Climate risk is real. The increasing incidence of weather events such as storms, floods, drought and wildfires have significant political, economic and social consequences.

4D Infrastructure believes the threats are real, can no longer be ignored, and should be incorporated into the assessment of the risks and opportunities offered by the infrastructure asset class.

The link between climate change and extreme weather events

Proving a link between anthropogenic (human-induced) climate change and the increased occurrence and impact of detrimental weather events has been debated for some time. The unpredictability of natural disasters has made it somewhat difficult to isolate specific drivers that can then be attributed to climate change.

A relatively new type of research called attribution analysis is helping to determine if anthropogenic global warming has increased the severity or likelihood of some extreme weather events, and by how much[1]. This is not a measure of cause, but rather of the severity/frequency.

Attribution studies run identical climate models under two following scenarios:

- Greenhouse gas (GHG) is kept at a constant level as at some historical point before humans started burning fossil fuels, and

- The world’s actual experience of GHG development over time.

By comparing the results from the two modelled scenarios, scientists can estimate the extent to which carbon emissions influenced the probability and severity of weather events.

The UK website, Carbon Brief, has at the time of writing mapped over 400 peer reviewed attribution studies of extreme weather events and analysed the trends. Overall, they conclude that extreme events have increased in the last 10 to 15 years, and has shown[2]:

- 71% of 504 extreme weather events were made more likely or more intense by anthropologic climate change

- 93% of 152 studies of extreme heat conditions found that climate change made them more likely or more severe

- 56% of 126 rainfall studies found that human activity made them more probable or intense

- 68% of 81 drought events were also exacerbated by climate change.

Source: Carbon Brief

There are limitations for attribution analysis, namely with the quality and length of climate data which feeds into the models. The World Weather Attribution (WWA) initiative, a collaboration of scientists around the world, suggests that for ideal analysis, the dataset should go back to the 1950s at least, ideally to the 19th century. However, this length of data isn’t available for all weather events across all jurisdictions.

In addition, due to natural variability, doing attribution analyses of extreme precipitation events like hurricanes is more difficult, according to climate scientist Radley Horton, of Columbia Climate School’s Lamont-Doherty Earth Observatory. “It’s not easy to do attribution on extreme rain events like this, though people do it for sure,” he said[3[.

The variability of extreme precipitation makes it difficult for models to assess patterns and correlation with climate change relative to noise of variability. There are other technical limitations based on data for storm events, but these are being overcome over time with improvements in analysis technology.

There is also growing support for scientific attribution analysis linking climate change to the frequency and ferocity of extreme weather events, being used in legal claims by individuals or groups against companies that are argued to contribute to climate change[4]. Within the infrastructure investment universe, gas and electric utilities, as well as oil/gas pipeline companies (midstream companies) could be at risk of being targeted in class action lawsuits for their alleged contribution to climate change. This area is still developing. For example, there is currently no standardised method for conducting all attribution studies which are accepted by the courts. However, there are examples of these kind of lawsuits being taken out, and it is something companies need to be aware of going forward[5].

Despite debate around the ideal inputs as well as other influencing factors, it does seem clear that these events are becoming more common and increasing in severity.

Financial risks posed by climate change

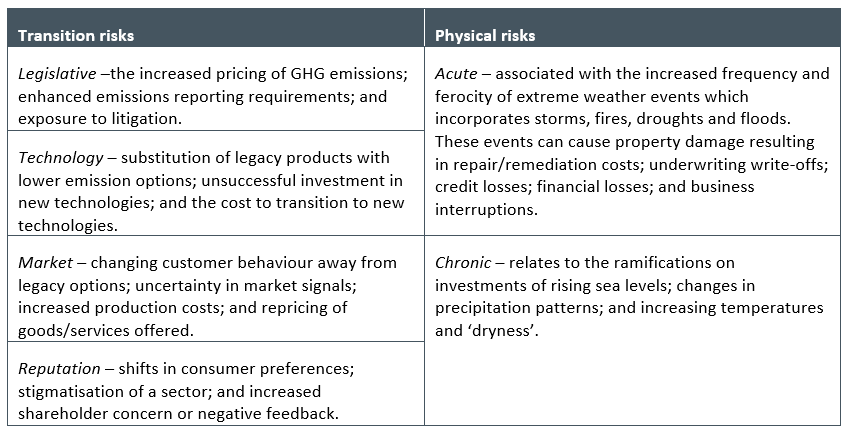

The financial risks operators face can be defined as transitory or physical.

