In this article, Sarah Shaw (4D’s Global PM & CIO) and Greg Goodsell (4D’s Global Equity Strategist) examine the politics, economics and investment impact of the current conflict.

The politics

Putin’s reasoning behind the Russian invasion of Ukraine seems principally related to Ukraine’s potential desire to join the North Atlantic Treaty Organisation (NATO), and Putin seeing this as a threat to Russia.

The Western world quickly united (including the traditionally neutral Switzerland) in opposing Russia’s actions and introducing a broad array of sanctions.

NATO is unlikely to directly assist Ukraine militarily as Ukraine is not a member, and such an intervention would lead to the first ever direct conflict between two nuclear armed super-powers. Hence the importance and extent of the non-military, economic and political sanctions. If the sanctions can effectively target and hurt wealthy Russians, then they may also ultimately influence Putin, or a social movement to oust him.

Further afield, China’s Xi Jinping will be watching the evolving situation – and importantly, the West’s response – closely. Our view is that Xi’s biggest concern is domestic social unrest, which could derail his leadership. As such, we don’t believe he can achieve this by supporting Russia (discussed further below). However, nor do we believe China will condemn Russia.

4D’s exposure to Russia

4D has never had any direct exposure to Russian securities.

Our investment process incorporates a country review process, which looks at four key parameters (economic, financial, political and ESG risks) to determine whether we believe a country is an acceptable investment destination. This review is undertaken before we even look at assets within that country.

Russia is graded Red (uninvestible) under our process, and has been so since our initial review in 2015, when 4D began. The principal reason for this is Russia’s invasion of Crimea in 2014 and its subsequent annexation. International sanctions were imposed (and remain) on Russia as a result of that aggressive action. While they are nowhere near as extensive as today’s, they clearly indicated unacceptable behaviour – hence the Red grading and no core exposure to Russian assets (see Annexure for the short form of our 2021 Russian country review).

As a consequence of the more recent sanctions, we reviewed our portfolio for any exposure to Russian assets, no matter how negligible. We placed trading restrictions on any exposed positions until companies had confirmed an exit from Russia or a writedown of assets to zero (where exit was not immediately possible), as we expect all our portfolio positions to support the current democratic stance against the invasion. As a result, negligible exposure has now been written off or the stock is restricted.

Global economic implications of the Russian invasion

IMF[1] analysis suggests that, in addition to the suffering and humanitarian crisis from Russia’s invasion of Ukraine, the entire global economy will feel the effects of slower growth and faster inflation. The IMF identified three main channels through which impacts will flow.

- Higher prices for commodities like food and energy will push up inflation further, in turn eroding the value of incomes and weighing on demand.

- Neighbouring economies in particular will grapple with disrupted trade, supply chains and remittances, as well as an historic surge in refugee flows.

- Reduced business confidence and higher investor uncertainty will weigh on asset prices, tightening financial conditions and potentially spurring capital outflows.

The IMF added that, while some effects may not fully come into focus for many years, there are already clear signs that the war and resulting jump in costs for essential commodities such as oil will make it harder for policymakers in some countries to strike the delicate balance between containing inflation and supporting the economic recovery from the ongoing COVID pandemic.

China’s response

There are concerns that China may provide assistance to Russia in its invasion of Ukraine. This could lead to the imposition of sanctions on China, similar to those imposed on Russia. At a virtual meeting on Friday 18 March 2022, US President Biden warned Chinese President Xi of possible ‘consequences’ for supporting Russia; and Chinese President Xi indicated that ‘The Ukraine crisis is not something we want to see’. He added that the events again show that countries should not come to the point of meeting on the battlefield. Conflict and confrontation are not in anyone's interest, and peace and security are what the international community should treasure the most.

Why would China assist Russia in Ukraine?

Reasons could include global politics and ensuring Russia’s future political and potential military support of China. It would also underpin a powerful military alliance balanced against the might of US/NATO in Europe. China may also see business opportunities in Russia given the economic void created by the sanctions.

Why wouldn’t China support Russia in Ukraine?

