This is the abridged version of the article. View full article with the Appendix.

We predict 2024 will primarily be about central banks treading a fine line between waiting long enough to see inflation sustainably lower and holding rates too long in severely contractionary territory, causing a shock to the economy.

Moving past peak rates and lower yields, even if settling higher than in recent cycles, will be a tailwind for long duration infrastructure assets. Furthermore, even with anticipated lower economic growth in 2024, underlying earnings growth in the sector remains strong with multi-decade investment and tailwinds from five core long-term infrastructure growth dynamics. At 4D, we believe these drivers should support the sector in a pivotal year for the global economy to somewhat normalise post-Covid.

In this article, Tim Snelgrove (Investment Director) & Sarah Shaw (Chief Investment Officer and Global Portfolio Manager) discuss the key economic factors currently in play, consider other recent developments that could impact the global economy over the medium to long term, and discuss what this means for the investors in the global infrastructure sector and for our portfolio positioning.

2023 year in review

We entered 2023 with an uncertain macroeconomic outlook, but with some green shoots emerging. As we said in our 2023 outlook article,

“The key concern in global equity markets remains ongoing inflationary pressure and the impact of monetary tightening undertaken by central banks in combatting inflation, potentially pushing economies into sharp slowdowns and maybe even recession…. Clearly, a key concern in the 2023 outlook for equity markets remains the ongoing inflation pressure and the risk that central banks overreact in their monetary tightening.“

Many predicted a technical and/or earnings recession heading into 2023. However, exiting 2023, US growth surprised on the upside, inflation appears to have cooled faster than expected, and risk sentiment led to new highs in major equity indices. This was despite a US banking crisis in March that saw three small to mid-size US banks fail over five days, political stalemate in the US and a heightened geopolitical environment with the Israel-Hamas conflict erupting in October. In summary:

- Growth: global economic growth outperformed expectations materially, with global GDP up 2.7% in 2023, 1% above the Bloomberg consensus at the start of the year. The US grew 2.4%, which is two percentage points above the consensus a year ago – including a 4.9% annualised Q3 growth rate, which heightened fears that the economy was running too hot, putting upward pressure on inflation and forcing the Fed to keep rates higher for longer. The consumer was the driver of this growth, boosted by a tight labour market, fiscal support and a full drawdown of excess Covid savings.

- Inflation: US inflation peaked at 9.1% in June 2022. US inflation in November was 3.1%, with 6m core annualised under 3%. Meanwhile European inflation was 2.4% in November, down from a peak of 10.6% in October 2022 driven by lower energy prices. Similarly, emerging markets (which were quicker to raise rates to combat inflation and a stronger USD) saw strong disinflationary trends over 2023, particularly driven by falling food prices. In Australia, domestic demand continues to run too hot to bring inflation down to target, and as such, is the only developed market economy with a chance of a final rate hike this year before easing in the second half, with a much slower disinflation path.

- Yields: long bond yields hit levels not seen since the Global Financial Crisis (GFC), with US 10-year yields touching 5%. This was driven by a “good news is bad news” dynamic, with strong US economic growth, a widening fiscal deficit, larger than expected treasury issuance, Fitch’s US sovereign debt downgrade in August, and Japan’s BoJ letting Japanese yields float to 1%, which made US yields relatively less attractive. These all had impacts on the term premium widening, and longer-term yields pushing higher. November saw a sharp reversal of yields due to softening US activity data, a dovish Fed due to soft inflation prints and a less-tight labour market. As a result, US 10-years closed only 11bps higher for 2023, but this hides the elevated bond volatility and the highest positive correlation between bonds and equities in 25 years (as opposed to the typical negative correlation).

- Policy rates: the Fed has raised interest rates 11 times since March 2022, the fastest tightening since the 1980s, bringing the target range to 5.25-5.5% and the highest since 2001. Other developed and emerging markets’ central banks followed similar paths. With the cooling of inflation and activity data, market expectations are for these policy rates to have peaked – the key question is, how long ‘til rate cuts occur?

Inflation, growth and interest rates

The global disinflation cycle should continue into 2024…

..but with a slowing of the pace of disinflation, as the ‘last mile’ of gains becomes harder to achieve.