- Transitory risks include the legislative, regulatory, technology and market changes that will occur to address the mitigation and adaptation requirements associated with the globe transitioning to cleaner, low/no fossil fuelled energy sources.

- Physical risks associated with climate change can be event driven (acute) or associated with longer term shifts in climate patterns (chronic).

Source: Taskforce Climate Related Financial Disclosures (TCFD)

To date, investors have probably been more focused on the transitory risks than the physical risks associated with climate change, as transitory risks can be measured and monitored, making them easier to incorporate into forecasts and value. With the physical risks of climate change still developing, combined with the unpredictable nature of acute physical weather events, these risks appear more difficult to assess and value – they are less certain, and the ramifications less clear. Some investors are also still sceptical on the physical risks of climate change.

Ramifications for the infrastructure sector

Extreme climate events and arguments around the cause have significant ramifications for the infrastructure sector and investors therein.

Positively, the world is working to reverse the warming, or at least halt it, providing a significant infrastructure investment opportunity. The energy transition supported by technology advancements and government policy is by far one of the biggest investment thematics of the next 30 years, and investors can capitalise on it via infrastructure companies – a theme we have written about many times before.

Concerningly, the increased number of extreme weather events are causing property damage and business interruptions with associated social and economic ramifications. While this disruption is not confined to the infrastructure sector, some infrastructure operators have also faced third party legal damages because of their involvement in triggering or exacerbating the weather event – the most common example of this is wildfire liabilities in the US impacting the electric utilities, which will be discussed further below.

As these events grow in number, the impact on the infrastructure operators, particularly those in the energy supply chain, is a concern, particularly given an uncertain yet evolving legal landscape to deal with these events.

Below we consider key climate events and how infrastructure has been impacted and responded.

Wildfire risk

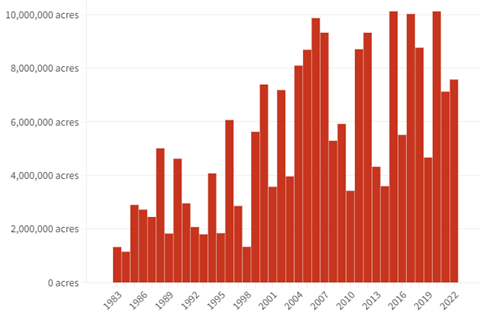

The potential for wildfires to cause damage to person and property is already a significant risk, and seemingly increasing. For example, of the 10 largest fires in the US (by acres burned) going back to 1871, five have occurred since 2013[6]. The graph below indicates the total acres burned by wildfires in the period 1983–2022. An obvious analysis of the trend over this 40-year period shows the increasing trend in damage caused by wildfires in the US.

Source: National Interagency Coordination Center

Scientific evidence suggests anthropogenic climate change is largely to blame for increasing the frequency and ferocity of wildfires.

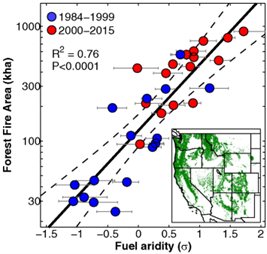

Proceedings of the National Academy of Sciences (PNAS), a peer reviewed journal in the US, have published studies that indicate the majority of the increase in atmospheric ‘dryness’ in Western US states, a key measure being vapor pressure deficit (VPD), can be attributed to anthropogenic global warming[7]. VPD results in moisture being drawn out of soils and plants, creating fuel for wildfires when ignition occurs.

The Center for Climate and Energy Solutions forecast that because of increasing VPD, an annual 1 degree C temperature increase would increase the annual median area burnt by wildfires by as much as 600% across parts of the western states of the US[8]. This risk is well illustrated in the graph below, which shows the relationship between increased frequency and ferocity of fires with increased fuel aridity driven by climate change. It plots the area burned by fires in the western continental US on an annual basis against fire aridity. A regression line is then constructed with the data.

Source: The Proceedings of the National Academy of Sciences (PNAS)

While the majority of studies to date have centred around the US, we believe this is not a US-only phenomenon. Recent fires in Australia[9] and China[10] have been found to be more severe or more likely to occur as a result of anthropogenic climate change.

Potential impact for infrastructure companies

Infrastructure companies will have insurance coverage to pay for damages to their own, and potentially third-party, property from natural disasters, up to a maximum threshold. The liability threshold of insurance policies is generally set based on historical analysis. It’s understood by companies that they will be responsible for costs in excess of these liability thresholds, but historically, this was a low risk as they weren’t expected to be breached. However, due to the increased ferocity of fires, liability thresholds are now, more often than not, being surpassed.

