In October 2020, we published a Global Matters article titled Decarbonisation and the infrastructure investment opportunity, in which we discussed how investors wanting to be part of the decarbonisation investment thematic should look to infrastructure as a means of participating. While the speed of ultimate decarbonisation remains unclear, there appears to be a real opportunity for multi-decade investment as every country moves towards a cleaner environment. Energy transition and decarbonisation of the power sector is an obvious thematic and will have the greatest impact on countries looking for Net Zero.

That article was an introduction to the decarbonisation thematic, and set a framework for follow-on pieces exploring in more detail the infrastructure investment solutions in aspiring to global Net Zero emissions by 2050. In this article, 4D’s Investment Analyst Tasneef Rahman looks at hydrogen and the potentially important role it could play in the evolving decarbonisation thematic, with Europe leading the charge.

What is hydrogen and how does it fit into the decarbonisation story?

Hydrogen is the most abundant naturally occurring element in the universe, accounting for ~75% of all matter. Contrary to popular belief, it is already widely used as feedstock in a number of industries, including refining and chemical production. Over time it is expected that hydrogen will become more prevalent in other industrial processes, be used in transport and mobility, and potentially even be extended into other applications such as building and residential heating.

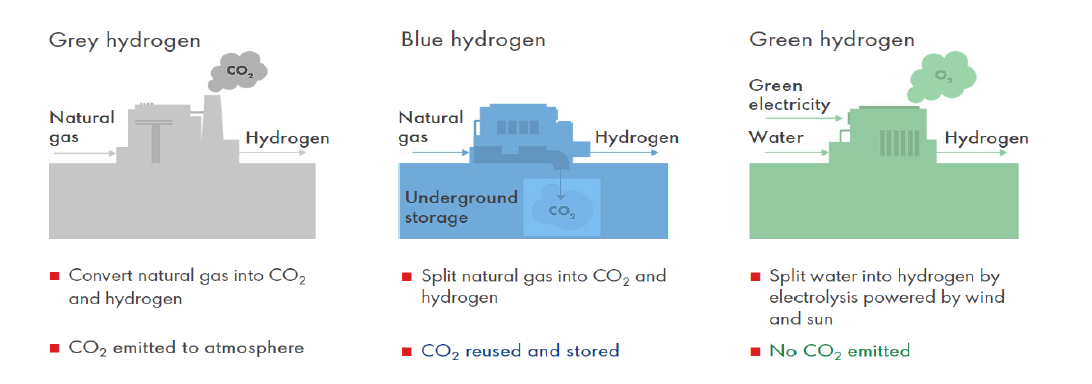

The key benefit of hydrogen is that, in today’s environmentally conscious world, it can be used without producing any carbon emissions. Nevertheless, while it is emissions free for end use applications, until recently the process to generate hydrogen into a useable form has not been emissions free. This is where the hydrogen colour scheme comes into play.

- Grey hydrogen is currently the most commonly used form of hydrogen. It is produced using fossil fuels (mainly methane) and the process to convert it to a useable form has significant CO2 emissions, estimated to be responsible for 2% of all global emissions[1].

- Blue hydrogen is produced in the same way as grey, but the process employs carbon capture and storage, which reduces the CO2 emissions relative to grey by over 70%.

- Green hydrogen is produced through electrolysis (electric currents are used to separate oxygen and hydrogen in water). This process is free of carbon emissions when the electricity used to drive the electrolysis is generated from renewable sources, such as solar and wind.

Today, due to the significant cost of production, less than 2% of all hydrogen produced is green. However, recent developments indicate this will increase significantly over the coming decades. The International Energy Agency (IEA) estimates that conversion to green hydrogen could save 830m tonnes of annual CO2 emissions[2].

Source: Shell International

Why is hydrogen making a resurgence?

Hydrogen has been touted for decades as an alternative energy source. While it is prominent in a number of industrial applications, its widespread use has been limited due to more cost-efficient alternate energy sources – cheaper electricity and fossil fuels. So why is hydrogen, and specifically green hydrogen, gaining so much airtime today? The answer to this comes down to three interlinked factors.