Put simply, economics, domestic politics and China’s self interest.

Differing global GDP positions

In considering whether China would support Russia in the Ukraine war it is important to acknowledge that China’s position in the global economy is vastly different to that of Russia. China is the world’s second-largest economy behind the US, with a GDP of US$14.9 trillion in 2020 (~17.8% of global GDP). Russia is only the 11th largest economy in the world, with a GDP of US$1.48 trillion (~1.74% of global GDP). By way of comparison, Australia has a GDP of US$1.35 trillion (~1.7% of global GDP)[2].

With this economic context, there is far less incentive for China to risk its globally dominant economic position to engage in a major conflict at this point in time.

China and global trade[3]

International trade is the lifeblood of the world economy, but is subject to constant change from economic, political and environmental forces. Emerging economies have seen their share of total global trade rocket in recent years.

China’s economic interests are different from its security concerns. China is deeply integrated into the global economy. Its share of global trade has increased significantly during the global pandemic, as has its share of global direct investment inflows. China’s share in global trade at the end of 2021 was about 17%, and its share in global direct investment inflows at the end of 3Q21 was ~19%. Its total trade flows, which exceeded $US6 trillion last year, dwarf those of Russia.

China’s firms and leadership are aware that major efforts to support Russia and violate existing sanctions could bring down secondary sanctions on them, especially if such support were to include military assistance. Russia is vulnerable to such sanctions; China would be even more exposed.

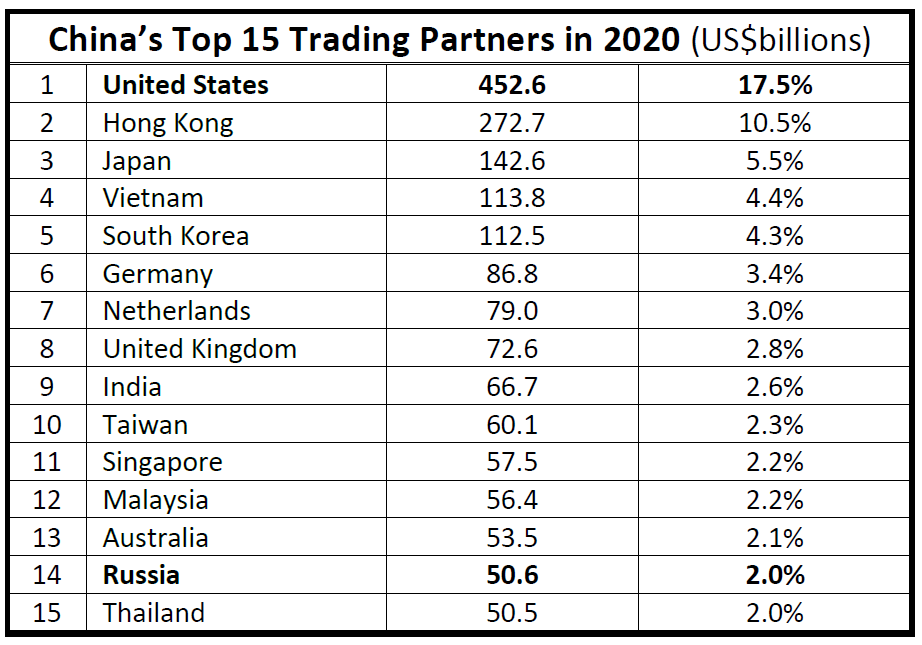

Below is a table highlighting China’s 15 top trading partners in terms of export sales. That is, these countries imported the most Chinese shipments by US$ value during 2020. Also shown is each import country’s percentage receipt of total Chinese exports.

Source: China's Top Trading Partners 2020 (worldstopexports.com)

Notably:

- The US alone accounts for 17.5% of Chinese exports – Russia just 2%;

- 66.7% of Chinese exports in 2020 were delivered to the above 15 trade partners. Many of these countries have imposed sanctions on Russia for its actions in Ukraine;

- The UK increased its import purchases from China at the fastest rate, up 16.6% from 2019 to 2020. In second place were importers in Vietnam, thanks to a 16.1% increase, trailed by Australia (up 11.2%), Thailand (up 10.8%) and Taiwan (up 9.2%); and

- There were three decliners year-over-year – namely India (down -10.9%), Hong Kong (down -2.5%) and Japan (down -0.4%).