Insurance companies are facing an increasing number and size of claims due to the greater frequency and ferocity of fires. In response to their increased underwriting liabilities, they are increasing the cost of premiums to customers to provide coverage.

Electric utility companies are particularly exposed to third-party property claims in the scenario where their assets actually ignite a wildfire that causes significant third-party damages. There are operational considerations as to why utility assets ignite fires, but scientific evidence shows that the environmental conditions supporting wildfires has escalated. Utilities can, and are, investing to make the grid more resilient to fires, and are undertaking operational activities like vegetation management – but all this comes with increased cost.

In the US, when an electric utility wire ignites a fire, the legal liability falls on the utility company if it’s proven it was negligent in managing the network. The question of negligence is based on whether the utility acted prudently in light of heightened conditions of wildfire risk. This is a legal standard that is still being tested and established. For example, is a utility responsible if a tree branch is blown a distance onto a utility overhead wire, ignites from contact, falls to the ground, and starts a fire on contact with vegetation?

The key question moving forward is who ultimately pays for the:

- increased insurance premiums to protect against fire damage,

- third party property damage from fires ignited by utilities, and whether this should differ on questions of negligence, and

- increased investment and operational costs to mitigate fires?

Utilities appear likely to bear the direct cost. However, they generally operate under regulatory frameworks which allow for the recovery of prudently incurred investment and costs through customer bills.

This means the end consumer is paying through higher bills, which has clear social consequences. Also, should the consumer be paying if the utility has been negligent? In this case, fairness would dictate the liability should rest with the utility (this was the key reason for PG&E Corp filing for bankruptcy protection in 2019). However, this too has social consequences, as it’s clearly in the public’s interest to have financially secure utility companies to effectively provide a reliable energy service.

The answer to who pays the price is not simple. However, what is clear is that increasing wildfire risk is a major concern for utilities, their customers and governments. The mitigation of increasing wildfire risk seems to be a combination of investing in making networks more resilient, operational preparedness, and establishing a framework or understanding as to what represents prudent operation of utility assets.

To date, much of the infrastructure-linked wildfire activity has been seen in North America, namely the western states, and more recently Canada and Hawaii. However, we think this could become a more global concern, with increased fire activity in Europe this summer and expectations of another tough fire season in Australia anticipated.

Drought risk

The environmental conditions supporting wildfires are similar to those that affect droughts. The Climate Science Special Report (CSSR), which was developed by the US Global Change Research Program (USGCRP), found little evidence of a human influence on precipitation deficits (limited rainfall), but significant evidence of a human influence on surface soil moisture deficits due to increased evaporation caused by higher temperatures.

There are numerous studies in the US linking a lack of snowfall water and higher levels of evaporation to reduced surface level water flows. The CSSR also predicted, with a very high level of certainty, that under more severe global warming scenarios, and assuming no change to current water resource management, chronic, long-duration drought is increasingly possible by the end of this century[11].

Potential impact for infrastructure companies

Droughts can impact electric utility operations in areas reliant on hydrogeneration as a core source of power supply. For example, over 60% of power generation in Brazil comes from hydropower, and over the last decade it has endured the worst and longest droughts in recorded history with associated social and economic impacts. The Brazilian regulatory model was premised on levels of assured energy calculated on historical averages which aimed to ensure security of supply across the system. During the 2001 energy crisis, Brazil saw rationing and penalties for excessive consumption and, as a consequence of four very severe drought periods since, the regulatory model has under gone a number of changes, with the increased drought risk/cost shared between the operators and consumers.

Assured energy levels have been revised down more than once, and a generation scaling factor (GSF) was introduced, which limits operators’ ability to generate depending on water levels - both of these impact generator returns, and are subject to ongoing litigation/concession revisions.

In 2015, the regulatory regime introduced a tariff flag system which adjust tariffs based on different water availability, increasing the cost to end users as result of the pass on of generation costs. These flags were implemented as green (no additional charges), yellow (increased cost per KWH) and red (a further increase).

As a result of the 2021 drought, a fourth flag was introduced, ‘water scarcity flag’, which significantly increases the cost (+50% on red)

Due to the increasing threat and severity of droughts, Brazil is working hard to diversify its generation mix away from a reliance on hydropower by adding more wind and solar to the mix. As with all infrastructure investment, this is not a quick fix.

Large parts of Europe are still in drought following an exceptionally bad year in 2022. This drought exacerbated the impact from the energy crisis caused by the Russian invasion of Ukraine. The lack of rainfall meant that utilities (particularly in southern Europe) that would normally rely on large amounts of secure hydropower, struggled to procure energy. Instead, they were forced to pay sky high prices in the wholesale market to meet customer demand. This not only increased customer bills, but also resulted in significant losses in utility retail businesses, which had considerable impacts on earnings and share prices.