1. Decarbonisation goals

The collective global push to reduce carbon emissions in line with Paris [3] climate goals is a key reason why hydrogen has again come to the fore.

In the shorter term, converting feedstock from grey hydrogen to at least blue hydrogen in existing industrial applications will have a meaningful impact on emissions reduction targets.

Over time, it is expected that roughly 85% of end user energy demand can be met by electrification. However, for the remaining applications/industries, electrification isn’t the most suitable nor efficient; and this is where hydrogen (particularly green) is expected to play a key role. The two key sectors where green hydrogen is the most viable solution to decarbonisation goals are heavy industry (e.g. steel, cement and chemicals – where in some instances hydrogen is already being employed) and transport (e.g. trucks, rail, shipping and aviation), where electrification isn’t viable.

Taking rail transport as an example, in Europe currently around 40% of the network still runs on diesel. [4] Electrification (by way of overhead/catenary wires) is possible but expensive, estimated to cost around €1.5m/km. [5] In Germany, where over 100,000km of track is yet to be electrified, this amounts to over ~€150bn – a massive outlay which would ultimately be borne by the end user. This is why other low carbon alternatives, such as battery and hydrogen powered trains, have started to gain traction. As explained by leading train producer Alstom, these two technologies are often seen as complementary, with ‘battery solutions generally more suitable in short and medium length non-electrified sections’ and ‘hydrogen solutions best to use when range is key’. [6]

Meanwhile heavy industries, including steel and cement production, are hugely reliant on fossil fuels (mainly coal) for combustion and heat generation for their industrial processes. As such these industries have massive carbon footprints, collectively accounting for over 15% of all global emissions. [7] Hydrogen’s potential to displace this fossil fuel use in these industrial processes can therefore have a significant impact on decarbonisation goals.

Finally, green hydrogen can potentially be used for storage, whereby excess renewable electricity not supplied to the power grid can be converted to hydrogen and stored for later usage – with potentially greater capacity than batteries.

2. Government policy support

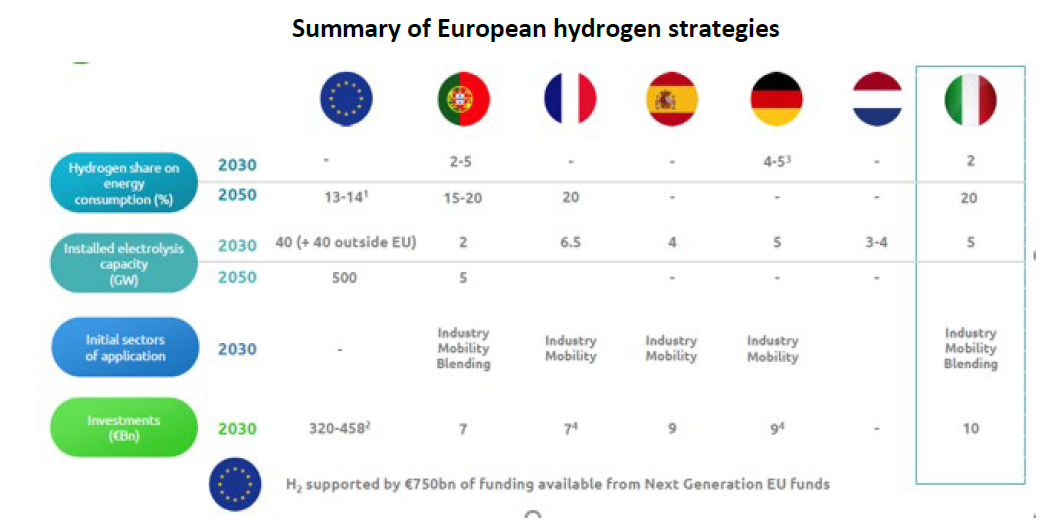

Europe is at the forefront of the energy transition, with goals of climate neutrality by 2050 as part of the European Green Deal. This commitment to the energy transition is reflected in the EU’s 7-year €1.1 trillion budget and €750bn Next Generation EU recovery plan[8], both of which are strongly focused on green investment to fight climate change.

Near-term environmental targets aim for a 32% share for renewable energy in the generation mix and a 55% cut in greenhouse gas emissions by 2030 (from 1990 levels).

