Despite these 2020 challenges, we remain optimistic about both the global economic outlook and the infrastructure asset class for 2021 and beyond. In this article Sarah Shaw (Chief Investment Officer and Global Portfolio Manager) and Greg Goodsell (Global Equity Strategist) from 4D Infrastructure (4D) examine the key macro issues and forces currently in play that will, we believe, lead to a positive 2021 for listed infrastructure. Infrastructure, in all its forms, will be integral to the economic recovery and returning society to ‘situation normal’. We have said it many times throughout 2020 – there is no global growth recovery without roads, railways, pipelines, power transmission networks, communication infrastructure, ports and airports.

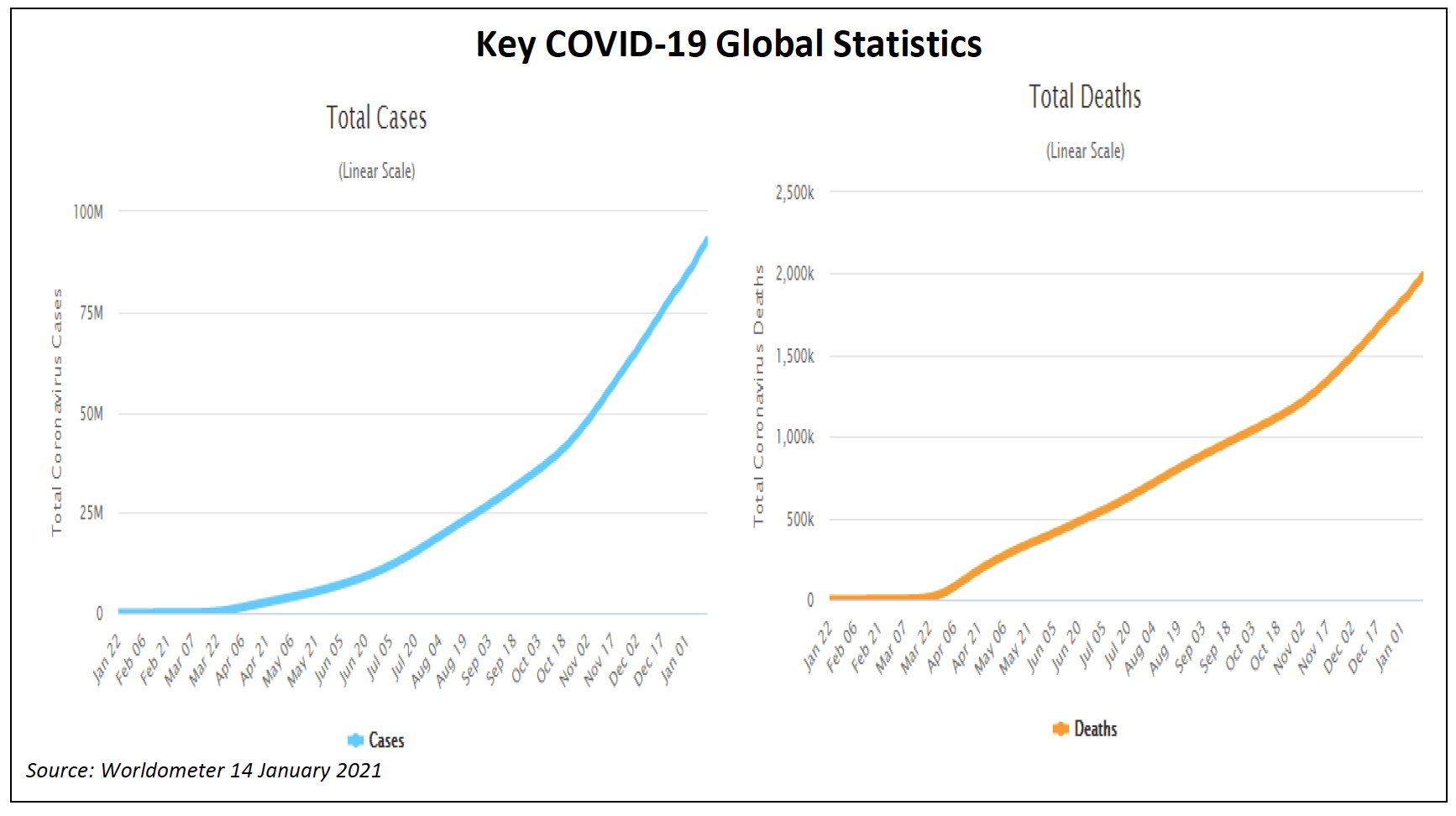

There is no doubt the COVID-19 pandemic remains the key issue impacting the economic and equity market outlook for 2021 and beyond. The virus’s continuing presence is clearly illustrated in the charts below.

Optimistic about the global economy and infrastructure asset class for 2021 and beyond

Despite the ongoing presence of the pandemic, we remain optimistic about the outlook for the global economy and the infrastructure asset class for 2021 and beyond.

Infrastructure provides basic services essential for communities to function and for economies to prosper and grow. For us at 4D this equates to the publicly listed owners and operators of essential services (regulated utilities in gas, power and water); and user pay assets (toll roads, airports, ports, rail where a user pays for the service).

These assets are characterised by:

- monopolistic market positions, or ones with high barriers to entry;

- returns underpinned by regulation or contract;

- a largely fixed operating cost base;

- high up-front capital costs and then very low ongoing maintenance spend; and

- inflation hedges within the business.

These characteristics together provide long-term, resilient and visible cash flows which underpin a yield or potential yield. It is because of these characteristics that infrastructure is known as a ‘defensive asset class’, with generally lower volatility of earnings and higher yields than broader equities. It is these attributes that attract investors, including ourselves, to the asset class.

However, listed infrastructure remains an equity and can be caught up in market volatility (as we saw in March 2020). This market volatility can present significant opportunity for investors to capitalise on the long-term infrastructure thematic (defensive characteristics with structural growth) and we believe 2021 will be such a year.

Our optimism stems from the following themes.

COVID-19 vaccines have been developed and are being deployed: a great demonstration of human ingenuity in a crisis

In our April 2020 Global Matters article (Global listed infrastructure – ‘buy’ time looming), we made the comment that ‘some of the world’s best and brightest medical research minds were focused on developing a vaccine’.

Fortunately, these efforts have borne fruit. In an endorsement of how creative humankind can be in a crisis, COVID-19 vaccines have been developed in record time and are now being deployed. This is truly remarkable and should hopefully see the currently rampant virus gradually tamed. As CSL CEO Paul Perreault said recently: ‘often a crisis breeds trailblazers and ingenuity, and the acceleration of solutions to treat and prevent COVID-19 has been truly inspirational’[1].

