain have greater earnings exposure to crude price downside than others (e.g. gathering & processing, marketing), while others are largely immune (pipelines).

- Factoring in worst case scenarios, regardless of where a company operates along the value chain, the sector has been oversold.

- The current market seems to be pricing in a significant probability of financial distress – none of our analysed companies appear at significant risk of this scenario in the immediate future; and

- Considering revised base case scenarios and prevailing share prices, all companies represent five-year IRRs in excess of 20%. This makes them a Strong Buy according to 4D’s valuation methodology.

- A significant near-term risk to achieving these returns exists if private investors with significant capital and longer-term investment horizons opportunistically bid for these companies at their depressed share prices. A ‘healthy’ premium could get a transaction done, but still represent a significant discount to fundamental valuation. This is a real concern for us at these levels. Company boards and management teams hopefully exercise strong governance and good judgement in insisting that real fundamental value is recognised and paid by potential acquirers.

7. Conclusions

Coronavirus test post-return from the US. Source: 4D Infrastructure

The two weeks Peter spent in the US helped bring to light the increasing importance of ESG issues for US utility management teams, and the significant role that US utilities have to play in the transition to a carbon-free economy. Achieving carbon neutrality by 2050 as outlined in the Paris Agreement poses a significant challenge, but also provides a massive investment opportunity. The transition to carbon neutrality will require enormous investment in low/zero carbon generation, huge amounts of battery/storage capacity, initiatives/technology to promote energy efficiency, potentially new technology such as carbon capture and hydrogen gas, and modernisation of the network to facilitate it altogether. These requirements will drive investment for US utilities to deliver strong growth for decades to come.

The real challenge for management teams is ensuring that while they implement these technologies and transition to carbon neutrality, they maintain service reliability, customer satisfaction and affordability. Combined with clear communication with respective regulatory bodies, this should see them maintain a strong relationship, helping to ensure a constructive regulatory framework where the regulator ensures that companies receive a suitable return on investment and are remunerated efficiently.

With the US federal election slated for November 2020 (assuming no delays as a result of COVID-19), there are some questions as to the environmental and economic mandates on which some Democratic candidates may run. As of now, the likely candidate in Joe Biden is considered a moderate Democrat candidate and hasn’t communicated any radically different environmental targets or aspirations that the state level governments aren’t already pushing for. In fact, his target of achieving carbon neutrality by 2050 is in line with the Paris Agreement that the US previously agreed to (under Obama in April 2016, although Trump subsequently withdrew), and importantly is already being mandated by a number of US states and utility companies. Any concern from utility companies regarding the US elections and its potential outcome has largely relaxed.

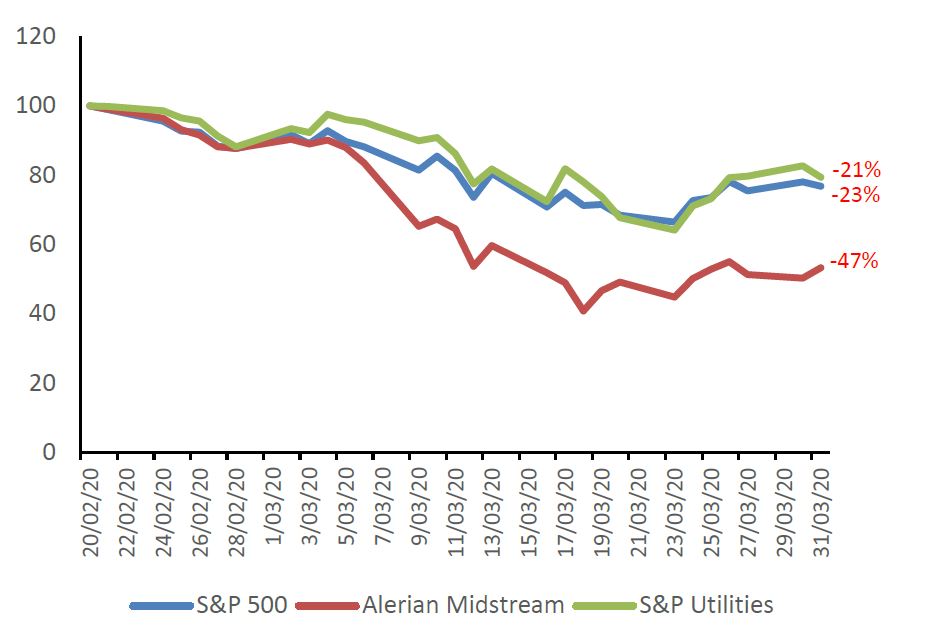

We see the market sell-off of US utilities due to the impact of COVID-19 as exaggerated, and believe US utilities now offer a very attractive investment proposition (the Total Shareholder Return (TSR) performance of the S&P 500 Utilities index against the broader market S&P 500 index and the Alerian Midstream index since the outset of COVID-19 impacting US markets is represented in the chart).

TSR performance since coronavirus starting impacting US markets: S&P 500 vs Alerian Midstream index vs S&P Utilities index

Utilities’ resilient earnings are not heavily exposed to the effects of COVID-19, especially relative to other industries and sectors. They have long dated, attractive growth drivers; and they now offer very good value at current pricing. Despite these supportive factors, utilities have only slightly outperformed the broader US market since COVID-19 started impacting US markets. We have selected high quality names based on 4D’s internal rating criteria, that now offer very attractive value, for inclusion in our global portfolio of infrastructure stocks.

Download of copy of the article here.