In support of these goals, the EU has recently developed a green hydrogen strategy. It targets 40GW of electrolyser capacity by 2030, a massive jump from ~60MW today, at an estimated cost of €24-42bn. The strategy also envisages €11bn of spend on adding carbon capture and storage technologies to existing grey hydrogen plants (effectively converting them to blue hydrogen). Over €60bn of investment is also planned for transport, distribution, storage, and refuelling stations.

Subsequently, almost all the major economies in Europe have developed their own individual strategies (or at least draft strategies) in conjunction with this wider EU objective. Out of the 40GW target, over 25GW of this goal has been met by the aggregate electrolyser capacity targets of Portugal, France, Spain, Germany, Netherlands and Italy.

The regions / countries above are EU, Portugal, France, Spain, Germany, Netherlands, Italy.[9]

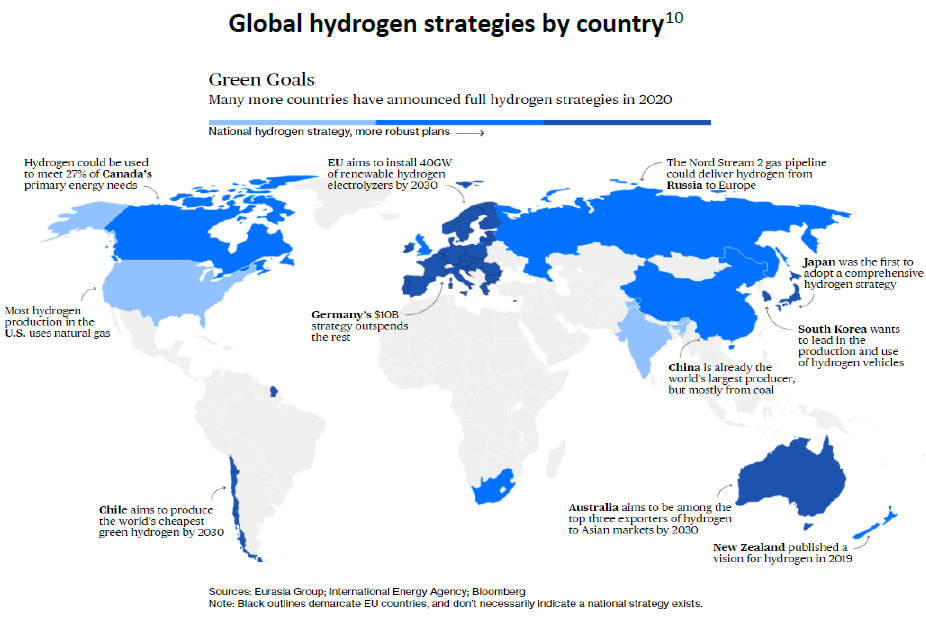

Even outside Europe, other developed countries including South Korea, Japan and Australia, and even less developed nations such as Chile, have formulated their own hydrogen agendas. The diagram below highlights countries that have announced hydrogen strategies, with darker shades of blue indicating more developed plans.

Focusing on Europe, funding from both the Next Generation EU fund (in the form of grants and loans) and the EU budget will provide extensive support to companies prioritising the energy transition, including those with hydrogen agendas. Similar to government subsidies and accommodative policy propelling the renewables boom, supportive hydrogen policy is expected to do the same.

3. Green hydrogen costs and their drivers

Like many new technologies, cost is still the most critical factor for more widespread green hydrogen adoption. Cost reduction by way of technology improvement is what will ultimately make green hydrogen more viable and competitive versus other fuels.

Corporates are under increasing pressure from governments and environmentally conscious stakeholders to reduce their carbon footprints. Anticipated cost reductions will make green hydrogen a genuine alternative to grey hydrogen and, over time, other power sources.

There are two key components of the cost of green hydrogen – renewable electricity and electrolysers.

Cost of renewable electricity

Given the need for renewable electricity in green hydrogen production, its cost is a significant factor in the overall cost of green hydrogen.