Clearly, any trade sanctions imposed on China by the US or the rest of the world would have a material negative impact on its economy.

Chinese domestic politics

It is in China’s interest for the global economy to remain strong, especially as China is suffering a further wave of COVID and President Xi is seeking a record third term in office.

Given the Chinese government has recently set its GDP growth target for 2022 at around 5.5% (higher than most economists anticipated) and has set the goal of ‘common prosperity’, having a significant portion of the Chinese economy subjected to Western sanctions would be a major negative. China has indicated that it supports an end to the war – it is in the country’s interests to do so.

In summary

The domestic political and economic case for China to avoid supporting Russia in the Ukraine war, and risk severe sanctions from the rest of the world, is clear. Unfortunately, rational, humane decision-making has not been a feature of the Ukraine war so far, and we continue to monitor the situation closely. We also do not rule out indirect support in some way, as long as it doesn’t invoke sanctions (e.g. China buying more Russian gas, which would lower energy costs in China (domestic win) while indirectly financing Putin’s activities).

Impact on infrastructure

In broader sector terms, we have assessed the immediate and longer-term impact on infrastructure assets in terms of direct and indirect consequences of the current conflict.

Energy

The conflict has seen an immediate and sharp increase in power prices across Europe as the flow of Russian gas is disrupted and countries scramble to source alternative fuel sources. In the short term this could see coal re-enter the generation mix. Over the medium to longer term we see alternative gas sources being secured, the development/extension of nuclear generation, and further fast-tracking of renewable generation as countries look to balance the social needs of their populous with decarbonisation goals.

- Those utilities exposed to merchant pricing will be directly and immediately impacted by rising prices, which is a core reason why we don’t regard merchant energy as ‘infrastructure’.

- Regulated names, by contrast, should theoretically be insulated (with a fuel pass through). However, in reality, from a social standpoint we are seeing regulated operators (e.g. Iberdrola, Enel) cap/delay the pass-through of the very high energy prices in immediate support of customers, which will have a near-term working capital impact. Governments are also introducing short-term measures to cap power prices. Longer term, however, we hope to see this recouped through the regulatory model.

- Volumes could be disrupted across the board – again, this should have a muted impact on regulated names which earn a return on investment.

- The investment outlook is very positive as new investment programs to reduce the energy reliance on Russia are prioritised and fast-tracked. Pure play renewables such as EDPR and Orsted will benefit, as will the integrated regulated names that are prioritising energy transition, such as Iberdrola and Enel.

- Energy providers across North America and other parts of the world will look to capitalise on the jump in commodity prices, with increased hard commodity exports supporting energy pipeline transportation companies as well as port and export capacity. Names such as Williams and Cheniere[4] will benefit.

- However, we need to be cognisant of the fact that the contracted/regulated structure of the energy infrastructure names means they will not realise the full upside of the commodity price spike (much as they were largely insulated on the downside when oil was at zero – see Global Matters 25 Impact of oil shock on midstream assets (March 2020)). This is a core characteristic we look for in energy infrastructure’s visibility of earnings profiles. Should these names run ahead of fundamentals, we could look to capitalise on the gain.

Transport

Immediate impacts of the conflict can be felt in the transport space, due to closure of air space and ports as well as the disruption in commodity sources and supply chains.

- Closure of air space around the region of conflict will have a limited passenger impact on certain airports as flights into and out of Russia and Ukraine are grounded. On a deep dive, passenger exposure to Russia/Ukraine is minimal for core European airports (e.g. Frankfurt <2%, AENA network <1% in 2021).

- There has also been a localised impact on certain ports in close proximity to the conflict. Should the situation escalate, this of course could extend further – some direct impact on Hamburger Hafen (not in portfolio).