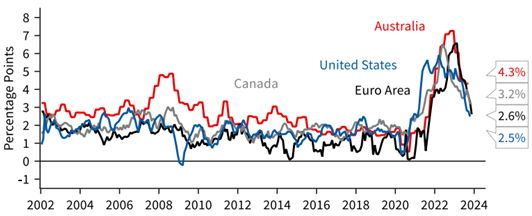

The main factors that led to high inflation have now eased or reversed. The big spikes in energy prices, supply chain issues (measured by supplier delivery lags), excessive central bank support, and super-stimulative fiscal policies have all eased – cooling inflation. We have recently seen goods deflation in many economies, while services inflation remains elevated (but falling) driven by wage growth and elevated shelter costs (which should fall further in the US). A less tight labour market is also cooling this wage growth, alleviating forward services inflation expectations.

Six-month annualised core inflation

Source: NAB

High rates will eventually impact growth

Higher interest rates impede economic growth by increasing the cost of borrowing, discouraging investments and reducing valuations. The economy tends to experience the full consequences of tightening monetary conditions with a notable lag, indicating that the onset of a recession may only now be starting to emerge.

Historically, the lag from first US rate hike to recession has averaged 18 months to fully impact spending patterns and prices, but it has been up to 29 months. Considering this, it’s too soon to declare victory and an ‘immaculate disinflation’ scenario. As the Fed’s chairman, Jerome Powell, said in November 2022:

“It’s commonly thought that monetary policy works with ‘long and variable lags’ …There was old literature that made those lags out to be fairly long. There’s newer literature that says that they’re shorter. The truth is, we don’t have a lot of data…. It’s highly uncertain – highly uncertain.”

The window could very much still be open for a slowdown in 2024.

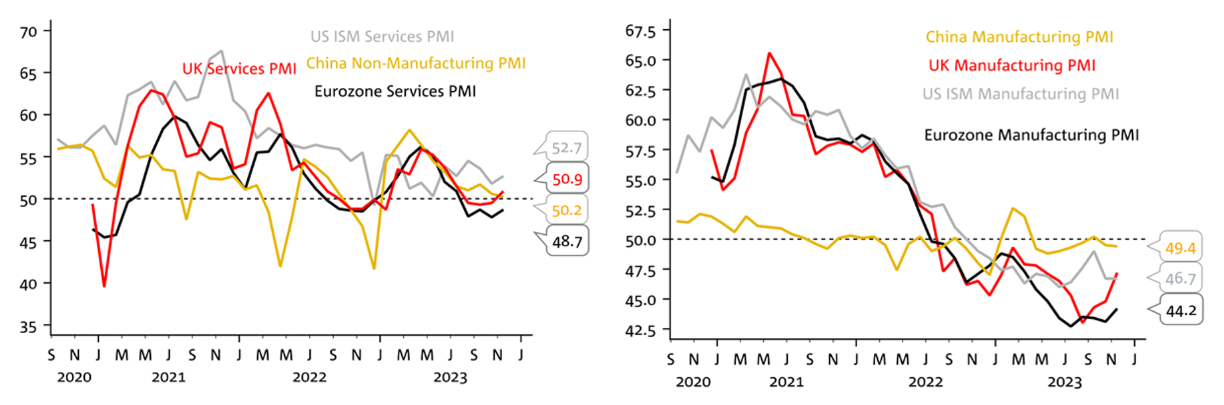

Signs of economic tension are emerging – the pace of hiring is slowing, certain borrowers are encountering financial distress, and manufacturers in advanced economies are reporting a deterioration in conditions. These can also be seen by the Purchasing Manufacturing Index (PMI) starting to go into contractionary territory in services (Eurozone) and manufacturing sectors (China, UK, US & Eurozone).

Global services and manufacturing PMI

Source: NAB

Growth and inflation’s impact on central banks’ policy rate outlook

The key to policy rate outlook is the path of inflation and where it settles, and how much post-Covid inflation will remain structural and sticky. However, the likelihood that most major developed market central banks have completed their rate-hiking endeavours is high.

Although the Fed and ECB appear to have, so far, avoided a hard landing scenario in their tightening cycle, unexpected shocks or an early shift towards policy easing could revive inflation and potentially lead to a hard landing. Conversely, more monetary tightening could induce a downturn just as the effects of previous tightening are being felt.

