However, this progress has created a number of climatic challenges which, if left unaddressed, could see the planet we all rely on struggle to sustain a liveable future.

Importantly, the world has recognised the challenge, and is working towards solutions and a new, sustainable future. At the heart of this is the need for ‘decarbonisation’, and meeting a global goal set out in the Paris Agreement to effectively be 'Net Zero' carbon emissions by 2050. Decarbonisation is the process by which the amount of carbon dioxide (CO2) emitted into the atmosphere is reduced.

Infrastructure, on the face of it, could be considered to be part of the problem – its build out has certainly supported the progress mentioned over the last century. However, 4D Infrastructure believes infrastructure is now a core part of the climate solution. Without significantly increased investment in infrastructure, the globe has no chance of reaching Net Zero carbon by 2050.

In this article, 4D CIO and Global Portfolio Manager, Sarah Shaw, discusses how investors wanting to be part of the decarbonisation investment thematic should look to infrastructure as a means of participating. While the speed of ultimate decarbonisation remains unclear, there appears to be a real opportunity for multi-decade investment as every country moves towards a cleaner environment. Energy transition and decarbonisation of the power sector is an obvious thematic, and will have the greatest impact on countries looking for net zero. However, other forms of infrastructure, namely transportation, also have a key role to play. This article is an introduction to the decarbonisation thematic, and is intended to set the framework for several follow-on pieces exploring in more detail the infrastructure investment solutions in aspiring to Net Zero.

1. Saving humanity from itself

Concerns over climate change, and in particular rising levels of CO2, emerged in the mid-1990s, culminating in the United Nations Climate Conference of Parties (COP) in 1995. These concerns led to the birth of a number of environmental movements across the globe, including the Australian Greens in 1992, Germany’s Energiewende (translated to ‘clean energy transition’) which originated in the early 2000s, and more recently Greta Thunberg’s Skolstrejk for Klimatet (translated to ‘school strike for climate’); increasing the pressure on the United Nations and governments for more ambitious clean energy targets.

The 2015 Paris Agreement: the key global driver of cultural change on climate

International climate policy fundamentally changed following the 21st COP in 2015 at which the ‘Paris Agreement’ was agreed. This is an agreement within the United Nations Framework Convention on Climate Change (UNFCCC) dealing with greenhouse gas (GHG) emissions mitigation, adaptation and finance. The language was negotiated by representatives of 196 states, and adopted by consensus on 12 December 2015 and formally signed in 2016.

The Paris Agreement’s central aim is to strengthen the global response to the threat of climate change by keeping the global temperature rise this century to well below 2 degrees Celsius above pre-industrial levels; and to pursue efforts to limit the temperature increase even further to 1.5 degrees Celsius (at the time, global temperatures were estimated to have risen by 1 degree Celsius). Additionally, the agreement aims to increase the ability of countries to deal with the impacts of climate change, and to make finance flows consistent with a low GHG emissions and climate-resilient pathway.

The Paris Agreement requires all parties to put forward their best efforts through ‘nationally determined contributions’, and to strengthen these efforts in the years ahead. It opened for signature on 22 April 2016, and entered into force on 4 November 2016. Since then, 189 parties (of the 197 to the Convention) have ratified the agreement[1].

In order to achieve the goals outlined in the Paris Agreement, it is thought that global GHG emissions need to be at or near ‘Net Zero’ by 2050. Net Zero refers to a position in which annual CO2 emissions into the environment are balanced by those taken out. This requires the world to come together to reduce net emissions from current levels of over 50 gigatonnes of CO2/year. It is a mammoth task, to say the least, and needs support from governments and the populous to balance the often-conflicting goals of environmental sustainability while still fostering population growth, economic advancement and social ideals. It will also require advancements in technology and its widespread adoption, all of which will require significant ongoing investment in infrastructure to support the transition.

While there is broad support for the objectives of the Paris Agreement, there is not yet widespread commitment to Net Zero emission targets. This is partly due to governments working to balance environmental, social and governance (ESG) requirements at a domestic level. Europe is leading the charge, but without greater global commitment at the leadership level the goal will remain simply that – a wish.

2. Progress creates challenges: how carbon has become an issue in the environment

There have been several crucial drivers in increasing CO2 in the atmosphere over the past 100 years.

Industrialisation: growth in transportation needs and electrification

The Industrial Revolution (IR) (1760-1840) represented a major historical turning point, with the introduction of power-driven machinery transforming the manufacturing model, driving economic advancement and altering everyday life. The IR, and the years that followed, saw significant progress, amazing innovation and great benefits; forever changing the working environment, improving the accessibility and affordability of goods, improving efficiencies and productivity, and advancing living standards for many. It also saw unprecedented and sustained population growth, supported by enhanced personal wealth and medical advancements. Today we are clear beneficiaries of this turning point in history.

However, this progress came with significant costs in terms of societal interaction, urbanisation, overcrowding and environmental impacts. There is a strong argument that the modern world’s environmental problems were, if not caused, then significantly exacerbated by the IR. To fuel development, natural resources were consumed at a rapid rate, depleting the planet’s stockpile of natural capital. This depletion has never been replenished, and in fact has accelerated over time. The more countries industrialise to support their own evolution, the greater this ecological impact becomes. To put some numbers on this, pre the IR (~1750), CO2 emissions were 275-290 parts per million by volume (ppmv). This had increased to over 400 ppmv by 2017[2].