- The world is looking to source soft commodities from alternative sources, increasing port activity as well as rail volumes in places like Brazil, Thailand, Chile and North America (large net exporters of soft commodities such as corn and wheat). This could support both Rumo and Santos Brasil out of Brazil, as well as the North American rail operators.

- We could see passengers more reticent to travel to certain regions surrounding the conflict area, impacting airports in the region. To date this has not materialised, but should the conflict escalate we expect this to play out.

- The conflict could exacerbate global supply chain disruptions through increased staff shortages. According to the Seafarer Workforce Report[5] of the total workforce, ~198.1k (10.5%) of seafarers are Russian and another 76.4k (4%) of seafarers are Ukrainian. Combined, they represent 14.5% of the global seafarer workforce.

As discussed above, inflation will remain high given the contribution of energy in the CPI bucket, which continues to favour transport names (as well as real rate utilities) that have an explicit inflation hedge. However, a significant jump in fuel prices around the globe has a number of flow-on effects to infrastructure names.

- Freight rates could jump as demand profiles shift and high fuel prices are passed on to end users.

- Improved competitiveness in transportation supports those that are more fuel efficient given the spike in fuel prices (e.g. benefits rail over trucks).

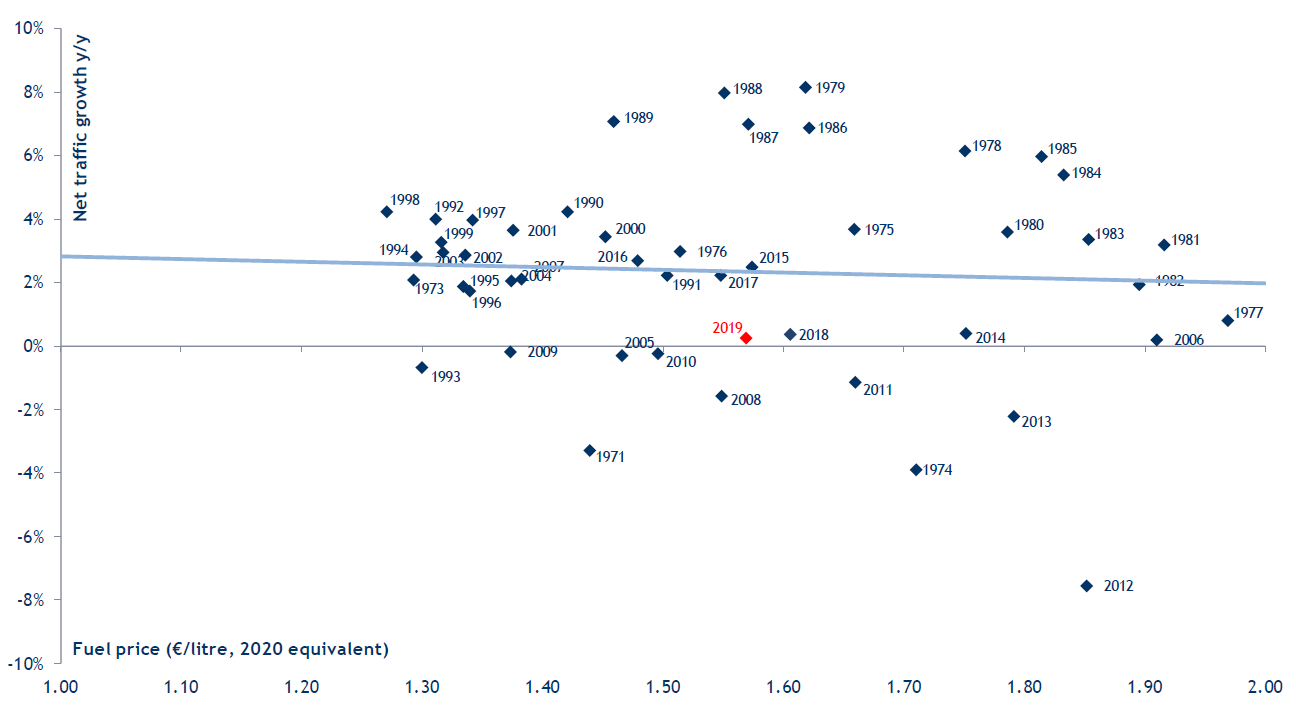

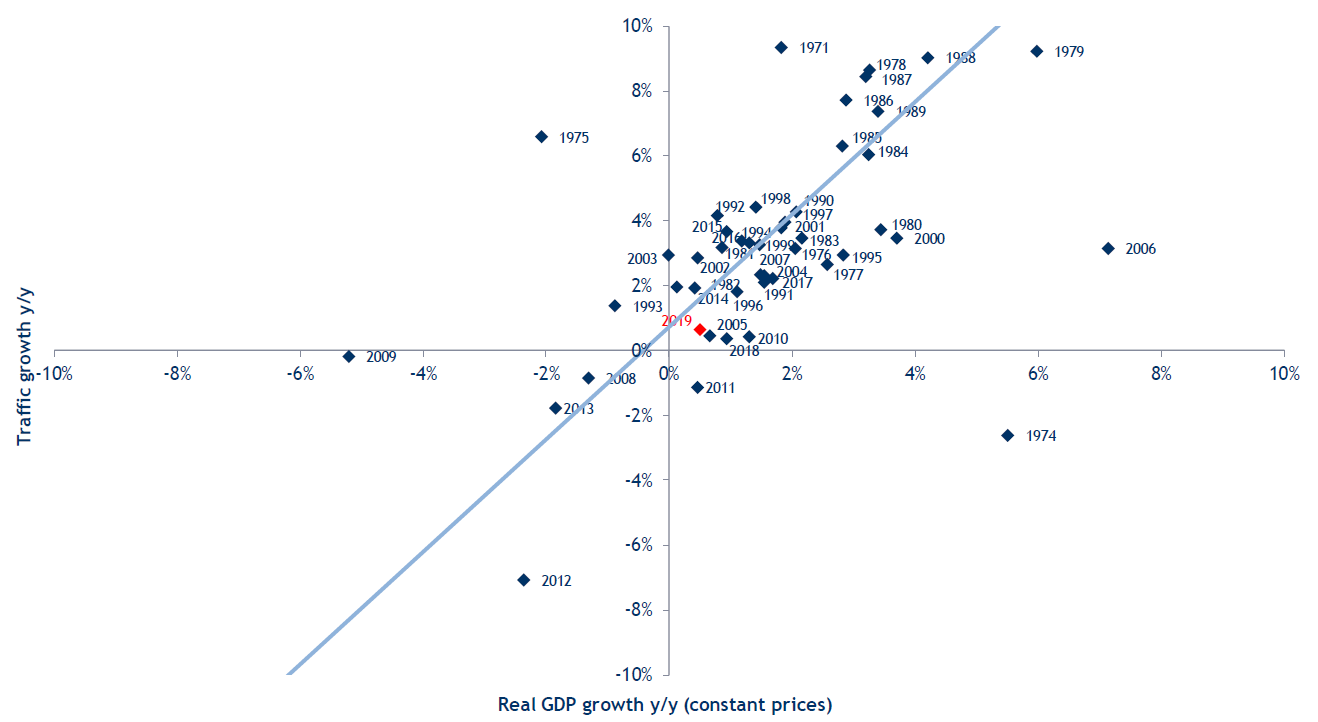

- Road traffic could see some sensitivity to soaring fuel prices. While volumes will be impacted, historically toll roads have reported a net upside from rising fuel prices as the CPI uptick to tariffs (driven up by fuel hikes) has more than compensated for the sensitivity of traffic. This is, however, dependent on passenger mix (commercial vs passenger) and sensitivity to prices. The following charts shows the relative insensitivity of toll traffic to fuel prices on Italian motorways since 1970, with the sensitivity to GDP growth much more relevant as depicted in the second chart.