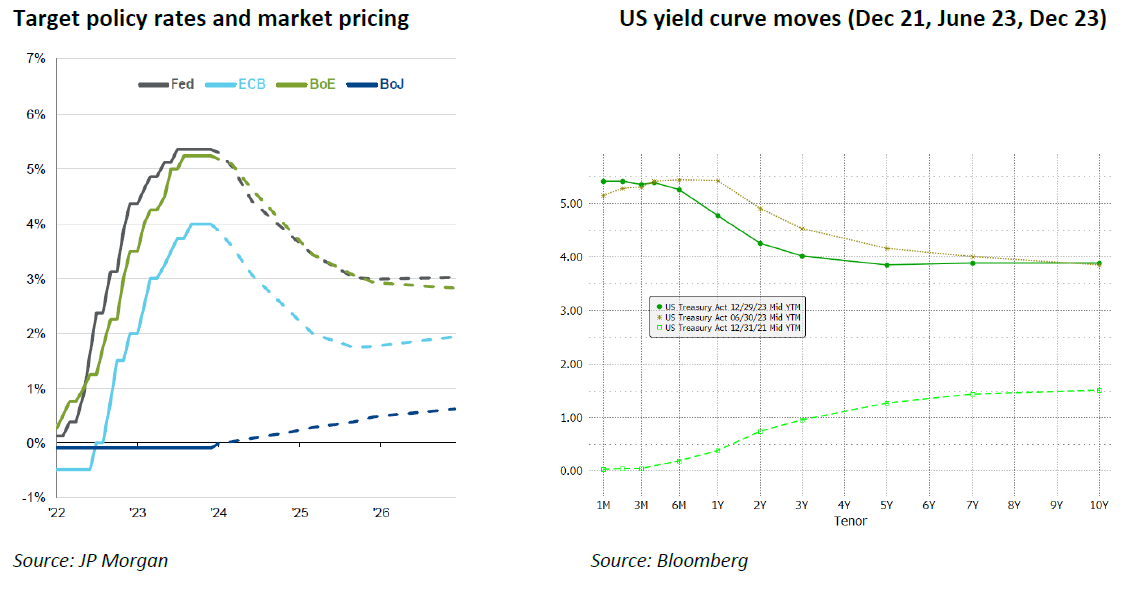

Worryingly, with inflation moderating faster than expected in the US and Europe, expectations of sizeable rate cuts have already been priced in by the market for 2024. As at time of publication:

- c150bps worth of cuts priced for the US Fed in 2024, with the first cut in March priced at 63%.

- c150bps for the ECB, with the first cut 74% priced for April.

- c130 bps for the BoE with the first cut 64% priced for May.

- In contrast, BoJ could start to normalise and raise rates.

We believe that the market has once again got ahead of itself in pricing in such aggressive rate cuts so soon, and there is a high chance of rate cuts being pushed into the second half of 2024, as central bankers wait for a more sustained period of lower inflation, which should structurally settle higher than pre-pandemic periods. We feel that the Fed is likely to cut rates faster only with a substantial economic slowdown, which is certainly not predicted in growth forecasts as yet (even if slowing compared to 2023).

Bloomberg consensus economic data/forecasts for key 4D countries – The Goldilocks scenario

Source: Bloomberg, 4D. 2023 is actual or consensus for final quarter if not released

In our view, the macroeconomic challenge for 2024 is one of perfecting the descent from the highest interest rates in a quarter of a century – continuing the path of disinflation towards central bank targets without being excessively contractionary for too long to cause a hard landing. As shown above, so far, the market is pricing in a soft landing in the US, core inflation back to target band and March rate cuts – a Goldilocks outcome – if we get there. We are not as optimistic.

In Europe, growth remains more sluggish, and is at a higher risk of disappointing, with lingering effects of higher energy prices, weak global manufacturing, and stickier inflation. China disappointed post re-opening and its economic outlook has longer-term structural issues to work through, especially in the property sector. Regardless, China remains the largest contributor to global growth and will be driven by government stimulus in the short term. 2024 will again be a year of divergent economic data points in key regions, as discussed in the Appendix.

Geopolitics: 2024 is an election super cycle

Geopolitical risks have spiked and are set to only become more important and unpredictable in 2024, with the highest geopolitical risk in decades compounding economic uncertainty. This is due to election cycles, trade tensions and armed conflicts.

- Elections: there is a busy election calendar in 2024, with 40 nations scheduled to go to the polls, including four of the five most populous countries, covering 40% of the world’s population and GDP. Elections bring instability to both domestic developments at the policy level, as well as global consequences. Key dates to watch include:

- February sees presidential elections in Indonesia after a successful decade under Joko Widodo. It’s set to be a three-pronged race, with a potential run off in June and a new government in Oct.

- March 17 sees Russia go to the polls, with little surprise expected, while Ukraine’s planned March 31 presidential vote is likely to be postponed due to martial law.

- April/May sees India go to the polls, with Modi trying to secure a third term – he is ahead in the polls at this stage.