Globalisation: leading to enhanced standards of living

Advances in transportation and technology have seen a rapid globalisation over the last century, starting with the IR and the advent of international trade. It gained traction over the years, particularly the last 30 years, driven by the rise of the internet. Globalisation and the free movement of people, capital and goods has created enormous opportunities, and supported significant economic growth. It has also allowed the emerging world to find its place on the global stage, and is fostering a rapid emergence of a middle class.

While recent analysis suggests globalisation may have peaked, and the next chapter for the global economy will focus more on domestic demand and self-sufficiency, the impact to date on the global landscape cannot be ignored. Nor can the consequences of globalisation on carbon emissions, with the world chasing the lowest cost alternative in all things, wherever it may be located. Cheaper output, increased consumption and the disposable nature of goods and services lead to increased production, distribution and CO2 emissions.

Population growth: significant environmental consequences

Carbon emissions are directly correlated with population growth. Humans consume around 40% of the Earth’s land-based net primary production – a measure of the rate at which plants convert solar energy into food and growth. As the world’s population continues to grow and the middle class continues to evolve, the planet’s finite resources are increasingly being appropriated for human use, reducing what is available for plants and animals supporting the ecosystem (clean air, clean water, etc).

In 1900, the global population was approximately 1.65 billion people, and by 2000 that number had grown to 6.1 billion. By the turn of the next century, the global population is expected to be over 11 billion, even assuming a much slower growth rate than historically

[3]. With carbon emissions per capita expected to continue edging upwards, population growth alone represents a significant challenge from an environmental standpoint.

Chart 1: Projected world population to 2100

Source: UN Department of Economic and Social Affairs, Population Division 2017

Importantly, much of this population growth has and will continue to come from the emerging world, where demographic trends are very supportive of economic evolution. This comes with an increasing carbon footprint, as discussed below.

This population growth compounds environmental and climatic challenges, and underpins the need for more infrastructure investment to ensure the sustainability of the planet. We must first address existing issues, and then put in place sustainable solutions for future generations.

Demographic trends: leading to further environmental pressures

The emergence of the middle class, particularly in emerging markets (EMs), is a theme we at 4D find very exciting at present, and one we believe will provide enormous opportunity for investors. However, it is also a theme that puts pressure on carbon emissions, as improved standards of living are correlated with increased individual carbon footprints.

From an individual’s perspective, as personal wealth increases in a country (reflected by a growing middle class) consumption patterns inevitably change. This starts with a desire for three meals a day, then moves to a demand for basic essential services such as clean water, indoor plumbing, gas for cooking/heating and power. With power comes the demand for a fridge or a TV, which increases usage as well as the need for port capacity and logistics chains. Over time this progresses to include services that support efficiency and a better quality of life, such as travel, with a demand for quality roads (on which to drive that new scooter and then car) and airports (to expand horizons).

Given the potential size of the middle class in EMs (today China, India and Indonesia alone account for around 40% of the global population), changes in spending and consumption patterns will have significant implications for global business opportunities and investment for decades to come. However, it will also compound environmental challenges as these communities evolve.

For example, at present only around 10% of the Chinese population has a passport (and less than 5% in India); yet, pre COVID-19, airports globally were reporting record passenger numbers driven by Chinese tourists. At the World Economic Forum in Davos last year, the CEO of Chinese travel provider Ctrip, Jane Sun, predicted the number of Chinese passport holders would grow to 240 million by 2020. At the time, about 120 million Chinese citizens, 8.7% of the population, held a passport. In our view this is just the start.

Chart 2 shows that as disposable income has grown in China, so too has the amount of travel undertaken by Chinese residents, both domestically and overseas. While this chart is a little old, the trend has continued, and post the COVID-19 blip, we expect it will continue for years to come.

Chart 2: Rising disposable income/capita in China has had a positive impact on domestic trips/person and outbound departures

Source: Morgan Stanley Research, Blue paper: Why we are bullish on China, February 2017

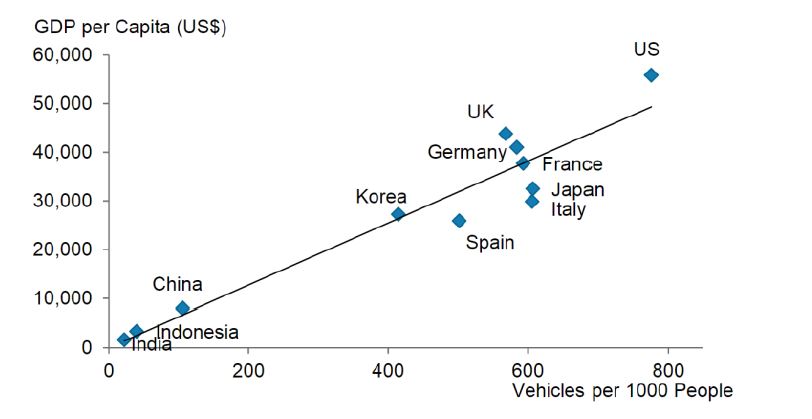

A further example of the impact of an expanding middle class is the correlation between growth in GDP per capita and vehicle ownership, as shown in Chart 3. China, like India and Indonesia, still has a low level of vehicle penetration. However, as each nation’s GDP per capita continues to climb, it can be expected that so too will each country’s level of vehicle ownership.