Huge fiscal and monetary stimulus will continue to propel global economic growth

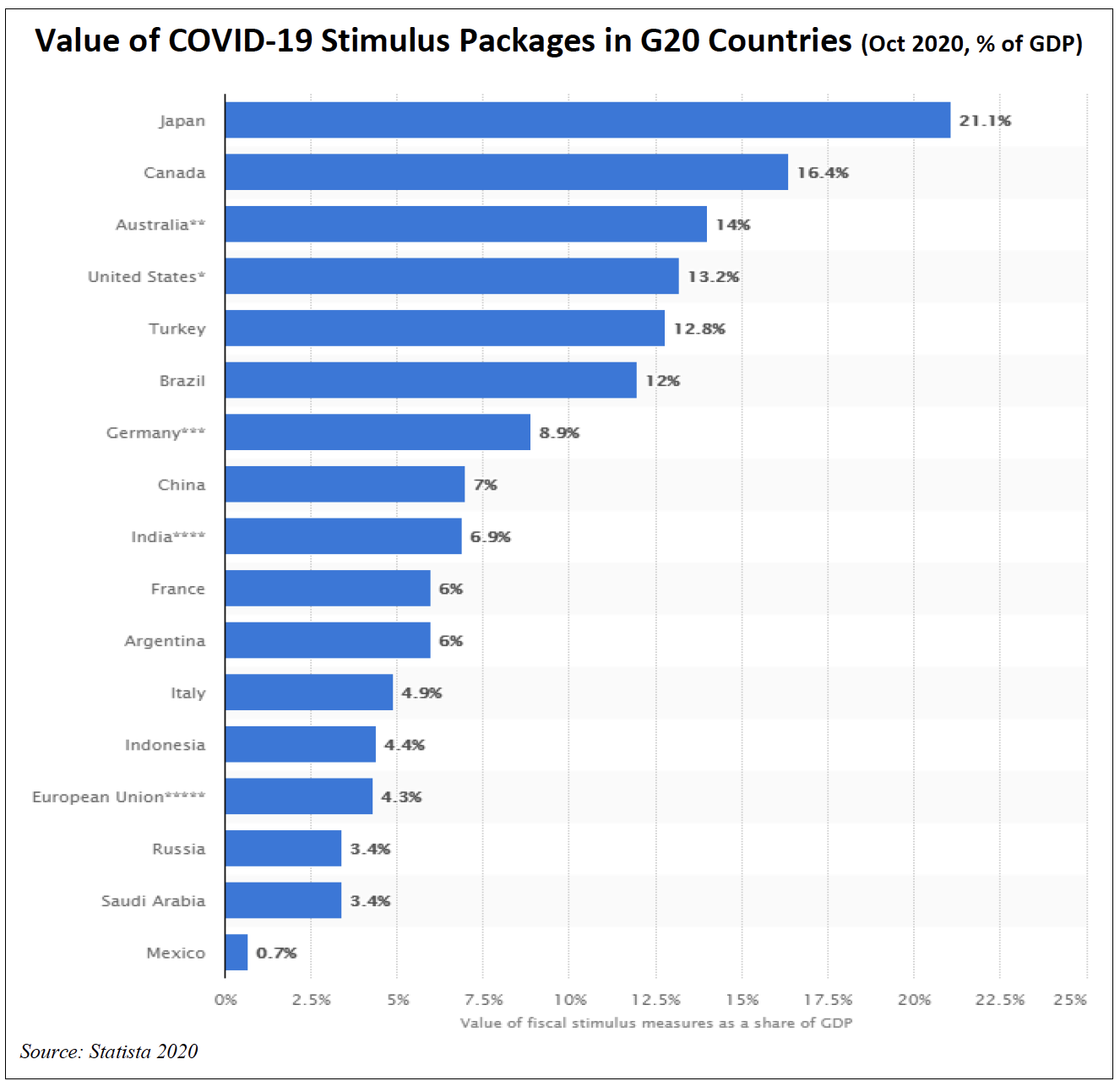

While the currently worsening pandemic will last longer than we initially hoped, we believe the global economy will ultimately emerge stronger for the experience. The huge amount of fiscal and monetary stimulus (see chart below) is still to be fully felt in economic terms with, of course, much of that spending focused on essential infrastructure investment around the globe, including the green energy transition.

The level of public sector spending and fiscal stimulus received a further, much-needed boost in December 2020 when, after months of wrangling, US lawmakers finally agreed to a further ~US$900bn package of pandemic aid, including money for businesses and unemployment programs. In January 2021 Mr Biden announced even further stimulus – see the Annexure to this paper for a brief outline.

Similarly, in Japan the Suga administration announced a stimulus package of over US$700bn in December, with parts of it set to be funded by next year’s budget. The stimulus aims at suppressing the virus while simultaneously helping the economy transition into a post-COVID world.

Also in December, the ECB boosted the size of its stimulus package and increased its bond-buying program by €500bn (now at €1.8trn), taking total monetary stimulus in 2020 to over €3trn. On the fiscal side, the stimulus package totals ~€1.8trillion euros, consisting of both the €1.1B EU budget and €750bn Next Generation EU recovery fund.

All this investment will be a strong positive for the global economy over coming years, improving efficiency, productivity and output. In addition, we believe many of the operational changes that have been forced on businesses by the pandemic will lead to a stronger, more efficient economic environment post the virus.

A substantial percentage of this fiscal spending is focused on infrastructure reinvestment and replacement. Industry participants suggest that for every $1 of infrastructure investment, an economy gets a boost of anywhere between $3-$5. That’s a significant economic boost as a result of the infrastructure investment dynamic.