Over the past decade renewable energy costs have dropped dramatically, with an estimated 82%, 47% and 39% cost reductions for the key technologies of solar photovoltaic (PV), offshore and onshore wind respectively.[11] It looks clear that this trend is set to continue over the next decade, with further technological improvements and scale benefits. Solar PV, onshore and offshore wind costs are expected to decline a further 40%, 30% and 50% respectively; driven by lower upfront investment costs, increased wind park and solar panel efficiency, and lower operating and financial costs[12].

Cost of electrolysers – used to extract hydrogen from water

The cost of electrolysers is the second key determinant in the cost of green hydrogen production.

Electrolyser costs have fallen ~60% in the last ten years, with even steeper cost reductions observed in China. [13] Costs are expected to drop another 40-50% by 2030 due to increased economies of scale, although this is dependent on increasing volumes of hydrogen from industrial feedstock.[14] Assuming this materialises and production is scaled up from increased demand, economies of scale will develop for manufacturers. Estimates suggest this will bring electrolyser capex down by almost two thirds, from around €1,100-€1400/kw currently to around €400 by 2030.[15]

Electrolyser cost reductions are expected to parallel those seen in the solar and wind industry over the last decade. Here volume growth from increased renewable penetration, government policy support and low-cost manufacturing (particularly from China) led to rapid declines in utility scale solar panels and turbines.

Additionally, as load factors in renewable electricity generation improve this will translate into higher electrolyser load factors; which ultimately increases hydrogen generation efficiency.

Which leads to the overall cost of hydrogen

Today in Europe, both grey and blue hydrogen are estimated to cost around ~€1-2.5/kgH, significantly cheaper than green hydrogen which costs on average around ~€4-5/kgH.[16] Green hydrogen costs vary significantly with the cost of renewable energy, and are cheapest in the best renewable resource centres – e.g. those areas with lots of land, sun and wind.

If efficiencies in electrolyser and renewable technology are realised, it is estimated that green hydrogen could see total cost declines of 35-60%, tightening the range closer towards €1-2.5/kgH. This would start to make it competitive with grey hydrogen, and likely extend it further into other industries and transport.

The cost of carbon is also critical

Green hydrogen’s potential to fulfill the energy needs of hard-to-abate sectors is also heavily dependent on carbon prices. It is expected that carbon price increases are necessary to ultimately discourage fossil fuel use in heavy industry and transport – and importantly, these increases will have the knock-on effect of increasing the viability of green hydrogen as an alternative.

It is also expected that the carbon price will increase over the next decade, with the ongoing global transition towards renewables. However, the exact quantum is still highly uncertain, which in turn creates ambiguity on timelines for green hydrogen competitiveness. Here we have seen a broad range of estimates, ranging between a 3-fold and a 5-fold increase in carbon pricing required to facilitate the switch. It seems clear that technologically-driven reduced costs, combined with some level of carbon pricing, will be needed for green hydrogen to truly fulfill its potential in supporting the ‘last leg’ of decarbonisation and achievement of the Paris climate goals.

How is 4D playing the hydrogen theme?

While we agree that hydrogen will play a critical role in carbon reductions over the medium to longer term, it is unclear when and to what extent this will actually translate into material earnings for the relevant companies in our listed infrastructure universe.

A core component of our investment process is the quality of a company’s cashflows as reflected in visible contracted, regulated or GDP-correlated earnings streams. Absent this certainty, we don’t assign value to a stock’s hydrogen investments or potential future benefits from the technology. Coupled with the fact that most messaging from company management teams has been that hydrogen remains a very long-dated opportunity, with minimal earnings contribution over the next decade, we have not made any direct investments in the theme.

Instead, we continue to focus on high quality businesses that have a transparent and integrated ESG strategy and which, we believe, are trading at significant discounts to their intrinsic value, on relatively high earnings visibility. In Europe, these companies include the likes of ENEL, Iberdrola, EDPR and SNAM (all of which we own in our global portfolio), which are compelling investment opportunities independent of any hydrogen hype, but are also poised to be key beneficiaries of hydrogen success. As such, these companies – along with almost all their listed peers – have taken (or are at least starting to take) steps to benefit from hydrogen’s potential.