Chart 3: China/India/Indonesia’s auto penetration v other nations 2015

Source: Morgan Stanley Research, Blue paper: Why we are bullish on China, February 2017

A growing demand for power and a desire for an improved quality of life (transportation modes) increases the pressure on the environment as it struggles to keep pace with the evolution. Are we to preclude these economies from evolving to a standard that the developed world enjoys? Clearly not, but this growth of the middle class creates challenges which should not be ignored, and we believe are better addressed at the outset rather than trying to rectify a growing problem in the future (much as we are doing in the Western world).

When you put these factors together – developed market industrialisation, globalisation, population growth (largely driven by the EMs) and demographic trends (such as the emergence of the middle class in EMs) – the challenge of managing the planet’s finite natural capital to support its future becomes clear.

3. Challenges create progress: why increased infrastructure investment is key to the solution

Infrastructure provides the basic services essential for communities to function and for economies to prosper and grow. For us at 4D, this equates to the publicly listed owners and operators of essential services (regulated utilities in gas, power and water), and user pay assets (toll roads, airports, ports and rail, where a user pays for the service).

On the face of it, this infrastructure has significantly contributed to current environmental concerns – electrification and transportation are big drivers of carbon emissions, as discussed below. However, we believe further infrastructure investment is now a core part of the solution, as there will be no ‘Net Zero’ without increased investment in infrastructure. This opportunity is a key thematic to which investors can gain exposure, and one not derailed by COVID-19. In fact, in all likelihood it increases as governments fast track infrastructure roll out and green policies as part of much needed economic stimulus programs.

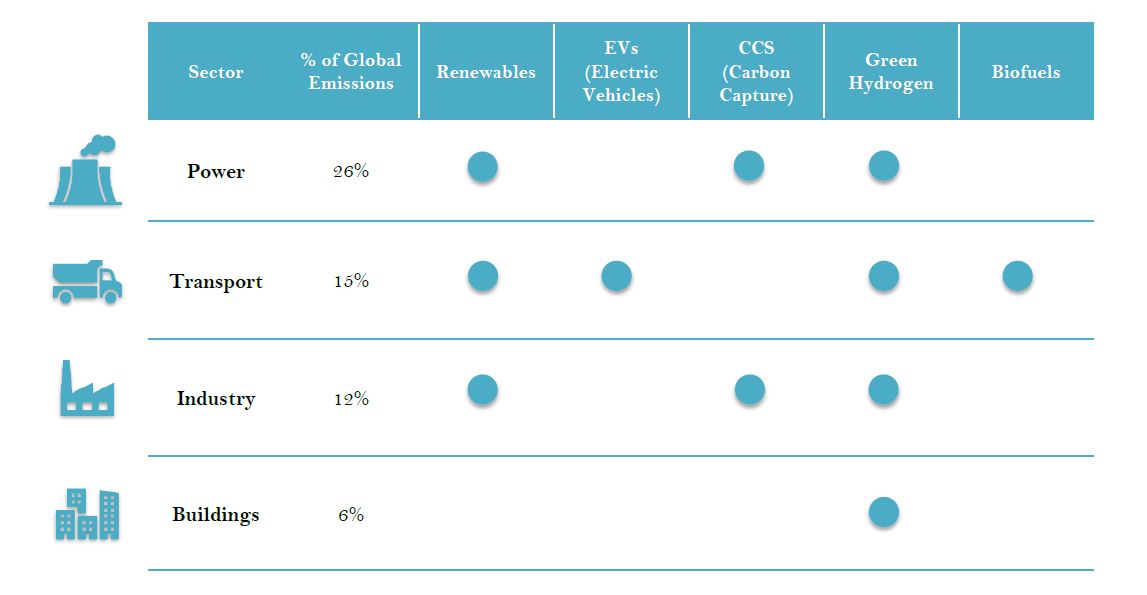

Morgan Stanley [4] estimates US$50trn is needed in investment in 5 key decarbonisation technologies (primarily in the energy space) over the next 30 years if we hope to meet the Paris objectives, equating to US$1.6trn a year. This number just grows when looking at other information sources: the OECD estimates US$6.9trn pa of infrastructure investment is needed by 2030[5] while IPCC forecasts US$2.4trn pa is needed over the next 15 years to keep temperature rises below 1.5 degrees[6]. Whatever source is used, and even if we assume that only a portion of the needed investment will be done, there is a clear, long duration opportunity that infrastructure investors must look to capitalise on, considering how essential infrastructure is to decarbonisation.

Chart 4: The 5 key decarbonisation technologies offering solutions for a number of sectors

Source: Morgan Stanley Research sourcing IEA, Hydrogen Council

Source: Morgan Stanley Research sourcing IEA, Hydrogen Council

Power sector: transition needed

Electricity generation has been correlated with population growth and economic activity (demand profiles), increasing at a compound rate of approximately 2.9%[7]pa over the last 35 years. Even on conservative targets, global electricity generation is expected to continue to grow at 1.5% pa over the medium to longer term.

Electricity generation is a core contributor to CO2 emissions, averaging around 25% of all global carbon emissions. In Australia, electricity generation accounts for 35% of the country’s total CO2 emissions; in the USA it makes up 33%. The numbers are lower in parts of Europe, which have been leaders in the deployment of renewable energy, and also in parts of the emerging world due to its stage of development, but as the middle class evolves they will quickly catch up unless we implement measures today to support a greener evolution.