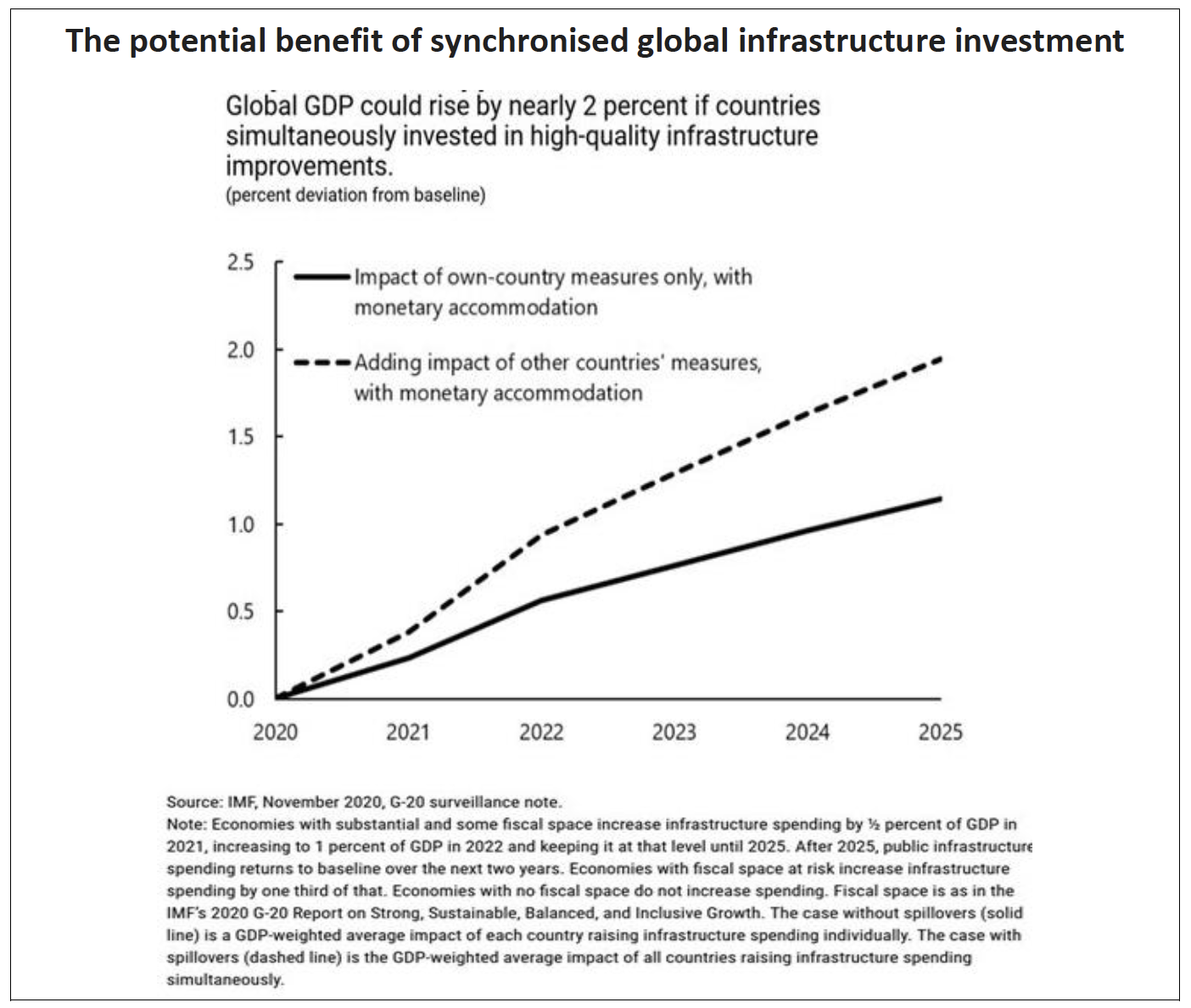

A November 2020 IMF research paper argues that a synchronised infrastructure investment push could invigorate growth, limit scarring, and address climate goals (see chart below). The IMF believes that, when many countries act at the same time, public infrastructure investment can help lift growth domestically and abroad through trade linkages. This positive ‘spillover’ effect could provide an additional boost to global output.

The IMF also argues that ‘spillovers’ created by higher demand have a greater impact when economic conditions are weak and interest rates low. When economic conditions are strong, higher government spending may push inflation above the central bank’s target and trigger a monetary policy tightening, offsetting some of the initial boost to demand. But when conditions are weak and inflation is well below target, as in the current global economic environment, monetary policy is less likely to tighten in response to higher government spending, resulting in a greater output response. The context of ample spare capacity thus amplifies the impact of both domestic public infrastructure spending and the demand that spills over from higher public investment abroad.

This is not to say we don’t expect inflation to gradually return – we want it to. Given the quantum of stimulus yet to flow through into the real economy, coupled with huge pent up consumption demand reflected in deposit rates having spiked through the pandemic, we do expect inflation will come back. While we will be monitoring this closely, we are currently in the camp of a gradual return of inflation with it continuing to track below target levels through 2021. As such, we don’t see central banks being forced into any drastic action such as near-term interest rate hikes. We are also of the belief that central banks will let inflation run a bit ahead of target over the short to medium term to assist in the reduction of headline government debt levels. However, it is worth reiterating that inflation can be positive for infrastructure assets and in particular the recovery names in the user pay space (see further discussion below). In an inflationary environment these assets will enjoy the perfect storm over the short/medium term – namely low interest rates to support future growth, economic activity flowing through to volumes, and explicit inflation hedges through their tariff mechanisms to combat any inflationary pop we may experience.

Increased public sector infrastructure spending is a clear positive for the listed infrastructure sector as it:

- boosts economic growth and labour efficiency, which is good for all businesses but especially those infrastructure businesses which form the ‘arteries’ of an economy;

- creates potential new opportunities for the private sector to co-invest alongside government or invest in place of governments; and

- on a longer-term basis, potentially provides a bigger pool of privatisation candidates.

We are not alone in our positive economic outlook for 2021, with the IMF also predicting an economic recovery in 2021 as shown in the table below.

A Joe Biden presidency should see a more stable, traditional form of governance

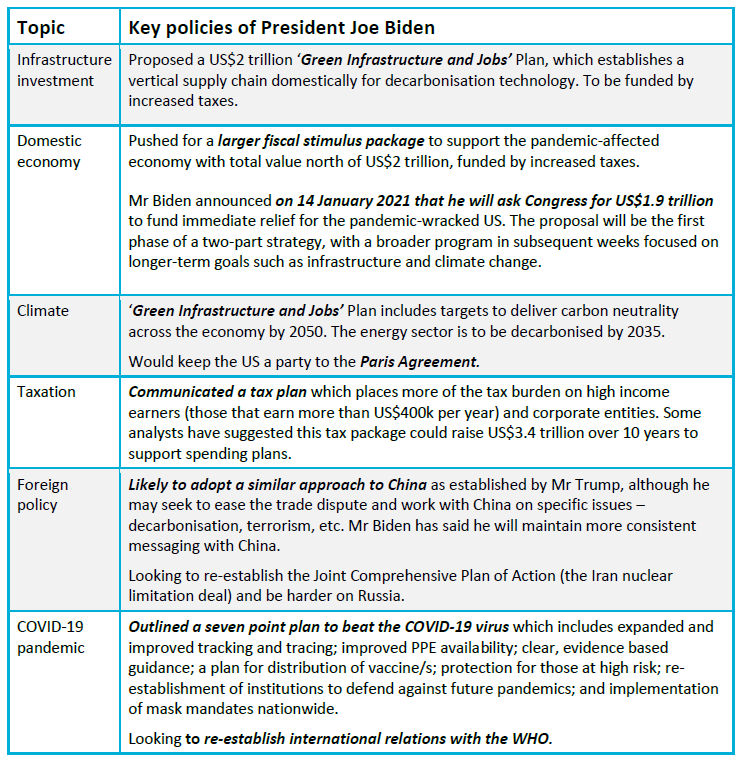

The November 2020 election of Democrat Joe Biden as US President should herald a more ‘traditional’ form of presidency, with properly developed and articulated policy returning as the mainstay of political discussion and debate.