Chart 1: Sensitivity of Italian motorway traffic to fuel prices

Source: Mediobanca

Note: 60% of traffic in Italian motorways are commuters driving <50km for each trip. The above correlation is one example and should not be considered a proxy for all motorways.

Chart 2: Sensitivity of Italian motorway traffic to GDP growth

Source: Mediobanca

Note: 60% of traffic in Italian motorways are commuters driving <50km for each trip. The above correlation is one example and should not be considered a proxy for all motorways.

- Air tickets will go up as airlines look to push the jump in fuel prices through to end users. Again, the overall impact on airports will be dependent on sensitivity to ticket pricing, which itself is driven by share of low cost carriers, domestic versus international etc. Again, this can be partly offset at the airport level by any inflation pass-through to regulated tariffs and/or commercial contracts.

- The inflation hedge has historically more than compensated any demand squeeze from elevated fuel prices.

Conclusion

The situation in Ukraine is, above all else, a major concern from a humanitarian and global stability standpoint. The positive aspect so far is just how fast the Western world has united in opposing Russia’s actions, introducing a large and diverse suite of sanctions designed to punish Russia economically and isolate it internationally. Potentially there are more sanctions to come.

While it will be a matter of waiting to see how effective sanctions are in influencing Russia’s behaviour, from an investment perspective there are some clear near-term negative impacts (fuel prices, energy costs and inflation uptick), but also some short-term and long-term relative winners in the infrastructure space, including user pay assets (inflation link), rail (increased competitiveness and soft commodity exposure), energy infrastructure (volume support) and utilities building for the future (integrated and pure play regulated utilities).

As always, 4D looks to maintain a diversified (regional and sector) portfolio of the best combination of value and quality within the infrastructure sector. At the same time, we look capitalise on long-term infrastructure thematics while remaining cognisant of near-term head and tail winds, including the current conflict and resultant political and economic responses.