Transitioning to a Net Zero world is near-impossible without commitment to decarbonise the power sector. Ignoring the sheer volume of green capacity needed, it is widely believed that this challenge of carbon neutrality cannot be practically met with the cost and capability of technology as it is today. In other words, we must assume some major improvements in technology and a continued lowering in its cost to feasibly implement carbon neutrality by 2050, while ensuring electricity affordability for customers.

While there remains a lot of scepticism about the world’s ability to achieve this, the commitment to the target is real, with increasing political and social support. It will require significant investment in the form of increased renewable (wind, solar, and hydro) capacity, transmission and distribution infrastructure to get zero-emission electricity where it is needed, and strengthening of the security of supply through energy storage. New clean-technologies such as utility-scale battery, green hydrogen, and carbon capture and storage (CCS) all need to play a role.

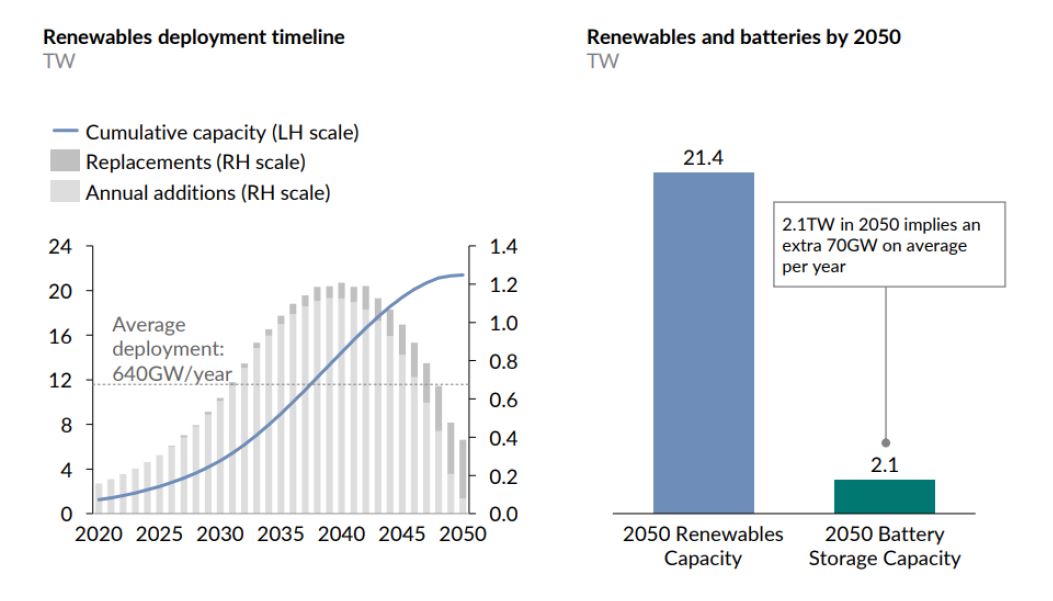

Renewable energy is the cornerstone of decarbonisation, with both direct (reduction in fossil fuels) and indirect (facilitating clean mobility and green hydrogen) benefits. Aurora Energy Research estimates that Net Zero will require over 20TW of additional renewable capacity and 2TW of storage globally by 2050, or 640GW/year in renewable deployment. Morgan Stanley[8] forecasts 24TW in renewable capacity needs by 2050, or 11 times the current capacity levels at a cost of over $25trn.

Either way, the need for renewable investment is huge, and this is just one aspect of the energy transition. This renewable power then needs to be connected to users, and the system requires increased investment to ensure security of supply. This all requires infrastructure investment to support and facilitate it. And this is before we even get to the necessary investment in new technologies, such as carbon capture and green hydrogen, which require even more infrastructure – and even further out, the potential for nuclear fusion (see Appendix 1 for an introduction to each of these future technologies).

Chart 5: Need for renewable capacity

Source: Aurora Research – study commissioned for UBS September 2020

A deep dive into this transition and all the associated technologies deserves more than one white paper, but at a very high level, it’s clear that a great deal of new infrastructure is required to replace existing carbon heavy generation sources, as well as to support future demand growth in a carbon neutral way.

Companies engaged in the provision of electricity – through energy transportation and storage, generation, and transmission and distribution – make up a significant proportion of the global listed infrastructure (GLI) investment universe. Utility stocks globally are recognising the important role they need to play in the energy transition, with 4D favouring those that have been forward thinking and are capitalising on the opportunity: such as pure play renewables (EDPR) or those integrated along the value chain (such as Iberdrola in Spain and NextEra Energy out of the USA – case studies provided in Appendix 2).

Further, as part of our country analysis we consider the political will, the plans and the execution of green energy targets. Country targets flow down to corporate targets as they look to meet or better the country position. To that end, we currently favour Europe over the USA in terms of climate policy and execution – the recently announced EU stimulus plans have been directly linked to decarbonisation to provide the dual benefit of stimulating a post-COVID economy while fast tracking environmental targets. Many of the listed utilities are already capitalising on the opportunity through increased roll out of renewables, hydrogen and carbon capture trials or strengthening of grids.

Transportation: another significant global emitter

The transport sector accounts for 15% of global CO2 emissions[9] and, after the power sector, is a major emitter. Energy demand from the transportation industry is expected to grow rapidly between now and 2050. While road transportation will account for the majority of this increased demand, aviation will grow at the fastest rate as a consequence of an emerging middle class. As such, to deliver a greener world, focus must also be directed at greener transport if we are to have any hope of reaching Net Zero by 2050. We believe this will largely come at a cost to users. However, investment in infrastructure can help reduce this burden and create greener mobility.