One of the few policy areas Democrats and Republicans do agree on is the need for large-scale US infrastructure spend to both stimulate growth and replace an aged asset base.

However, as the Democrats will now control US Congress, the market will be closely watching the roll-out of Mr Biden’s policy platform, a summary of which is included as an Annexure to this paper. A more detailed analysis can be found in our October 2020 Global Matters article: US presidential election: What policy means for infrastructure investment. On balance, we believe the Biden policies are very supportive of the infrastructure asset class and managing climate change. However, we will be monitoring closely the market’s evaluation of those Democrat policies the market was concerned about prior to the election (such as the big increases in taxes).

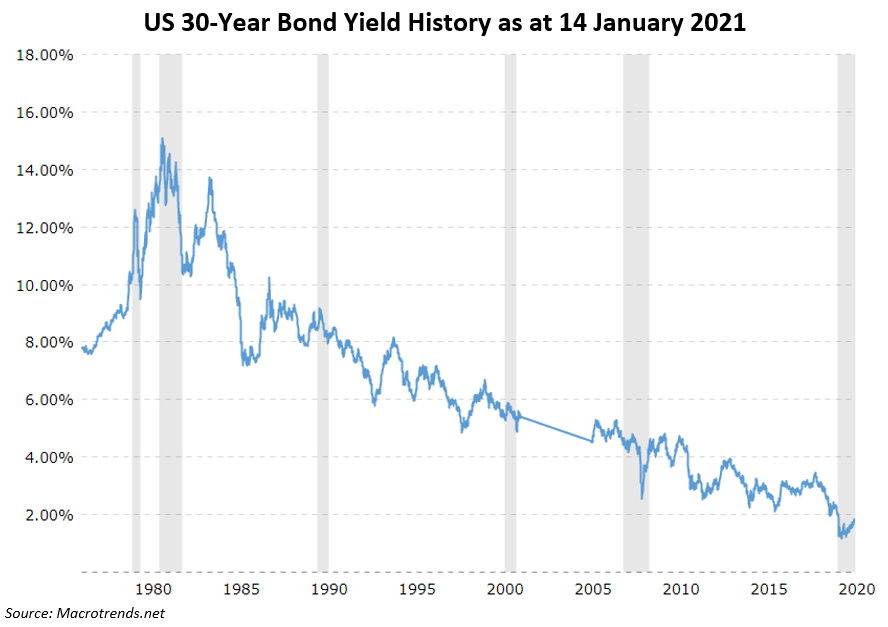

Interest rates lower for longer: very positive for the infrastructure asset class

Of all the equity market sectors, infrastructure is one of the most closely correlated to movements in market interest rates. We have published several articles on the correlation between interest rates and infrastructure asset values, particularly in a rising interest rate environment. However, at present we look to be in a lower-for-longer scenario as illustrated in the following chart of the yield on 30-year US Treasury Bonds over time. Clearly the trend in yields over the past 40 years has been down, and there is no present indication of a significant near-term reversal.

While a low interest rate environment will benefit all equity asset sectors, it will be particularly beneficial to infrastructure because:

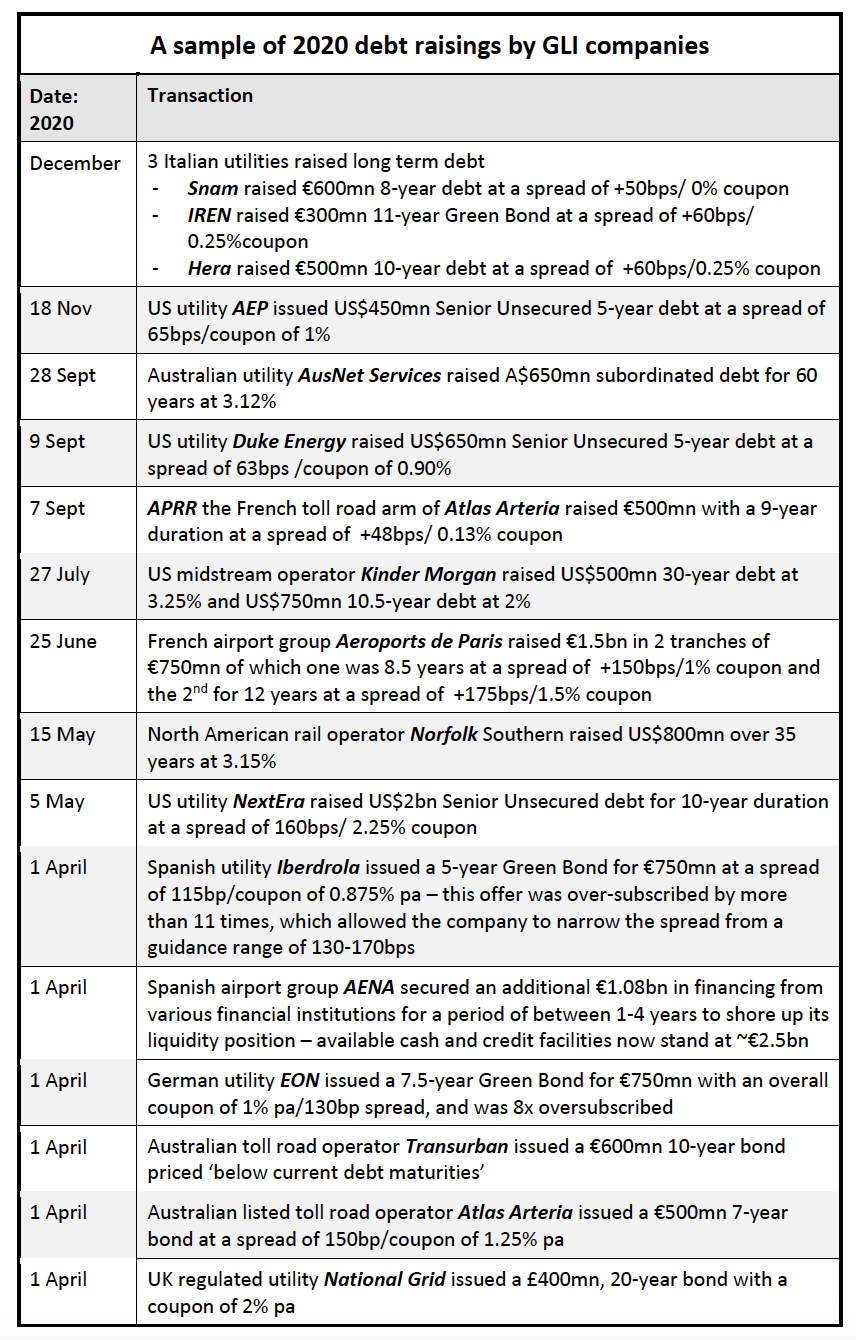

- Infrastructure companies commonly employ larger amounts of debt in their capital structures. This is principally driven by the sector’s key characteristics (discussed above) which makes it a ‘natural’ match with a more highly geared capital structure. In the current environment, with record low interest rates, we expect infrastructure companies to continue to take advantage of this historic scenario of low interest rate long-dated debt.