Annexure

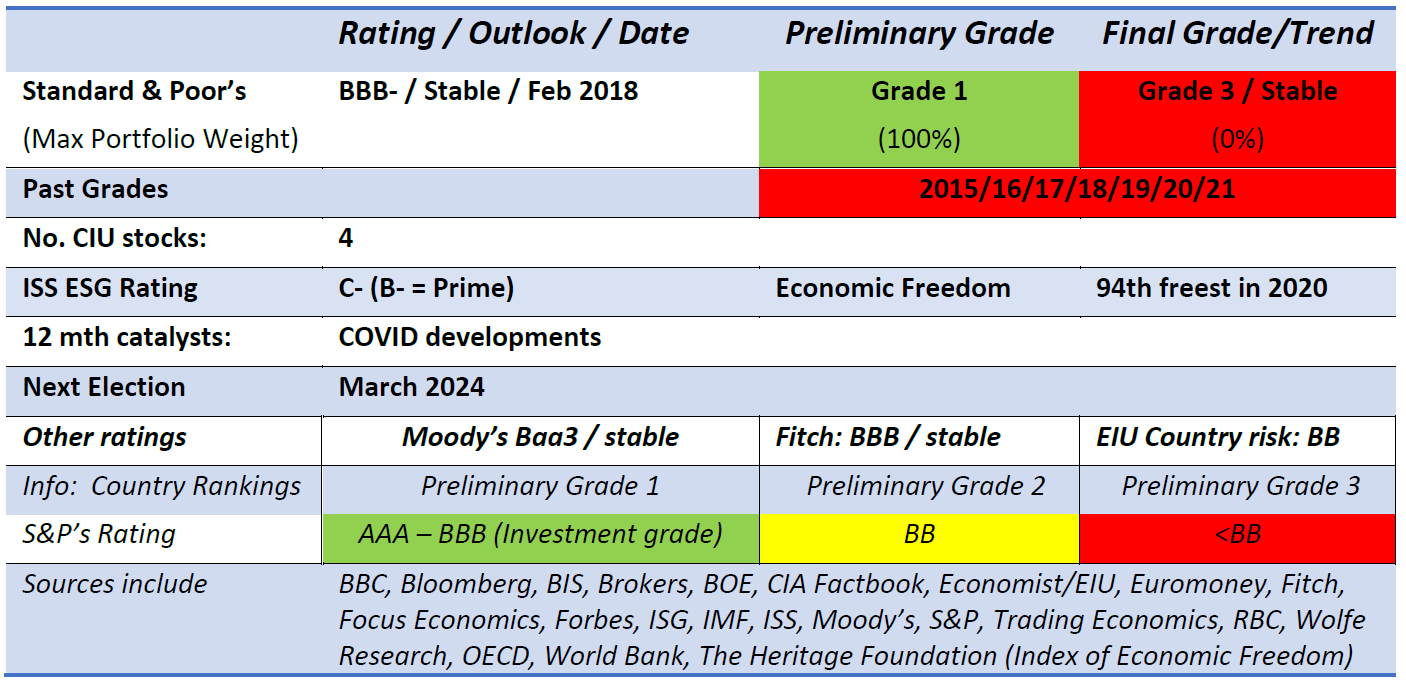

Russia Country Review: 31 July 2021

Russia Summary

Russia maintained at Grade 3 (Red Flag)/Trend Stable

Like all nations, Russia had a tough battle with COVID. An economic recovery is underway. However, we are retaining it as a Grade 3 (Red) jurisdiction for the following reasons.

Financial

- The US maintains sanctions on Russia related to Russia’s 2014 invasion of Ukraine, malicious cyber activities and influence operations (including election interference), human rights abuses, use of a chemical weapon, weapons proliferation, illicit trade with North Korea, support to the governments of Syria and Venezuela, and use of energy exports as a coercive or political tool.

- Russia’s external position is stable with a public debt ratio of a highish ~110%, CDS spreads of just ~18bp and reserves well in excess of 100% of GDP. It has generally been well managed economically.

- A Red Country Grade 3 is well below its Preliminary Grade 1, which is based on an Investment Grade ‘BBB-’ S&P credit rating.

Economic

- The Russian economy is poised to recover in 2021, with the central bank predicting it will rebound to pre-crisis levels.

- Russia has had a relatively tough COVID, with 1,079 deaths/1 million people by July 2021.

Political

- The connection between political power and property is strong in Russia, with some senior officials reportedly using their government positions to amass vast property holdings. Tensions with the West have been increasing.

- Russia’s current demographic picture is fair. The country has a large working-age population that supports a relatively small dependency ratio. The growth in this ratio going forward is a concern as the population ages rapidly, with a younger cohort in line to occupy jobs and power. It also has a high degree of income inequality, with a Gini of 0.38.

ESG

- Russia’s ESG rating by ISS is ‘C-’ or ‘Not Prime’, which is poor.

- The abundance of available energy, in the form of oil, gas and coal, leads to one of the most inefficient and highest energy consumptions in the world and an economic structure dominated by extractive industries. Transport, households and industry are squandering energy since domestic prices are kept low.

- Russia is a signatory to the Paris Accord but does not have a Net Zero Carbon goal.

- The judiciary lacks independence.

The Trend is returned to Stable with improvement hoped for.

[1]. ‘War in Ukraine Reverberates Around World’, IMF Weekend Read, 19 March 2022

[2]. Source – Stastistics.com

[3]. SMH 16 March 2022: ‘As China quietly joins sanctions against Russia, Xi night be too rational to risk arming Putin’. Tianlei Huang and Nicholas R. Lardy are China experts with the Peterson Institute for International Economics, a Washington-based think tank.

[4]. Cheniere announced on 9 March 2022 that it had agreed to amend the LNG sale and purchase agreement it has with Engie to increase the contracted volumes and extend the term of the agreement.

[5]. Published in 2021 by BIMCO and International Chamber of Shipping (ICS)

The content contained in this article represents the opinions of the authors. The authors may hold either long or short positions in securities of various companies discussed in the article. This commentary in no way constitutes a solicitation of business or investment advice. It is intended solely as an avenue for the authors to express their personal views on investing and for the entertainment of the reader.