Road: electric vehicles and ‘clever roads’

Motor vehicle penetration has grown rapidly over the last 100 years in line with improving wealth demographics and a decline in the cost of motor vehicles as more budget options enter the market. This has created significant congestion across cities not designed for the influx of vehicles. This clearly has environmental ramifications at several levels, including:

- Sheer number of emitting cars on roads;

- Congestion levels compounding emissions as journey times are lengthened; and

- Demand for materials and more roads, with the construction industry a net emitter.

Today, cars account for around 7% of global GHG emissions. Again, without a revamp of the sector, decarbonisation targets are in our view unachievable; particularly as penetration continues to ramp up across the emerging world and the trend to larger vehicles continues.

The motor car itself must decarbonise; an event being actively fostered by car manufacturers around the world. This started with the increased usage of biofuels, and in recent years has been fast-tracked by the advent of electric vehicles (EVs). In some countries the transition is being supported by government subsidies to improve competitiveness of EVs against traditional gas guzzlers and/or regulations making it close to impossible for traditional vehicle designs to meet emission standards.

This in turn creates a demand for improved infrastructure to not only cut down congestion times, but also to support the rise of greener transportation, including:

- More renewable energy so EVs are completely green – Morgan Stanley forecasts the rise of EVs will require over 1 TW of incremental generation capacity by 2050 at a cost of US$1.6trn;

- Roads that accommodate high speed EV charging – charging infrastructure alone is a US$2trn market out to 2050;

- Roads constructed and maintained using recycled aggregates;

- Roads that can communicate with the vehicle as you drive, reducing congestion; and

- Roads that capture and distribute renewable energy, which themselves become a green electricity generation source.

As infrastructure investors we seek to identify those companies that are thinking ahead to the future of road transportation. For example:

- Ferrovial and Transurban are both heavily involved in the build-out of managed toll roads across the USA that facilitate dynamic tolling, allowing the operators to manage traffic flow with tolls to optimise the user experience and reduce overall travel times/congestion;

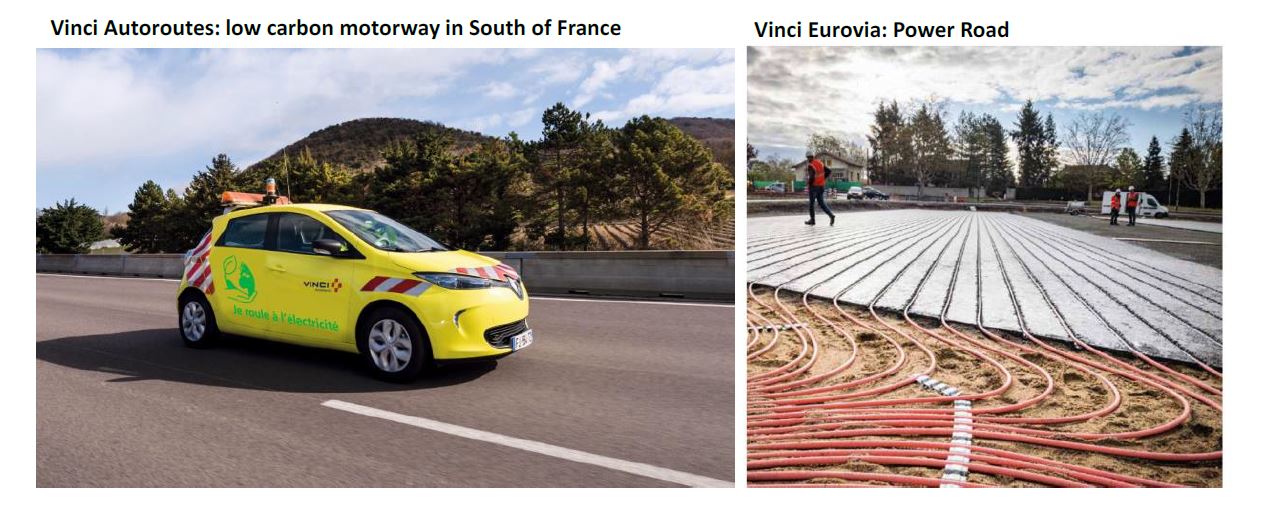

- Vinci (out of Europe) has very ambitious environmental targets at the Group level, including a 40% reduction in the carbon footprint of Vinci’s business activities by 2030. Innovative projects to support this goal within the roads arena include:

- Using 100% recycled road technology at subsidiary Eurovia;

- High speed charging stations along all of Vinci’s Autoroutes (toll roads);

- Fostering shared mobility via dedicated carpooling facilities and fees;

- The trialling of an I2V (Infrastructure to Vehicle) data exchange platform; and

- ‘Power Roads’, which use the road and solar heating technology to generate electricity.

Chart 6: Vinci’s vision for the future

Source: Vinci

Air: more efficient aircraft, ‘smarter’ airports and possibly a carbon tax

Aircraft are often considered the ‘devil’ of environmental warriors; yet at just 2.8%[10], air transport makes up a comparatively small contribution to CO2 emissions today. However, in a world where we believe air travel is here to stay and with air traffic growth expected to continue to outpace GDP growth, emissions will increasingly become relevant unless we instigate measures today.

Like the road industry, decarbonisation depends on measures taken by both the aircraft (including airlines) and the infrastructure providers (including airports).

