Company management meetings and site visits are integral to our investment process, and after 2 years attending online it was fantastic to be back in Cancun at Santander’s flagship Latin American conference. Over the week, Sarah visited with management teams from regulated utilities, renewables, and transport players across the region. She also experienced firsthand the passenger recovery at the Mexican airports and growth in the region. In the second leg of the trip, North America was the focus, with Sarah exploring divergent views on where we are in the economic cycle and what the outlook is for 2023.

In this piece, we highlight some interesting themes and observations from the trip. We also reiterate our overweight call to the LatAm region into 2023.

Politics

Mexico

Mexico is back in fashion, with many market participants increasingly comfortable in understanding the core government policies and, importantly, largely supporting them. These include:

- Fiscal discipline and austerity

- Central Bank monetary policy independence

- Internationalisation

- Government control of the energy sector (note – we disagree with this policy)

- Pro women and labour policies

One commentator pointed out that it looked very similar to Mexico in the 1950/60s – a stabilising economic plan that saw a 15-year economic boom with an average growth of 6.8% pa, industrial production up 8%, and inflation staying at just 2.5% – the ‘Mexican Miracle’[1]. Considering Mexico is facing presidential elections in 2024, 4D is not yet confident of a continuation of current policy post the election, although many investors Sarah spoke to expect some continuity in any new administration. From our viewpoint we hope this is the case as the policy framework, should it survive, is certainly one that we could largely get behind.

In terms of the election, front running as successor to Andres Manuel Lopez Obrador (AMLO) is Claudia Sheinbaum, the head of Mexico City who enjoys the support of key members of the governing MORENA party. As always, we expect some volatility in Mexico in the lead-up to the election. Ahead of the trip we saw increased political and social tension around drug cartels and expect this will remain a key election policy which could cause some unrest.

Brazil

Arguably returning President Luiz Inacio Lula da Silva (Lula) did not start well, with a lot of rhetoric concerning the market on a fiscal level. However, we note that Lula is not new to the role and, despite significant concerns and a lot of noise when he started in 2003, he proved to be quite fiscally responsible while also supporting significant social reform.

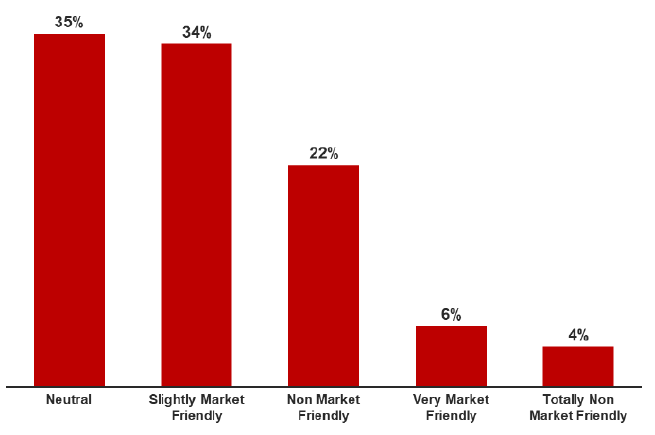

The consensus view at the conference was that Brazil is in no way as bad as the locals believe, with nearly 70% of those polled expecting Lula to be neutral at worst.

Question: What do you expect for the new Brazilian government in 2023 in terms of impact on equities?

Source: Santander Investor Poll – 162 responses

Many participants were also increasing their overweights to the country. Despite the noise:

- Talk of a 1% deficit this year is in no way a disaster – the market was expecting 0.5-1%

- While Lula is more left, he historically has not, and is not expected to, cross fiscal boundaries

- Interest rates are likely to come down in Brazil this year – a significant catalyst for growth and equity re-rating, and

- Some solid policy objectives are on the agenda – the proposed tax simplification agenda, which would consolidate 5 taxes to a single VAT (24%), would be a great step forward in productivity (tax regime complexity leads to very low Brazilian productivity).

At the same time, current equity market valuations are pricing in a worst-case scenario, to the point that the market is trading at a discount to the disastrous Dilma era of 2011-16 when Brazil experienced the most severe financial crisis in history. While Lula’s policy may be uncertain at the moment, this is more than priced in and his track record is quite rational. One commentator actually stated that Brazilian equities were the cheapest in the world and offered significant opportunity at these levels.