- June sees European parliament elections and a Mexican presidential vote, which could impact trade and border security with the US.

- In the US, government debt sustainability and fiscal path are set to be key in the November election. Despite this environment, large deficits limit the prospects of fiscal giveaways. A 6 % US deficit level would suggest that whoever ends up running for president in 2024 will not be doing so on the promise of major tax cuts. Foreign policy predictability, immigration, infrastructure, the economy and continued aid to Ukraine are also important election topics.

- Sometime in Q4 (unless snap elections are called) the UK goes to the polls. The opposition Labour party is well ahead in the opinion polls and appears set for victory. Higher taxes may be on the cards, with the high levels of public debt. There is a risk that consumers and businesses take a ‘wait and see’ approach to spending and investing ahead of the election.

- February sees presidential elections in Indonesia after a successful decade under Joko Widodo. It’s set to be a three-pronged race, with a potential run off in June and a new government in Oct.

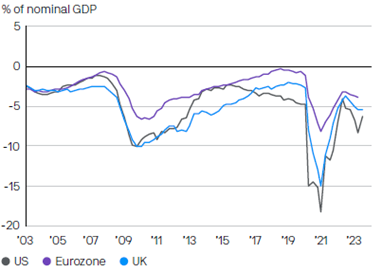

Public sector fiscal deficits

Source: Bloomberg, Eurostat, ONS, US Treasury, JPAM. As at 15 Nov 2023

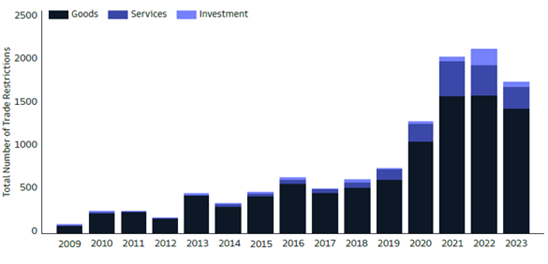

- Trade restrictions: rising geopolitical tensions could trigger further restrictions across the globe, with ‘re-shoring’ critical supply chains and economic security becoming even more front and centre of political powers. These include critical mineral inputs into the supply chains of the green energy transition.

Trade restrictions have tripled since 2017

Source: IMF, Goldman Sachs as at August 23

- Conflict: The ongoing Israel-Hamas and Russia-Ukraine wars, and China-Taiwan conflict, could all impact markets in 2024. These continue to have potential impacts on agricultural and energy markets.

- Ukraine is likely to step down as winter progresses and with lower funding from the West, but a negotiated settlement (the only way for a meaningful end to the conflict) seems highly unlikely.

- The Israel conflict is set to become a bigger issue if it is not contained to Hamas (Gaza) and Hezbollah on the southern Lebanese border. That is, if Iran has any direct role, it would impact oil prices much more, both directly and via trade through the Strait of Hormuz (20% of global supplies pass through)

- The China-Taiwan conflict continues to evolve and be front of mind early in the year. The Democratic Progressive Party (DPP) won a historic third successive term in January, but with a minority 40% of parliament (from majority) meaning it will have to negotiate with opposition parties on all legislation and budgets. It remains to be seen if the new relationship between incoming President Lai and Beijing will involve a hardening or softening of approach from either party.

- Ukraine is likely to step down as winter progresses and with lower funding from the West, but a negotiated settlement (the only way for a meaningful end to the conflict) seems highly unlikely.

- Populism: with elections, comes the rise of the populist rhetoric. Populism poses a real threat to democracies for a number of economic, social and governance reasons. From an economic perspective, the key issue is that populism leads to the development and attempted implementation of poor economic policy. This policy gets them elected, but in turn, becomes very hard to implement due to social and economic consequences.

What does this mean for infrastructure?

We remain conscious of the volatile economic environment as well as the 2024 political overhangs, and we’re positioning accordingly. However, macro uncertainty and geopolitical tensions can also create unjustified market volatility and noise. We look to separate the resilience of the infrastructure asset class from this noise, and we remain optimistic about the long-term fundamentals underpinning the infrastructure investment case.

We believe that infrastructure, as an asset class, can always play a vital role in portfolio construction due to its unique characteristics such as inflation passthrough, visible and resilient contracted or regulated earnings profiles, and exposure to numerous long-dated growth thematics.

Infrastructure also offers truly global exposure with assets across developed Asia, Europe and North America, as well as emerging markets. This allows investors to capitalise on in-country economic cycles and gain exposure to domestic demand stories. With economic trends currently diverging, certain regions offer greater relative upside at present, and we can position for this. At the moment, we started the year overweight Europe and emerging markets.