With increased investment in capacity, the use of biofuels and hydrogen can help lower net emissions by aircraft, but with today’s technology this will come at a significantly increased cost (premium over fossil fuels). On balance, without significant technology advancements we believe the air industry will remain emitters for the foreseeable future.

As such, a business model could be adopted that allows the air industry to compensate for its emissions – this could take the form of a carbon tax or some other form of penalty on the emitter. Morgan Stanley forecasts that a starting point for a global carbon price is US$40/ton with above inflation increases going forward. This cost will ultimately be passed through to the end users.

Either way, with aircraft using environmentally friendly fuel and/or a carbon tax, it seems clear that the cost of decarbonisation will be borne by the industry and users – ticket prices are a function of an airline’s operational costs (which include fuel and, in the future, we expect a carbon tax), a fee to access the relevant airports, and a profit margin.

In order to support the transition in the most cost-effective way and keep air travel affordable in future, airports need to commit to reduce their own carbon footprint, but also facilitate airlines to move towards a more carbon neutral position.

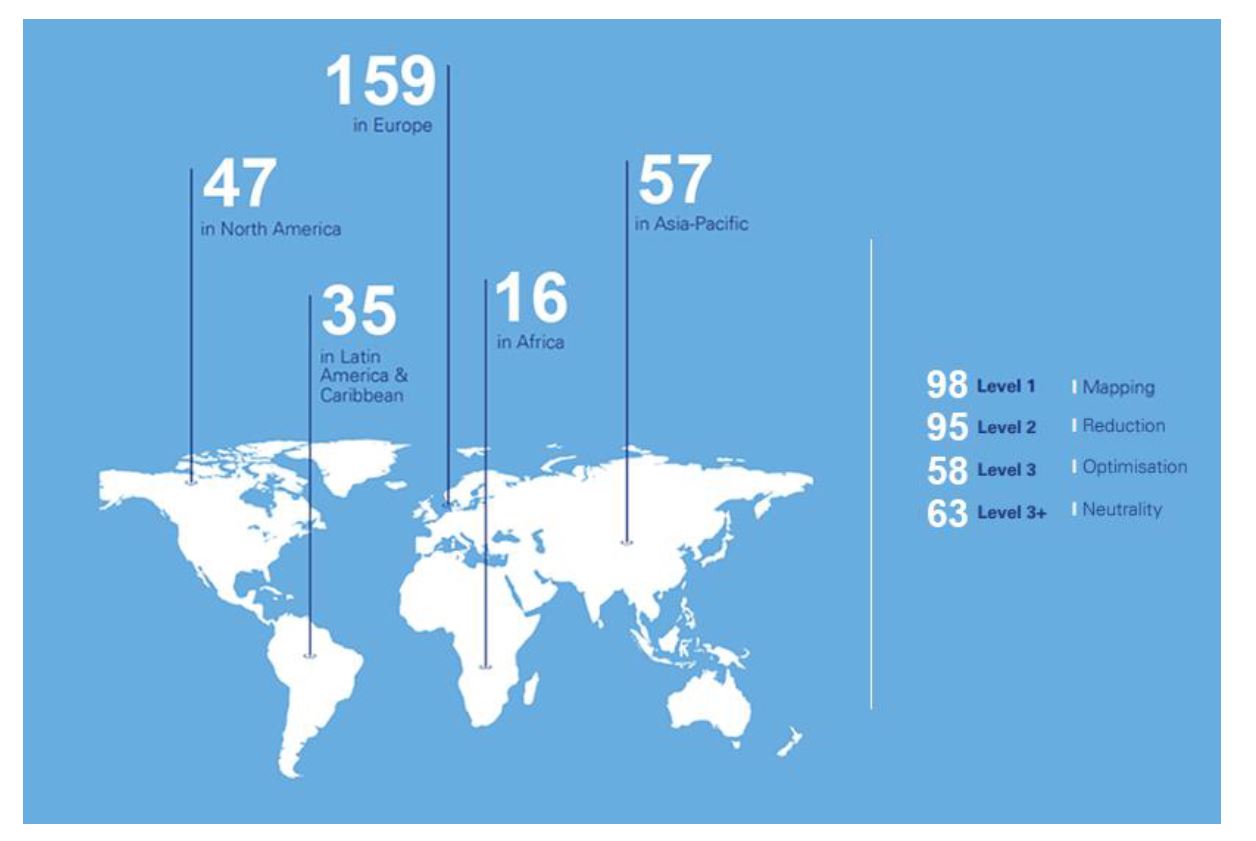

The Airport Carbon Accreditation of the Airport Council International has provided a four-step framework by which airports can have their emissions ranked externally:

- Level 1: Mapping – Carbon footprint measurement

- Level 2: Reduction – Reduction of carbon footprint

- Level 3: Optimisation – Engagement with others on the airport side to reduce CO2 emissions (this includes airlines, retailers, controllers, etc)

- Level 4: Neutrality – These airports are carbon neutral offsetting any residual CO2 emissions from the airport operation.

There are currently 314 airports in the above program across 71 countries, representing 44.8% of the global air passenger market. Europe is again leading the way with 159 airports ranked, 51 of which are already carbon neutral. This accreditation is monitored across our universe of assets.

Chart 7: Airport Carbon Accreditation global footprint

Source: Airport Council International

At 4D we favour airports participating in the accreditation process, and/or those adhering to climate goals and supporting an overall industry emission reduction. For example:

- Vinci’s airport group was among the first airport operators to develop an environmental policy on a global scale and, by the end of 2019, had reduced the carbon footprint of its airports by over 20%. Its new Brazilian airport in Salvador Bahia has been a case study in environmental upgrades with its own solar farm, a wastewater treatment facility, and a waste sorting facility supporting zero waste to landfill. It has already been named Brazil’s ‘most sustainable airport’.