The lack of rain, alongside rising river temperatures has also adversely affected nuclear generation. France, which gets almost 75% of its power from nuclear energy (and is also a large exporter of energy), is most impacted, as water is used to cool nuclear reactors. French regulation sets limits on nuclear production when temperatures are too high or when river flows are impacted, as the hot water discharge can overheat rivers and threaten marine and other wildlife. EDF (operator of the French nuclear fleet) had to cut production earlier this year as temperatures soared, while during last year's heatwave they had to obtain waivers to environmental rules due to the energy crisis. According to EDF, production losses from high river temperatures and lower flows have cut on average 0.3% of production since 2000, and could potentially rise to 1.5% by 2050. This is not an incidental impact on national power supply.

Droughts also impact water utility companies. In the short term, regulated water companies’ earnings are actually supported by drought conditions, as increased customer demand for water for use in pools and on lawns actually increases volume demand and revenues. Over the longer term, many water companies affected by drought can be caught short of supply. They have a requirement under their operating licences to supply clean water on demand, so they are required to purchase water from alternate sources at an escalated price.

Similar to electric utilities, water utilities generally operate under regulatory frameworks which allow them to recover prudent costs from customer bills. The question again is then raised – who is to pay for the elevated cost of water supply in drought conditions? The question of the prudency of the elevated cost is key to determining if the water utility must bear the increased cost or it can be passed onto customers. But, if water utilities are to invest in finding alternate sources of clean water supply, this should theoretically be recovered through customer bills.

Tropical storm risk

Tropical storms cause destruction through strong winds and high surface water levels (a form of flood). Storm activity in many global locations seems to be on the rise in the past couple of decades, and could be related to climate change, albeit the length and quality of data is insufficient to determine this with a high enough degree of probability.

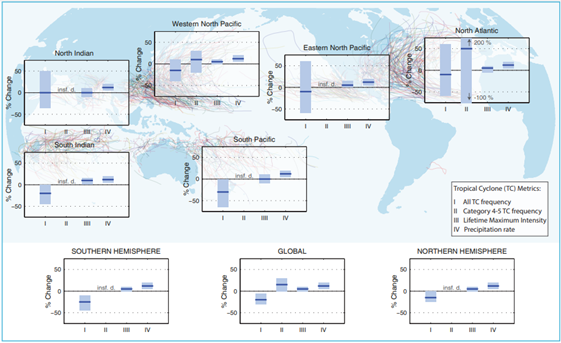

In general, both theoretical and numerical modelling simulations suggest an increase in tropical cyclone intensity in a warmer world, and the models generally show an increase in the number of very intense tropical cyclones[12]. The Fifth Assessment Report from the Intergovernmental Panel on Climate Change (IPCC AR5) provides projections for tropical storms in the late 21st century, forecasting an increase in the average intensity, precipitation rate and frequency of very intense (category 4–5) storms. It also projects a a decrease, or little change, in global storm frequency.

The graph below shows that data gathered indicates an increase in the expectation of category 4 and 5 storm frequency, and it will be much more pronounced in the northern hemisphere, particularly in the North Atlantic – a best guess estimate is a 50% increase in the frequency of these storms[13].

Source: Climate Change 2013: The Physical Science Basis

Potential impact for infrastructure companies

Obviously, strong winds can cause immediate property damage, and the associated rain may be the cause of floods. All infrastructure sectors will be exposed to property damage and/or business interruption which could run into the billions. As with other weather events, insurance policies will provide protection up to a certain threshold.

For infrastructure assets not operating under a regulatory model, losses from business interruption as a result of storm damage are clear. If insurance levels are breached, the cost is borne by the company unless the concession contract provides for ‘force majeure’ events. Even then, recovery is slow by way of concession extension, government contribution or tariff uptick. The priority of the operator is, of course, to get the asset back online as quickly as possible to minimise business interruption. In recent years, this has been an increasing concern for airport assets in particular locations.

For utilities, maintaining and restoring service to customers is a key priority during tropical storm events. Any increased costs in restoring service, such as increased working crews, maintenance costs, or temporary provisions of service, are all borne by the company. The cost to replace or repair damaged property requires immediate cashflow. The utility will usually attempt to recover these prudently incurred costs through the regulatory mechanisms available, but it can take time for recovery. This has caused uncertainty in recovery, and therefore elevates liquidity and credit risks.