Utilities and renewable stocks are the key infrastructure beneficiaries from green hydrogen. Specifically, these companies are set to benefit in two direct ways:

- over the long term through core regulated asset or contract/pipeline growth (in transmission networks and renewables); and

- in the medium-term through their unregulated business units, including newly-formed hydrogen divisions and in energy supply.

Case study: renewable energy developers

For renewable energy developers such as ENEL, Iberdrola and EDPR, the most clear and immediate benefit from hydrogen energy is that it further intensifies the transition towards, and growth in, renewable energy.

This is best highlighted by the EU which states that 80-120GW of solar and wind capacity, costing approximately €220-€340bn, will be required to provide the necessary electricity for the 40GW of electrolysers they envision being in place for green hydrogen by 2030. Put simply, green hydrogen needs green electricity. Given their existing operational renewable capacity coupled with the significant renewable development pipelines these industry leaders possess, we think it is most likely that they will be structural winners from the accelerated renewable proliferation that is required for hydrogen adoption and meeting decarbonisation goals.

Additionally, as a number of the leading renewable developers operate integrated models, increased renewable proliferation has the added bonus of supporting additional investments in electricity networks and, with more electrification, increasing electricity volumes sold.

At 4D, we only value renewable pipeline capacity that has reached final investment decision (FID) stage and is generally contracted, so any additional pipeline conversion represents further upside to our valuations. To put this in perspective, ENEL (one of our top ten holdings) has secured ~10.5GW out of its three-year ~20GW additional renewable capacity target. This 20GW is also part of a wider 60GW mature stage pipeline. Our valuation methodology values only the secured capacity of 10.5GW. Therefore, if hydrogen targets do help accelerate ENEL’s growth towards the near-term 20GW target and eventually convert more of the 60GW mature stage pipeline, this should be positive for cashflows, accretive to earnings and provide further support to our valuation.

Case study – Iberdrola

Outside their core businesses, almost all of Europe’s largest listed renewable developers and utilities have started to explore new hydrogen-related opportunities.

Iberdrola, which is currently a major position in the 4D Global Infrastructure Fund, is a prime example. As one of the world’s leading renewable developers, it has one of the most ambitious hydrogen-related targets in the sector. Globally, the company is targeting over 600MW of electrolyser capacity by 2025 and 3GW by 2030, focusing on those sectors where grey hydrogen is already commonly used. As part of its strategy it is currently developing one of Europe’s largest industrial green hydrogen projects in the centre-south of Spain, which – once operational – is expected to save 39,000 tonnes of CO2 annually. The €150m project for Fertiberia, one of Iberia’s largest fertiliser companies, will use 100MW of solar PV capacity, battery storage and one of the largest electrolysers in the world (20MW). The two companies have recently expanded their green hydrogen partnership, aiming to install up to 800MW of electrolysers and 1.3GW of solar PV capacity by 2027 at a potential cost of €1.8bn euros; with plans, however, dependent on receiving adequate support from the Spanish state and European recovery funds. Further, in February 2021, Iberdrola presented to the Spanish Ministry of Ecological Transition a capex plan of €2.5bn in green hydrogen projects across 53 different Spanish projects. This proposal corresponds to 25% (1GW out of 4GW) of Spain’s target for electrolysers by 2030 and is expected to be presented as part of the Spanish proposal for the utilisation of the Next Generation EU program (discussed above).

Iberdrola has also ventured further into the hydrogen value chain. Recently it signed an MoU with NEL Hydrogen (one of the largest electrolyser suppliers and the supplier to Iberdrola’s Fertiberia project) to develop large-scale hydrogen projects, and a new venture called Iberlyser to distribute industrial-scale electrolysers to customers who have significant demand for hydrogen. As an integrated utility with strong relationships with long-standing industrial clients, the ability to offer on-site hydrogen generation plus electrolysers arguably extends Iberdrola’s energy value proposition to industry – a clear advantage. Additionally, working across the value chain gives better insight into the nuts and bolts of hydrogen technology along with the hurdles and opportunities – something that may prove crucial as adoption increases.