Some recent examples of this are set out in the table below.

- Discounted Cash Flow (DCF) valuation methodology is the core methodology employed to value infrastructure assets. This is typically the case as the long duration of infrastructure investment and the maturity profile of their cashflows makes them ideally suited to being valued using long-dated DCF analysis. This methodology utilises a Weighted Average Cost of Capital (WACC) concept as the key variable linking all those years of cashflow together. A core component of any WACC calculation is the Risk Free Rate used, with this rate a function of current market interest rates. If lower market interest rates prevail for longer, infrastructure investors gradually recognise this and reduce the assumed Risk Free Rate in their DCF’s WACC. All else held equal, this will lead to an increase in asset values as the lower WACCs flow through, providing a higher NPV of the cashflows.

The long-term, structural opportunity for infrastructure investment remains intact

Despite the chaos caused by COVID-19, we believe the longer-term infrastructure investment opportunity remains intact. Infrastructure offers defensiveness with economic diversity. These attributes, coupled with a significant growth pipeline, create a very attractive long-term thematic for the sector despite the near-term concerns of COVID-19. There is a huge and growing need for infrastructure investment globally, as a result of decades of underspend and the changing dynamics of the global population.

Replacement infrastructure spend

There has been a chronic underspend on critical infrastructure in virtually every nation over the past 30 years, if not longer. This has largely been due to governments having other spending priorities. For example, during the GFC the priority was saving the global banking system – not replacing water mains. During COVID-19 governments have prioritised social support – not road repairs.

The photos below are all examples of developed market infrastructure in dire need of replacement.

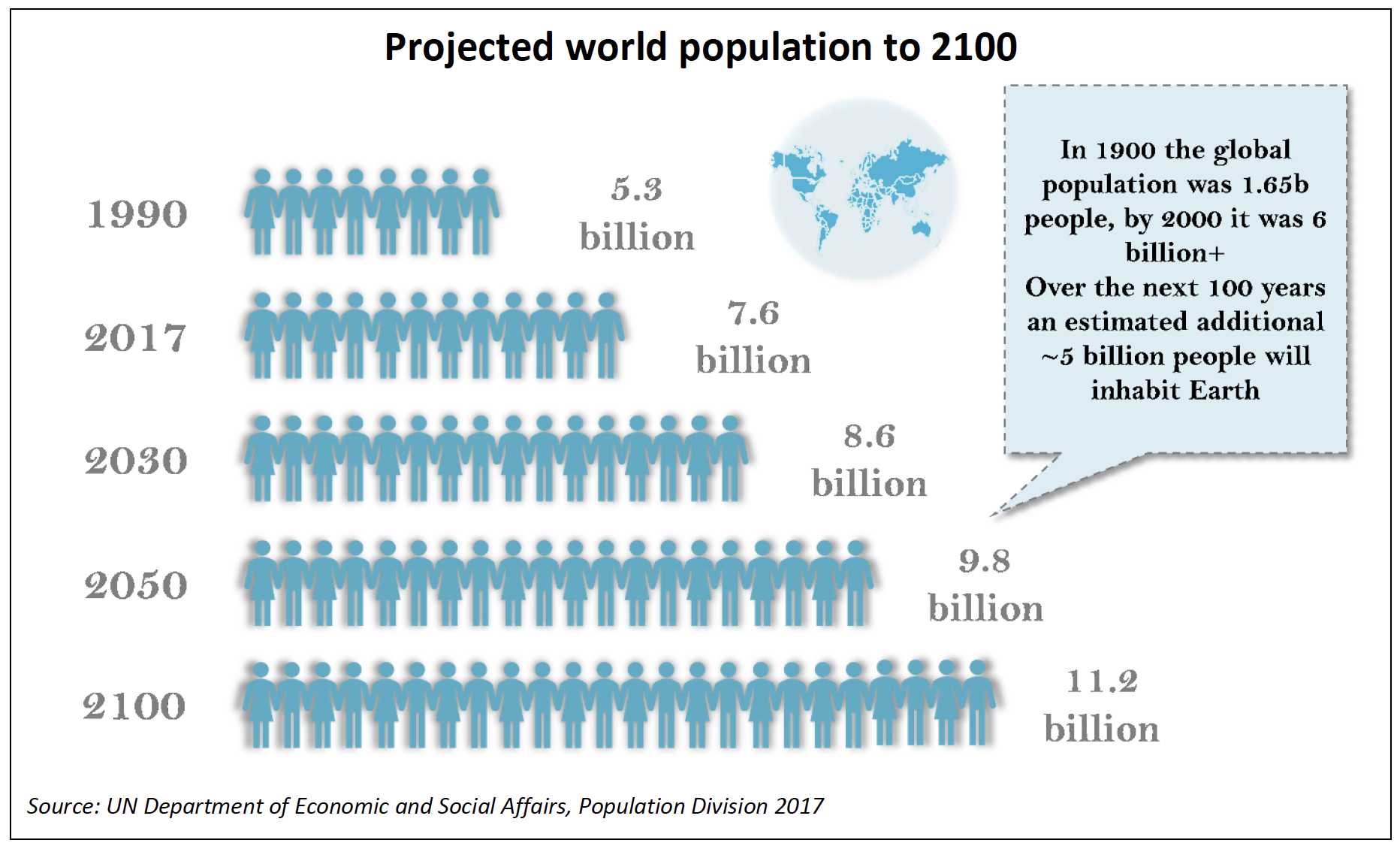

Population growth & environmental considerations

The second driver of the need for infrastructure investment is population growth. In 1900 the global population was approximately 1.65 billion people, and by 2000 that number had grown to almost 6.1 billion – keeping in mind that some of the infrastructure we are still using today was built to service that 1.65 billion. By the turn of the next century, the global population is expected to be over 11 billion, underpinning the need for yet more spend. As a society we need to first play catch-up, and then invest for the future generations.