In some countries, such as Italy, utilities receive incentive returns if they meet reliability targets. This increasing occurrence of storms has made it difficult to achieve incentives, so the companies are motivated to invest in strengthening their networks to withstand the strong winds driven by storm conditions. The need to invest to maintain, let alone improve, reliability performance is making achieving increasing regulatory reliability targets more difficult and more costly over time.

The increasing occurrence of storms from climate change intensifies any credit risk for utilities, and also raises affordability concerns for customers as costs of the utility are recovered through bills. The recovery of increased storm-related costs is an ongoing focus for credit rating agencies who perceive the increasing frequency and ferocity of storms as a credit risk for utility companies.

4D’s approach to managing climate risks

4D considers both the physical and transition risks/opportunities posed by climate change as being central portfolio concerns. We undertake environmental assessments as part of our overall ESG due diligence at all stages of our investment process, including in screening our universe, at a country level, at the individual stock level, and in developing and assessing the portfolio as a whole.

The risks posed by natural disasters, and the ramifications they can have on infrastructure companies, is continually developing. We monitor the situation in all the global markets we invest in, including due consideration to legal frameworks, and political environmental goals and directives. At the individual company level, the environmental risk assessment involves understanding the environmental risks that the company is exposed to, and the efforts that are being taken to mitigate these risks. This includes consideration of jurisdiction, contract/regulatory structures, as well as management quality and execution. We rate the company on a qualitative basis based on this exposure and mitigation efforts, as well as incorporate sensitivity/scenario analysis into our valuation assessments.

Conclusion

The increasing frequency and ferocity of acute physical weather events associated with climate change are causing increasing headaches for infrastructure investors. Storms, wildfires, droughts and floods have caused varying operational and financial difficulties for infrastructure companies, often having significant impacts on share prices and investor returns. This raises the question, have we now reached a new norm where the acute physical risks from climate change are not considered rare or ‘one-off’, and need to be recognised as key risks by infrastructure investors?

[1] Attribution Science: Linking Climate Change to Extreme Weather; Renee Cho; October 4 2021

[2] Mapped: How climate change affects extreme weather around the world; https://www.carbonbrief.org/mapped-how-climate-change-affects-extreme-weather-around-the-world/

[3] Attribution Science: Linking Climate Change to Extreme Weather; Renee Cho; 4 October 2021

[4] Scientific American: Scientists Can Now Blame Individual Natural Disasters on Climate Change; Chelsea Harvey; 2 January 2018

[5] In September 2023 the state of California sued multiple large oil companies including Exxon Mobil Corp, Shell Plc, and Chevron Corp, accusing them of knowingly downplaying the risks associated with fossil fuels, and alleges that the companies caused tens of billions of dollars in damages and accused them of deceiving the public.

[6] 10 Largest Wildfires in U.S. History; Western Fire Chiefs Association; 13 December 2022

[7] Impact of anthropogenic climate change on wildfire across western US forests; John T. Abatzoglou & A. Park Williams; October 10, 2016

[8] Center for Climate and Energy Solutions: Wildfires and Climate Change; https://www.c2es.org/content/wildfires-and-climate-change

[9] Attribution of the Australian bushfire risk to anthropogenic climate change; Geert Jan van Oldenborgh, Folmer Krikken, Sophie Lewis, Nicholas J. Leach, Flavio Lehner, Kate R. Saunders, Michiel van Weele, Karsten Haustein, Sihan Li, David Wallom, Sarah Sparrow, Julie Arrighi, Roop K. Singh, Maarten K. van Aalst, Sjoukje Y. Philip, Robert Vautard, and Friederike E. L. Otto;

[10] Attribution of the Extreme Drought-Related Risk of Wildfires in Spring 2019 over Southwest China; Jizeng Du, Kaicun Wang, Baoshan Cui

[11] Fourth National Climate Assessment (NCA4), Volume I; The Climate Science Special Report (CSSR): Chapter 8 - Droughts, Floods, and Wildfire

[12] Fourth National Climate Assessment (NCA4), Volume I; The Climate Science Special Report (CSSR): Chapter 9 - Extreme Storms

[13] Climate Change 2013: The Physical Science Basis; Chapter 14: Climate Phenomena and their Relevance for Future Regional Climate Change; https://www.climatechange2013.org/images/report/WG1AR5_Chapter14_FINAL.pdf

The content contained in this article represents the opinions of the authors. The authors may hold either long or short positions in securities of various companies discussed in the article. This commentary in no way constitutes a solicitation of business or investment advice. It is intended solely as an avenue for the authors to express their personal views on investing and for the entertainment of the reader.