The company is also taking steps in areas that are considered longer-term opportunities for decarbonisation, such as transport. For example, Iberdrola was selected as the winner for a contract to supply Barcelona’s transport operator (Transports Metropolitans de Barcelona) with hydrogen for its fleet of renewable buses, starting this year. The project is the first of its kind in Spain, giving the company more experience in applications for sustainable transport and mobility; if successful (by way of policy support and economic viability), it has the potential to be replicated across other geographies.

Still, despite these new initiatives and potential investment the company acknowledges that hydrogen’s contribution from an earnings perspective will still be largely ‘symbolic’ and heavily dependent on government support. At this stage, by 2025 Iberdrola sees a ~€40-50mn contribution to EBITDA from hydrogen, which amounts to only 0.3% of their group wide ~€15bn target. However, while offering little in value accretion over the medium term, the opportunity set is huge and Iberdrola is again positioning itself as a leader in new technology.

Case study: gas transmission networks

For gas transmission networks in Europe, the hydrogen opportunity is immense. Gas transporters have long argued that natural gas is the transition fuel necessary to provide security of energy supply, as intermittent renewable generation is unable to adequately cover the phase out of base load coal and nuclear generation. This view has been hotly contested, with infrastructure investors largely favouring electricity networks over their gas counterparts due to increased electrification brought on by the energy transition, and potential stranded asset risk with gas. This has generally resulted in gas networks trading at notable discounts to their electricity peers in the listed markets. However, with the emergence of green hydrogen, it feels more likely that the stranded asset risk has lessened, with gas transmission networks set to play a more definitive role in the hydrogen story. This was highlighted by Europe’s gas transmission operators, who last year presented their future vision of a ~23,000km dedicated hydrogen network (or backbone) by 2040, connecting hydrogen demand and supply centres throughout the continent. The potential cost is estimated at €27-64bn, relatively low in the context of the wider energy transition as 75% of the existing network can be retrofitted.[17]

Case study – SNAM

For SNAM, owner of Europe’s largest gas transport network and one of the largest globally, this certainly seems to hold true. The company has been the most prominent advocate of green hydrogen (and other green gases such as biomethane) in Europe over the last few years, and recent developments are starting to suggest that their early support is starting to bear fruit. This is evidenced and supported by the following.

Pipelines are the cheapest way to transport gases (including hydrogen) over distances to end users

In the EU, the gas transmission grid requires limited retrofit to be hydrogen-ready, equivalent to about 10-25% of new build cost.