Within the infrastructure space, we also have economic diversity which allows us to actively position at a fundamental level for all points of the economic cycle, even in periods of inflation and rising interest rates, recession, and stagflation. While a diversified portfolio is always optimal, active management of the two economically diverse infrastructure sub-sectors (essential services and user pays) aims to smooth the volatility of equity investment and market cycles. We believe infrastructure is truly unique as an asset class in offering this portfolio flexibility.

Through 2023 we were overweight user pay assets and inflation, remaining underweight the utilities that could not pass through inflation or the interest rate moves. This is how we ended 2023. Moving into 2024, we will be monitoring the regional economics and politics closely, and positioning ourselves to best capture these at an in-country level. At this stage we expect the following:

- Inflation to settle above the historical levels of the 2010s, and we look to compound this where possible.

- Interest rates are expected to remain higher through at least the first half 2024, so that will factor into our allocations. We also expect rate cuts in developed markets that have had very sharp rate increases, but feel the market may be a bit too aggressive with 100-150bps cuts priced in. Considering the higher ongoing inflation and deficits, long bond rates should remain elevated (10 years), i.e. US >3.75-4% even if cash rates get cut. All cuts, however, will be supportive of infrastructure assets and, in particular, the utility sector – which will see increased allocation as this plays out.

- Growth should normalise. 2023 was very strong and took everyone by surprise. Consumer is key, and the labour market not breaking is key to them powering the economy through a mere slowdown. However, we are not anticipating contraction at this point, and remain positive on the consumer, particularly in travel.

- Energy risk seems to be dissipating, with some countries positioned better than others to capitalise on/insulate from any ongoing risk. We continue to position for this through our midstream and utility exposure.

- While it’s hard to see a quick fix for China given property issues, trust / shadow bank issues, increasing savings rates and weak confidence, the market has priced this in and valuations look very cheap.

- Robust travel momentum continues to surprise, as travellers seem willing to give up other forms of discretionary spend amidst cost-of-living pressures in order to continue investing in travel and associated experiences. While we expect the pace to slow, we continue to position for solid travel demand into 2024.

- Politics is an overhang and noise can be disruptive. We favour those regions that have less exposure to this dynamic, albeit will use any market volatility around the elections as a buying opportunity should it present itself.

Outside these near-term influences, we also see five key and integrated growth dynamics within the infrastructure space that are long term, significant and completely immune to short-term economic events. We continue to position to capitalise on:

- Developed market replacement spend – our infrastructure is old and inefficient, and a failure to upgrade it could have significant social and economic consequences (health, safety, efficiency).

- The global population growth, but with changing demographics – the West is getting older, but much of the East younger. Both dynamics require increased infrastructure investment.

- The emergence of the middle class in developing economies, which offers a huge opportunity with infrastructure both as a driver and a first beneficiary of improved living standards.

- The energy transition that is currently underway – while the speed of ultimate decarbonisation remains unclear, there appears to be a real opportunity for multi-decade investment in infrastructure as every country moves towards a cleaner environment.

- The rise of technology and all the associated nuances of its use and impacts on infrastructure needs.

Conclusion

2024 is set to be a pivotal year for the global economy, as we move past peak rates, growth moderates, and inflation continues its downward path to central bank target bands. There is still a potential window open for a recession considering the “long and variable lags” of monetary policy transmission.

For now, however, the market is pricing in a goldilocks scenario where inflation settles and growth doesn’t suffer a hard landing. This last mile of disinflation could be harder to achieve than the market is hoping for, meaning that rate cuts start in the second half of the year. Either way, lower rates are a tailwind for long duration infrastructure assets which we forecast to continue to have strong earnings growth driven by multi-decade thematics.

At 4D, we continue to prioritise companies with strong leadership, defined strategic goals that integrate with a sustainability policy, strong balance sheets to support much-needed investment, and those that are best in class within their sector in building their infrastructure footprint in countries with strong economic fundamentals, balanced risks and outlooks. We believe that with active management, a listed infrastructure equity portfolio can be positioned to take advantage of the long-term structural opportunity, as well as whatever near-term cyclical events may prevail – whether they be environmental, political, economic or social.

The content contained in this article represents the opinions of the authors. The authors may hold either long or short positions in securities of various companies discussed in the article. This commentary in no way constitutes a solicitation of business or investment advice. It is intended solely as an avenue for the authors to express their personal views on investing and for the entertainment of the reader.