This population growth has also raised a number of environmental and climatic challenges that underpin the need for even more spend on infrastructure to ensure the sustainability of the planet. As discussed in our October 2020 Global Matters article Decarbonisation and the infrastructure investment opportunity, infrastructure investment is core to the climate solution; and without significantly increased investment in infrastructure, the globe has no chance of reaching the Paris Agreement goal of Net Zero carbon by 2050. While the speed of ultimate decarbonisation remains unclear, there appears to be a real opportunity for multi-decade investment as every country moves towards a cleaner environment. Energy transition and decarbonisation of the power sector is an obvious thematic and will have the greatest impact on countries looking for Net Zero. However, other forms of infrastructure, namely transportation, also have a key role to play.

Demographic trends support infrastructure investment

Longer-term global demographic trends further support the infrastructure asset class and the need for investment. While the COVID-19 pandemic may lead to a temporary pause in these thematics, we believe they will re-assert themselves once the crisis is behind us.

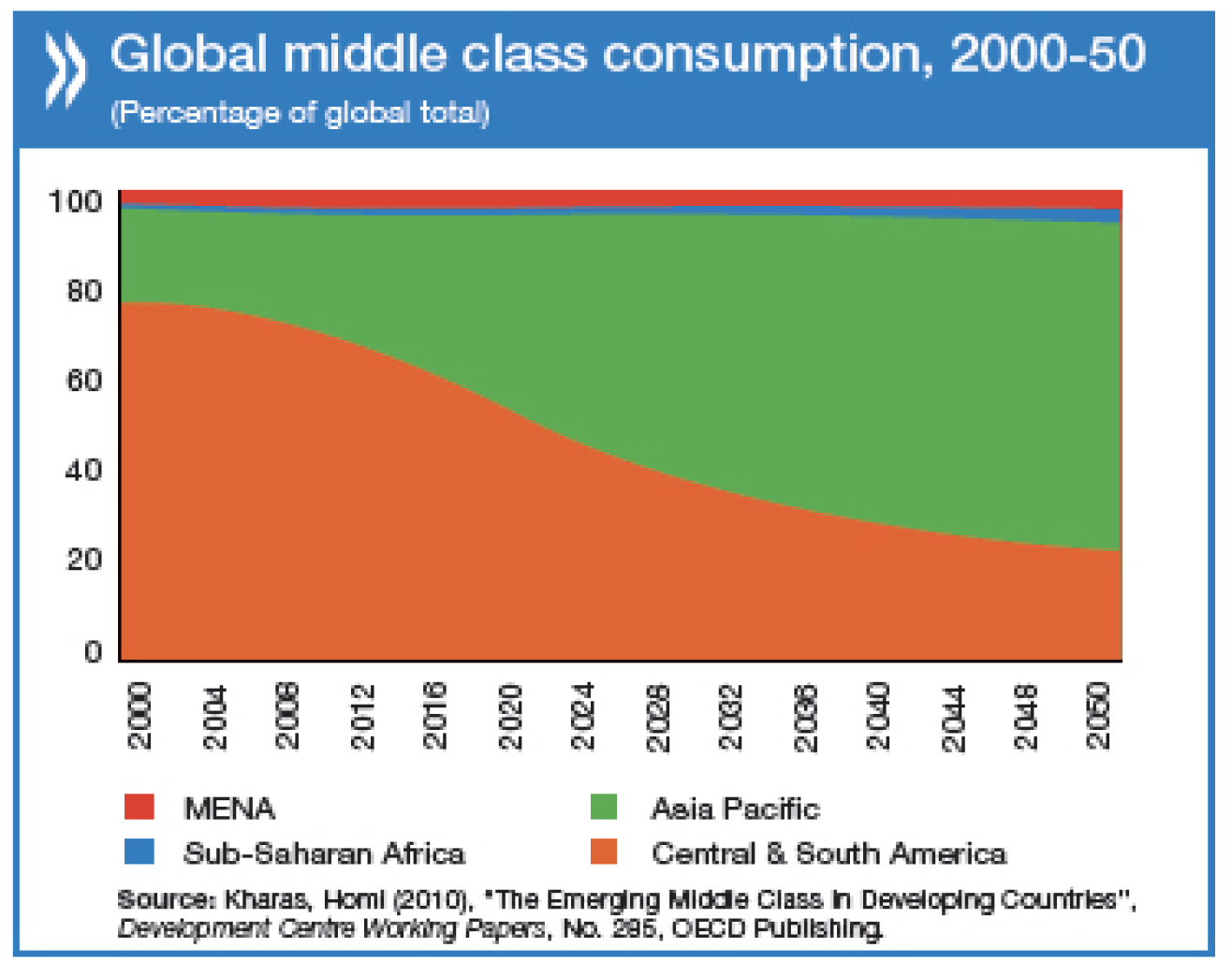

The emergence of the middle class, particularly in emerging markets (EMs), is a theme 4D finds exciting and one we believe will provide enormous opportunity for investors. Given the potential size of the middle class in EMs (China, India and Indonesia alone account for 40% of the global population), changes in spending and consumption patterns will have significant implications for global business opportunities and investment for decades to come.

Importantly, one of the clear and early winners of the emergence of the middle class is infrastructure, which is needed to support the evolution.

When you combine all these factors (i.e. developed market replacement spend, population growth (largely driven by the EMs), environmental considerations and the emergence of the middle class in EMs, the need for global infrastructure investment over the coming decades is clear. It is also clear that governments, the traditional providers of infrastructure, are simply not going to be able to fully fund this need – thereby creating a huge investment opportunity for the private sector over the coming years. That opportunity is a key thematic to which investors can gain exposure, and a thematic not derailed by COVID-19 – in fact, it is in all likelihood enhanced.