Sarah had some concerns that if Lula was only looking at a single term in office (he may be seen as too old for re-election), he may be more aggressive in this term in an effort to realise his social ideals and leave a legacy at the expense of economics or sensible policies. However, having canvassed a number of players (domestically and internationally), the largely unanimous view is that even if Lula does not seek re-election himself, he will want his party to remain in power and this will curtail any radical action – the legacy he wants to leave is one of party popularity as well as his own. This gives us increased confidence that his policy choice will be restrained, and he will seek to manage social, fiscal and economic goals.

Argentina

2023 is an election year for Argentina, with it increasingly likely that we will see a move centre right in the August polls, which would be a strong positive for the country. However, a positive outlook is already reflected in equity prices with the market up 80% since their World Cup win. While we see significant longer-term opportunity in Argentina under a new regime, it is going to take time to realise and we need to see important green shoots before Argentina could become investible – the path to recovery is long and winding.

Andean

It’s hard to get excited about the Andean region as yet, with a number of political overhangs and economic headwinds.

Economics

Mexico

The Finance Minister, Mr Ramirez de la O, delivered quite a positive message for the domestic outlook for 2023/24 – he is not forecasting a recession, while budget planning remained unchanged with a base case GDP growth of 2.5-3% in 2023.

The Minister believed ‘crowd’ sentiment was ignoring two key drivers of economic activity, namely:

- Service sector/tourism is still in post COVID recovery mode: it has lagged some other sectors and is now expected to be well above trend for 2023, supporting overall growth targets, and

- Domestic level debt is very low: with all the social programs implemented in 2020, household incomes improved significantly, and this is driving additional consumption. This is further supported by recent substantial increases in the minimum wage.

As such, Mr Ramirez expects Mexican domestic demand to decouple from US trends for at least the next couple of years. We are starting to see this through increases in Mexican GDP growth targets for this year and next.

On the flip side, he believed inflation had started to turn, with expectations it will start to normalise in 2023. He cited the cap on gasoline prices having helped curb inflation while supporting consumption-led growth, with the government confirming the extension of this cap through to the end of 2023.

Interestingly, however, since the conference Banxico surprised the market in raising the policy rate by 50 bps to 11.0% (est 25 bps) as the Labor Ministry reported that private wages negotiated in January of this year increased by an average of 11.2%. This, combined with the increase in the minimum wage by 20% this year, could destabilise the inflation goals. This metric, as with elsewhere in the world, warrants ongoing monitoring. We will continue to position to capture the inflation.

Mexico, and importantly the infrastructure sector, should also benefit from a couple of longer-term growth thematics, namely:

- Onshoring or nearshoring: the practice of transferring a business operation that previously moved overseas back to the country in which it was originally relocated, and

- Energy investment: in line with virtually every nation in the world, Mexico is working to ensure security of supply and a smooth transition to a greener environment.

These thematics not only support growth, but importantly jobs and the continued emergence of the middle class in Mexico, with the infrastructure sector both a key driver and long-term beneficiary of this trend (discussed further below).

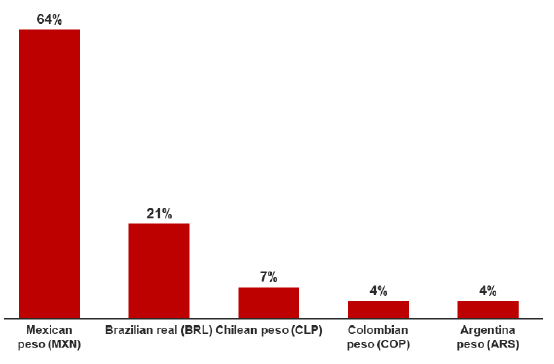

One of the main concerns for Mexico was a possible hard landing recession in the US, which could have a negative impact on Mexican exports and discretionary sectors with a general flow on to the broader economy. Regardless, investors had a strong belief that Mexican equities and the currency would be top performers within the region this year.

Best performing LatAm currency in 2023?