- Fraport airport group is considered an environmental leader in the transport space according to external ESG provider Institutional Shareholder Services Inc (ISS), with CO2 emission targets of -65% by 2030 (relative to a base year of 1990) and an aim to be carbon free by 2050 in Frankfurt. And these goals do not stop at Frankfurt, with emission targets in place across their entire airport portfolio. In order to achieve these goals, they are investing in energy efficiency and renewable sources (the energy mix at Frankfurt is currently 55% renewable), as well as technological and infrastructure upgrades.

Sea: maritime shipping is more efficient than others, but there is more to do

Maritime shipping is the world’s most carbon efficient form of goods transportation. However, shippers are also carbon emitters. As consumption continues to grow around the world, the transport of goods and subsequent emissions are only going to increase.

As with other mobility industries, shippers are cognisant of the need to reduce their carbon footprint. The size of vessels is growing to facilitate the demand, and on a per unit basis, the larger the vessel the lower the carbon footprint – in this case, bigger is better for the environment. They are also working on efficiency, ship design, fuel sources and technical improvements to further reduce emissions. According to the World Shipping Council, the majority of new ships (since 2013) are 30-40% more carbon efficient than older ships.

Again, the maritime industry requires support from infrastructure players to ensure facilities are in place to support larger vessels or newer designs – this requires investment in ports to expand quay lengths and draft depths. LNG and biofuels are also being explored as alternative, more environmentally friendly, fuel sources. Should this gain traction, we would see an increased demand for LNG, which needs the support of the infrastructure players in the pipeline and gas distribution space. Without infrastructure investment, shippers will be hard pressed to continue to reduce their footprint, and could see costs rise as a result (e.g. via carbon taxes).

4. A huge investment opportunity emerging: time to be part of it

At 4D, ESG assessments have always played a key role in our investment process. We have a unique, integrated approach to investment, whereby country risk analysis is combined with individual stock analysis in a single analytical cycle. ESG analysis is conducted inhouse, with ISS providing an external data feed into our analysis.

ESG factors are considered in screening stocks in and out of our investment universe, through our country review process and stock analysis, as well as at the portfolio measurement stage. This analysis has always been incredibly important at 4D, with the ‘E’, the ‘S’ and the ‘G’ all deserving of review. While this article focuses on the ‘E’ and the need for climate response via infrastructure investment, it cannot be considered in isolation as social factors and governance models will have a significant contribution to the success of global environmental goals. I reference our

Global Matters 24: ESG at 4D for a complete look at how we integrate ESG into our investment process, and below will focus on how we are measuring our portfolio’s contribution to the decarbonisation thematic.

4D’s internal stock quality assessment

As part of our internal stock analysis, we assign a Quality Grade to each company. This grade is made up of a number of industry, asset and management assessments, including an overall ESG grade which is broken down into respective environmental, social and governance assessments. Within the environmental score, a company is assessed on its historical performance, its transparency and its targets and plans to meet industry and global benchmarks on environmental factors. This analysis is conducted internally with input from ISS.

New disclosure on carbon emissions to be required from fund managers

Common reporting requirements are being developed under the Paris Agreement, and are to be available for review by the end of 2020. While the formats have yet to be finalised, set out below are illustrative examples of what potential reports may look like (as developed by ISS) together with comments on recent develoments in GRESB/GLIO – the investor-driven global ESG benchmark for the infrastructure sector.