Current investment opportunities in the sector are very attractive

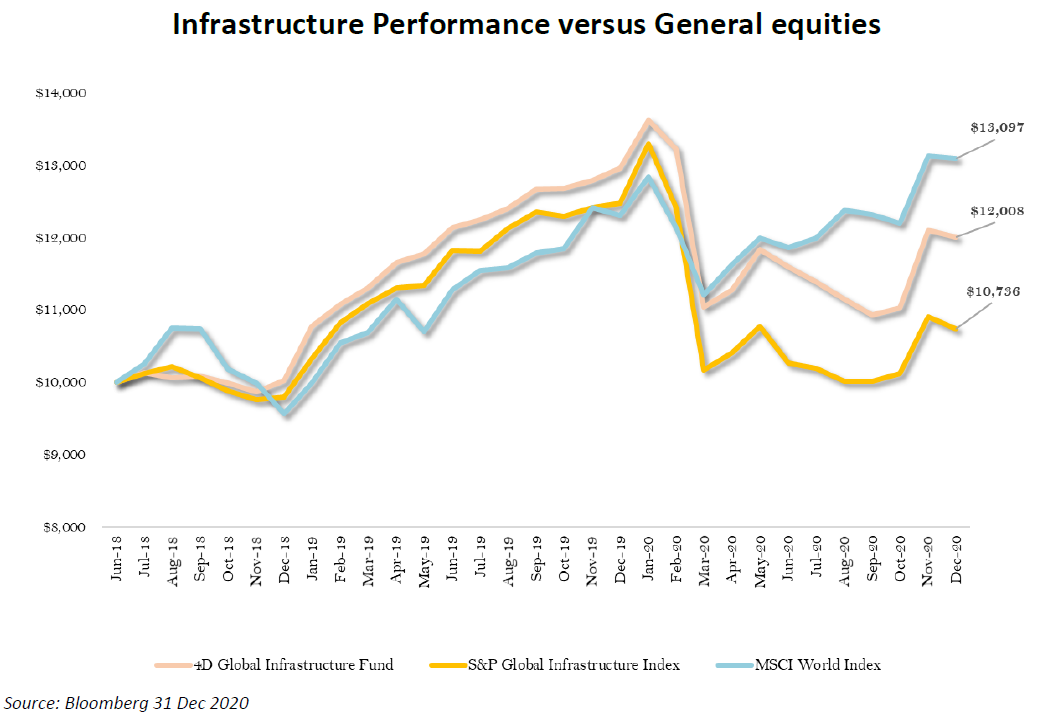

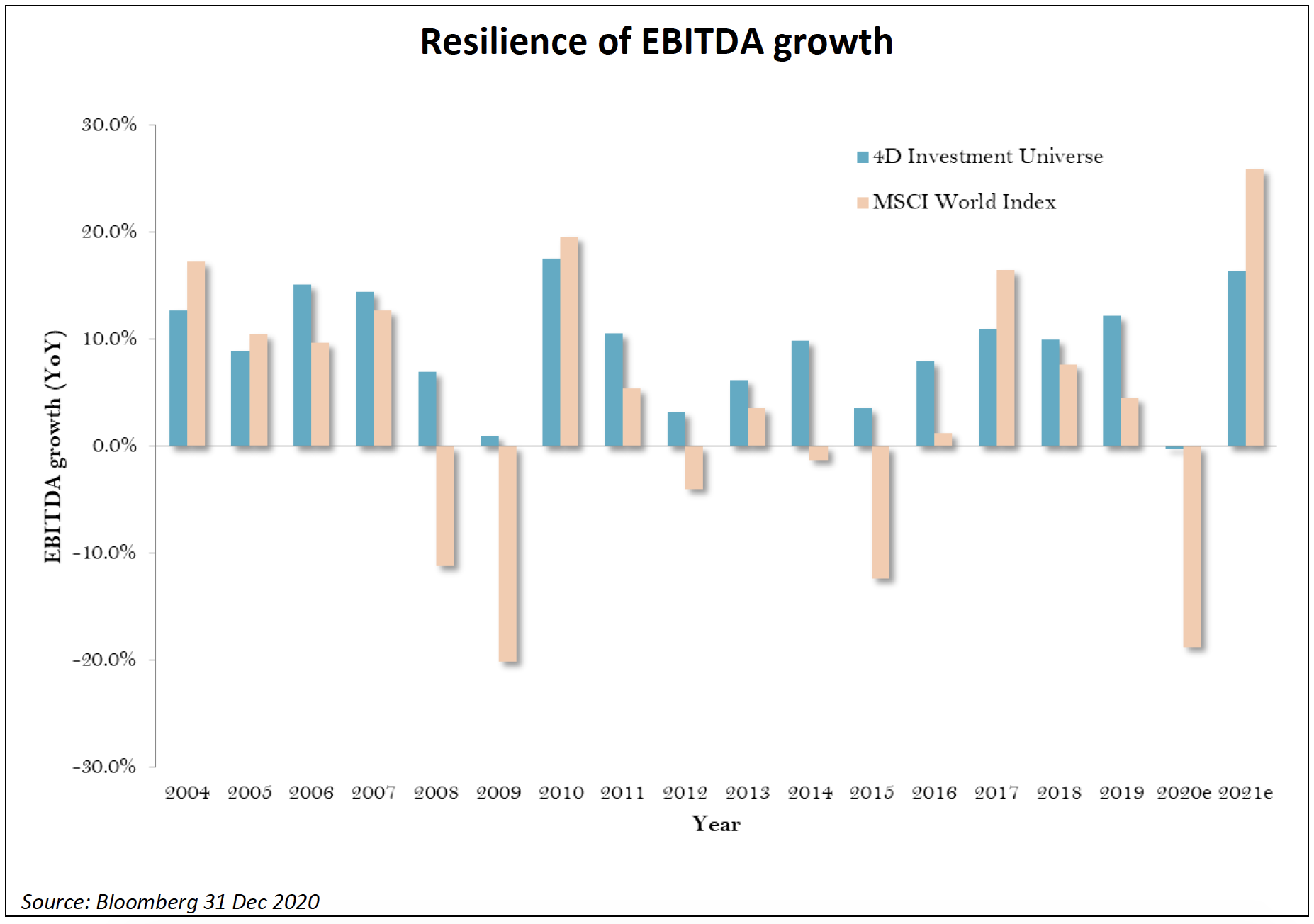

COVID-19 pushed an otherwise generally robust international economy into recession and saw the global equity market collapse. As an equity asset class, listed infrastructure was not immune to the COVID-19 market selloff. Unfortunately infrastructure hasn’t, as yet, fully participated in the subsequent cyclical market bounce as depicted in the chart below. We believe this has created a very attractive and unique investment opportunity in global listed infrastructure.

Separating the equity market moves from the investment fundamentals, the earnings of the asset class have proven to be far more resilient than the share price sell-off implies. Through a tumultuous 2020, the asset class has proven its defensive characteristics with solid earnings momentum underpinned by strong balance sheets. The chart below depicts EBITDA growth expectations for the infrastructure sector (including the hard-hit airports) and the broader equity market. The MSCI World is expecting an EBITDA contraction of close to 20% in the 2020 earnings year relative to infrastructure’s flat. At the same time the MSCI World index has fully recovered from its March lows, ending 2020 +5.8% for the full year while infrastructure has lagged with the indices finishing the year down 12-15%[2] in AUD.

This is a significant disconnect and, we believe, it is only a matter of time before the market recognises the infrastructure opportunity.

To better describe the current opportunity offered by the listed infrastructure asset class, we have briefly revisited some of the key features and core themes that support the investment thesis in the current environment.

Firstly, infrastructure comprises two quite distinct and economically diverse subsectors.

- Essential Services are the regulated utilities in the power, gas and water space. These assets are largely immune to economic shifts (up or down), as a function of them being:

- a basic need; and

- the structure of their regulatory/business environment, which means returns are measured independent of volumes.