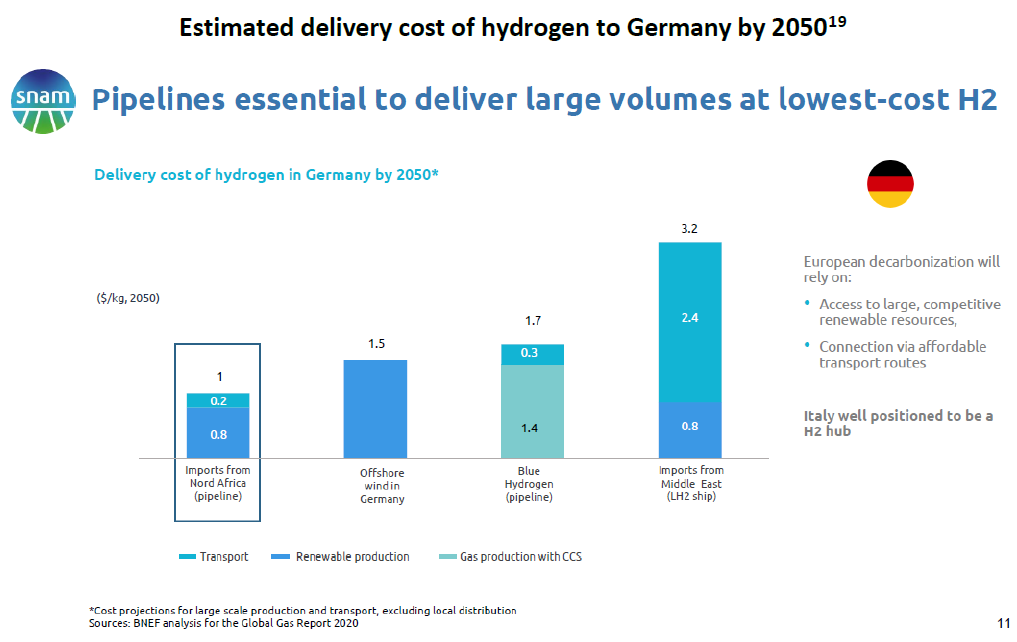

SNAM currently believes 70% of its pipeline is already hydrogen-compliant.[18] SNAM highlights that given green hydrogen’s dependency on low-cost renewable energy, it benefits from its Southern European position close to North Africa, where the region’s excellent solar resource could make it one of the most competitive green hydrogen production areas globally for European consumption. Ultimately, the (very long-term) idea is that, once hydrogen use reaches greater scale, low-cost green hydrogen can be generated in North Africa; connected into SNAM’s pipeline network; and eventually transported to those areas with highest demand, such as Germany (currently the biggest consumer in Europe).

This opportunity is highlighted by the following chart, which shows the differences in costs of delivering hydrogen from various sources to German demand centres.

Government support

With the Italian government aiming for 20% hydrogen in the energy mix by 2050, it is likely that additional investment will be required. This additional spend will be above and beyond SNAM’s regulated investment plans, which currently exclude direct hydrogen investment. Although 70% of its pipeline is hydrogen-ready and the vast majority of approved replacement capex is hydrogen-compliant, there are still parts of the network that will need to be upgraded – including things like valves and compression units – as well as potentially additional investment to overcome hurdles related to storage.

Blending

While hydrogen for downstream residential use is not one of the most efficient uses of hydrogen today, blending hydrogen in the gas grid even before consumption markets are developed can potentially help speed up adoption and further reduce carbon emissions. SNAM was the first company in Europe to test a 10% hydrogen blend in part of its hydrogen network, and has recently confirmed a 2% blend can run through its pipes. At the same time, work is underway with gas distributors and appliance makers to determine the impact of hydrogen on end users. This blending concept is further supported in the Italian government’s draft hydrogen strategy (the key components of which are shown in the following chart), as part of its aim to reach 2% hydrogen in the energy mix by 2030 and 20% by 2050.

For utilities like SNAM, cash flows in their regulated business are driven by allowed capital investment to grow their regulated asset base (RAB). While regulatory progress related to hydrogen is still in the formative stages, depending on how these investments are funded there is clearly potential for this spend to (eventually) make it into the RAB. Any additional allowed investment for hydrogen (beyond what is already approved for regular growth and maintenance in natural gas networks) is therefore likely supportive for earnings and is upside to SNAM’s steady long-term RAB growth expectation, which currently stands at 2.5% over the next 20 years.

Like Iberdrola, outside the regulated opportunity, SNAM has also created a separate hydrogen unit to capitalise on more immediate growth and, in its own words, ‘stay ahead of the curve’. It has undertaken a number of investments/projects, including the following.

Projects to convert diesel trains to hydrogen where electrification is not possible

SNAM has an agreement in place with train manufacturer Alstom and rail operator FS to provide hydrogen refuelling stations and related infrastructure, giving it a foothold in the sustainable transport sector.

Strategic investment in and a corresponding JV with ITM Power

ITM Power is currently one of the world’s largest producers of electrolysers. This not only leverages SNAM to the expected boom in electrolyser demand over the coming decade, but ITM will also be the preferred supplier to SNAM for 100MW of pilot electrolysis projects due to be used over the next five years, with the potential of further collaboration on global projects. Like Iberdrola, this makes SNAM a partner of choice for industrial clients, who may already use or could use hydrogen, with many of them already connected to SNAM’s existing natural gas grid.

Investment in De Nora

De Nora is an electrochemical and water treatment solutions company that specialises in components for electrolysers and other industrial applications. SNAM’s investment is also a seed asset for the company’s new energy transition investment fund, and is leveraged to the energy transition thematic (plus electrolyser growth) while giving SNAM a better understanding of technology within the hydrogen value chain.

Most striking is that despite hydrogen being considered a long-dated opportunity, SNAM still expects to achieve profitability within its hydrogen division by 2024 – without including any upside from expected policy support, or proceeds/loans or grants from the European and national recovery funds.