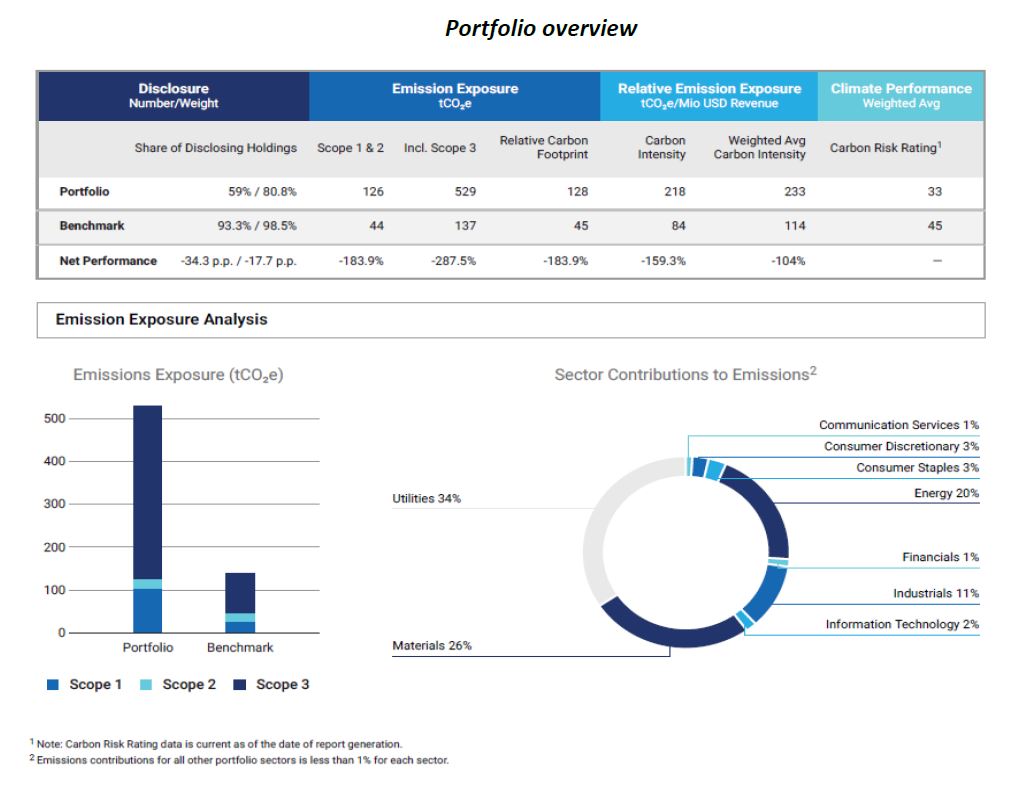

- Portfolio overview versus a benchmark. This report provides a comparison of an illustrative portfolio on emissions grounds against a benchmark.

Source: ISS ESG

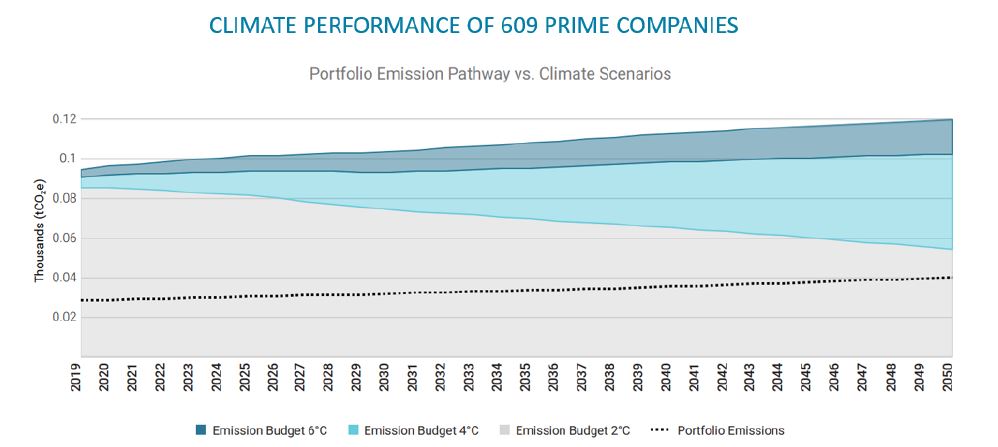

- Ongoing portfolio compliance against the 2 degree target. This illustrative ISS report shows that a sample portfolio of 609 companies rated as ‘Prime’[11] by ISS on ESG grounds would comply with the 2 degree target out to 2050.

Source: ISS ESG

- New GRESB/GLIO infrastructure public disclosure dataset. In 2019, GRESB and GLIO released a new public disclosure dataset measuring the level of material ESG disclosure by the listed infrastructure sector. The dataset’s initial coverage will enable investors to evaluate ESG transparency levels across the entire global listed infrastructure universe.

The GRESB/GLIO dataset collection is unique in that GRESB originally gathers the information and subsequently provides each company with the opportunity to review and correct the data.

5. Carbon: the times they are a changin’

Decarbonisation must happen, and the goal of Net Zero is just not achievable without the right forms of infrastructure investment across both the energy and transport sectors. This represents a significant opportunity for infrastructure investors such as 4D, who want to be part of the solution.

ESG is embedded in 4D’s investment philosophy and is fundamental to our process. We believe by a proper analysis of the integrated elements of ES&G at both a country and corporate level, an investor can capitalise on the huge and long duration decarbonisation thematic and be part of a sustainable future.

4D manages a diversified portfolio of stocks across the utility and transport sectors. We prioritise both countries and companies with strong management teams, defined strategic environmental goals that integrate with an ESG policy, strong balance sheets to support much needed investment, and those that are best in class within their sector in building a sustainable infrastructure footprint. This applies whether it be pure play renewable operators, toll roads supporting EVs and a reduction in congestion, or airports that are themselves targeting net zero. This assessment dictates a company’s quality grade, which must be married with valuation metrics to warrant investment.

Decarbonisation can’t be fully explored in one article, so over the coming months I look forward to sharing with you our deeper dives into the energy transition, the rise of green hydrogen and other related themes.

To receive CPD points for reading, view this article on AdviserVoice’s website and complete the questionnaire.

[1] UNFCCC as at September 2020

[2]Encyclopedia Britannica

[3]The United Nations is forecasting that population growth will slow from the 1.5-2% levels of the last 50 years to well below 1% for the next 80 years.

[4]Morgan Stanley: Decarbonisation: the Race to Net Zero, Oct 2019

[5]OECD: Green Finance & Investment, Morgan Stanley

[6]The Economist: Conquering carbon dioxide, Nov 18, Morgan Stanley

[7]BP Energy Outlook, 2019

[8]Morgan Stanley forecasts: 24TW includes 11TW of new renewable capacity for power generation at a cost of $14trn, as well as 12TW to support electric vehicles and hydrogen technologies

[9]2017 figures according to IE, IPCC and Morgan Stanley

[10]Fraport sustainability report referencing www.klimaschutz-portal.aero

[11]ISS uses a broad ‘Prime/Non-Prime’ approach to rating countries and companies in terms of ESG as well as individual entity gradings on an A-D basis.