These assets are more ‘bond proxy’ in nature, particularly over the shorter term. They are more immediately adversely impacted by rising interest rates/inflation and are slower to realise the benefits of economic growth. At the same time, they are less exposed to economic contraction and benefit from lower interest rates. These assets are attractive overweight portfolio positions in depressed economic environments as they can offer earnings growth and yield support, even in a year like 2020.

Indeed, over the past few months utility companies around the world have largely reiterated their full-year earnings guidance and dividend policies, despite the COVID impact. Fundamentally, they are holding up as expected (very well) and we did increase our exposure in April 2020.

- In contrast, User Pay assets such as airports, toll roads, rails and ports are positively correlated to GDP growth and inflation. These stocks capture GDP growth via volumes, but with inflation protection through their tariffs. As such, these assets are well suited to growth environments or the recovery phase of an economic cycle.

User Pay assets will see sharp earnings shifts this year, particularly in the airport space. But even in their case, the negative valuation impact of a harsh 2020 does not justify the share price falls that we have seen to date. Many of these User Pay assets are offering significant fundamental value at these price levels and we believe they will rebound strongly as vaccines come into play – pent-up demand for travel is huge. Further, as discussed above these assets are well positioned for any return of inflation with explicit hedges in tariffs and direct correlation to economic activity. As such we remain overweight.

Secondly, infrastructure investment also offers geographic diversity. This allows investors to capitalise on in-country domestic demand, in-country stimulus and position accordingly. To this end we are currently overweight Europe and EMs.

Finally, as discussed above the structural infrastructure growth opportunity remains intact. The advent of COVID-19 hasn’t changed this dynamic. We believe the long-term infrastructure investment themes have actually been enhanced by the current pandemic – government stimulus programs are fast-tracking infrastructure investment, increasingly stretched government balance sheets will see a greater reliance on private sector capital, and a ‘lower for longer’ interest rate environment is supportive of infrastructure investment and valuations.

Meanwhile, solid well-managed infrastructure companies are in robust financial positions. Balance sheets were in strong starting positions, and few have reported any liquidity issues as a result of COVID-19. Management teams are also taking advantage of open credit markets and low market interest rates to secure attractive, long-dated debt financing to ensure ongoing liquidity and support growth profiles (see previous table ‘Recent debt raisings by GLI companies’). Despite near-term uncertainty around economics and the duration of the pandemic, the underlying fundamentals of these assets remain attractive to debt investors, which should go some way to reassuring equity investors. This is particularly true given that, during the GFC, debt markets were generally far better indicators of pending market problems than were equity markets.

We believe the combination of attractive investment fundamentals, long-term structural thematics that remain intact, the COVID-19 response and currently very attractive stock prices represents a unique buying opportunity for listed infrastructure – an opportunity we are looking to capitalise on as we move into the economic recovery phase and a hopefully prosperous 2021.

What could derail our outlook?

While we are optimistic regarding 2021, there is no doubt 2020 has been a tumultuous year. There are a number of residual factors that could adversely affect our view, including:

-

whether the COVID-19 vaccine(s) are effectively deployed globally, and in a timely manner, delivering the expected health benefits leading to subsequent economic recovery;

- governments and central banks prematurely take their feet off the ‘go’ pedal before the global economy has the opportunity to properly get back on its feet;

- the actual shape of the economic recovery, which is crucial, remains to be seen (V, U, L or W);

- President Biden is unable to make diplomatic progress and we see renewed Chinese/US tensions on a variety of issues: trade, Hong Kong, South China Sea, COVID-19 origins.

- a ‘hot’ India/China confrontation emerges;

- longer-term attention will turn to how all the massive global fiscal stimulus, much of which will be sourced from central banks, is paid for;

- the question of whether ‘Modern Monetary Theory’[3] will earn its stripes; or will too many dollars chasing too few goods see currencies devalue and inflation escalate (‘Monetarism’[4] and Milton Friedman’s economic theories)?; and

- whether inflation comes back faster than anticipated, forcing central banks to act ahead of plans through increasing interest rates

Conclusion

Despite a tumultuous 2020, as infrastructure investors we remain excited about the listed infrastructure investment opportunity in 2021 and beyond. The combination of infrastructure’s attractive fundamentals (supporting earnings resilience), the economic and geographic diversity within the sector and prevailing long-term structural thematics (e.g. the emerging middle class in EMs and the green energy transition to renewables), represent a unique investment opportunity in listed infrastructure. We believe this opportunity has actually been enhanced by the current pandemic – government stimulus programs are fast-tracking infrastructure investment, stretched government balance sheets will see a greater reliance on private sector capital, and a ‘lower for longer’ interest rate environment is supportive of infrastructure investment and valuations.

As noted at the outset, infrastructure in all its forms will be integral to the economic recovery and returning society to ‘situation normal’. There is no global recovery without roads, railways, pipelines, power transmission networks, communication infrastructure, ports and airports. Indeed, the pandemic may have actually reinforced and enhanced some of the key drivers supporting the asset class.

To receive CPD points for reading, view this article on AdviserVoice’s website and complete the questionnaire.

[1] Australian Financial Review, ‘We are more resilient and adaptable than we ever imagined’, 18 Dec 2020

[2] FTSE Global Core Infrastructure Index -12.6% in AUD, Dow Jones Brookfield Global Infrastructure Index

-15.2% in AUD and the S&P Global Infrastructure Index -14.8% in AUD on a 1 year view to 31 December 2020

[3] Modern Monetary Theory (MMT) is a macroeconomic theory that, for countries with complete control over their currency, government spending cannot be thought of like a household budget. Instead of thinking of taxes as income and government spending as expenses, MMT proponents say that fiscal policy is merely a representation of how much money the government is putting into the economy or taking out. This means that any government spending can be paid for by the creation of money, with the purpose of taxes being to limit inflation, by controlling the money supply. This means that spending shouldn't be determined by deficit levels, but by whether or not spending is keeping the economy at full employment and at a reasonable level of inflation. (Investopedia)

[4] Monetarism is an economic school of thought, which states that the supply of money in an economy is the primary driver of economic growth. As the availability of money in the system increases, aggregate demand for goods and services goes up. An increase in aggregate demand encourages job creation, which reduces the rate of unemployment and stimulates economic growth. However, in the long-term, the increasing demand will eventually be greater than supply, causing a disequilibrium in the markets. The shortage caused by a greater demand than supply will force prices to go up, leading to inflation. (Investopedia)

Annexure

The content contained in this article represents the opinions of the authors. The authors may hold either long or short positions in securities of various companies discussed in the article. This commentary in no way constitutes a solicitation of business or investment advice. It is intended solely as an avenue for the authors to express their personal views on investing and for the entertainment of the reader.