Conclusion

We believe green hydrogen will be an important component of the global decarbonisation process necessary to meet Paris climate goals and the EU’s aspiration of Net Zero emissions by 2050. It is also clear that Europe is leading the way in green hydrogen plans, and while this article has focused on the European opportunities, we expect the rest of the world is not far behind with countries globally articulating green hydrogen targets. As a global listed infrastructure investor, this is an exciting opportunity on which we will look to capitalise.

While we assess every opportunity on a case-by-case basis, at this stage we are comfortable with our portfolio companies participating in this emerging opportunity because of the:

- performance track records of their management teams in being technology leaders and in generating strong returns on invested capital, both inside and outside of their core businesses;

- fact that hydrogen-related capex is largely insignificant in the context of these infrastructure companies’ core investment plans;

- fact that, most significantly, involvement in the hydrogen evolution does not detract from the company’s core investment propositions – which for SNAM, for example, continues to be that of a gas transmission business, and for Iberdrola a renewable electricity-focused integrated utility.

Overall, it is clear these new green hydrogen opportunities within our investment universe are very exciting. However, we recognise there is still a long way to go. We see the combination of decarbonisation goals, cost efficiencies and policy support increasing the potential for long-term hydrogen adoption.

We continue to focus on high quality businesses within our universe that are leveraged to, or have optionality on, the hydrogen theme, but remain great investments independent of any hydrogen hype. Importantly, what gets us most excited is that we can still own these businesses for a lot less than what we believe they’re worth, and without compromising our valuation methodology.

Stay tuned for the next instalment on the 4D decarbonisation journey, exploring exactly how vast the renewable energy opportunity is.

[1] Iberdrola, Green Hydrogen presentation, December 2020

[2] IEA, The Future of Hydrogen, www.iea.org/reports/the-future-of-hydrogen

[3] International climate policy fundamentally changed following the 21st United Nations Climate Conference of Parties (COP) in 1995, at which the ‘Paris Agreement’ was agreed. This is an agreement within the United Nations Framework Convention on Climate Change (UNFCCC) dealing with greenhouse gas (GHG) emissions mitigation, adaptation and finance. The language was negotiated by representatives of 196 states, and adopted by consensus on 12 December 2015 and formally signed in 2016.

The Paris Agreement’s central aim is to strengthen the global response to the threat of climate change by keeping the global temperature rise this century to well below 2 degrees Celsius above pre-industrial levels; and to pursue efforts to limit the temperature increase even further to 1.5 degrees Celsius (at the time, global temperatures were estimated to have risen by 1 degree Celsius). Additionally, the agreement aims to increase the ability of countries to deal with the impacts of climate change, and to make finance flows consistent with a low GHG emissions and climate-resilient pathway.

[4] Santander Hydrogen Report, December 2020

[5] Santander Hydrogen Report, December 2020

[7] World Steel Association estimates steel accounts for 7-9% of all global emissions, Chatham House estimates cement accounts for 8% of all global emissions

[8] In July 2020, the European Council agreed to a massive recovery fund of €750 billion branded Next Generation EU (NGEU) in order to support member states hit by the COVID-19 pandemic. The NGEU fund covers the years 2021–2023 and will be tied to the 2021-27 EU budget (MFF).

[9] SNAM Capital Markets Day 2020

[10] Eurasia Group, IEA, Bloomberg - www.bloomberg.com/graphics/2020-opinion-hydrogen-green-energy-revolution-challenges-risks-advantages/policy.html

[11] International Renewable Energy Agency 2020

[12] Iberdrola

[15] Iberdrola / Energy Transition Commission

[16] 4D, Santander, Credit Suisse

[18] SNAM FY20 Strategic Plan

[19] SNAM FY20 Strategic Plan

[20] SNAM FY20 Strategic Plan

The content contained in this article represents the opinions of the authors. The authors may hold either long or short positions in securities of various companies discussed in the article. This commentary in no way constitutes a solicitation of business or investment advice. It is intended solely as an avenue for the authors to express their personal views on investing and for the entertainment of the reader.