Source: Santander Investor Poll – 191 and 184 responses respectively. Qualification: 54% of survey respondents were Mexico based.

Brazil

Domestically the economic environment is improving, with inflation now tracking below the US and a strong expectation that interest rates will come down this year – a significant positive catalyst for Brazilian equities, and in particular infrastructure names. As interest rates turn, the relative attractiveness of equities to the Selic swings for domestic investors and we should see a significant flow of funds into the domestic equity market. We expect investors to start looking 6 months out for this dynamic, so we could see some re-rating sooner rather than later.

The external environment also remains relevant for Brazil, with a couple of key positive catalysts in 2023:

- China re-opening is positive – a commodity exporter both soft and hard

- Fed tightening – a halt in tightening supports capital flows and improved balance of payments.

Chile

Within the region, Chile was expected to be the first to cut interest rates post a brief recession and politically could see some upside. It’s not without positive news, but we believe it is largely priced in.

Argentina

A challenge awaits the new administration, with 40-50% of the population currently dependent on subsidies. The economic outlook requires significant improvement before we could consider upgrading it from a Red (uninvestible) country grading.

USA

Throughout the trip Sarah spoke with a number of US economists on the outlook for domestic growth, inflation and interest rates in 2023. Her key takeaway was that it is anyone’s guess – certain charts tell one story while others another, and we are not sure we can rely on historical trends. Just three examples of divergent views:

- Inflation has already turned a corner, growth is slowing and not only will the Fed halt rate hikes this year, they will begin to ease policy – Professor Siegel of Wharton School of Finance

- Jobs, economy remain stronger, inflation remains elevated. The growth outlook is solid, savings rates high and interest rates end higher than the market expects – 2023 OK but watch out for 2024 when rates really start to bite – Stephen Stanley, US Chief Economist Santander

- Growth to fall off a cliff and hard landing inevitable as the Fed rate ends higher than anticipated and earnings revisions are extreme – France Trahan, Trahan Macro

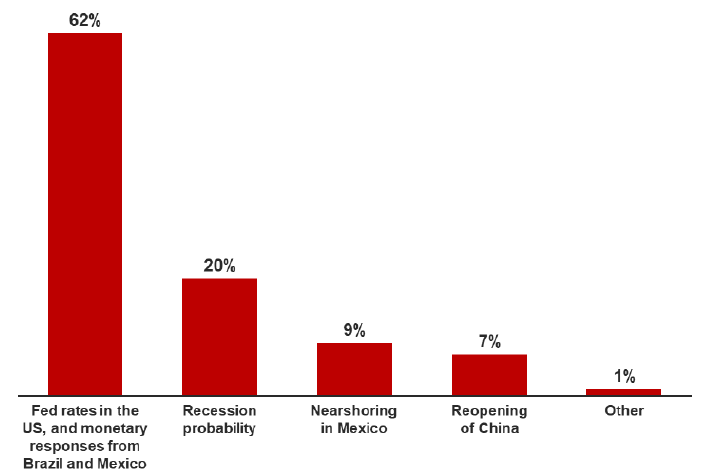

We certainly don’t have a crystal ball, but at this stage we remain positioned for inflation and interest rate rises, which means an overweight to names that are positioned to better capture these dynamics.

It is also clear that Fed activity is the key concern for investors across the Americas into 2023, so we will be monitoring it closely.

Source: Santander Investor Poll – 201 responses

Infrastructure

While much is happening across the economic and political landscape, what was clear from this trip was that infrastructure investment is needed to support key political and economic goals, including:

- Onshoring: a talking point at this year’s conference and seems to be a real opportunity for the region, particularly Mexico, as long as it is supported by much needed infrastructure development

- Emergence of the middle class: EM governments have recognised the direct link between infrastructure and economic advancement. They need private sector capital to meet their infrastructure investment needs so economies can continue to evolve, seeing increased privatisation of assets and support for investment pipelines

- Tourism: the pent-up demand is real and not yet abating – a positive for airports

- Utilities: Security of supply and a move to a greener energy mix is not just a developed market phenomenon. Arguably it is even more important in the emerging world and the globe will not reach Net Zero without this commitment.

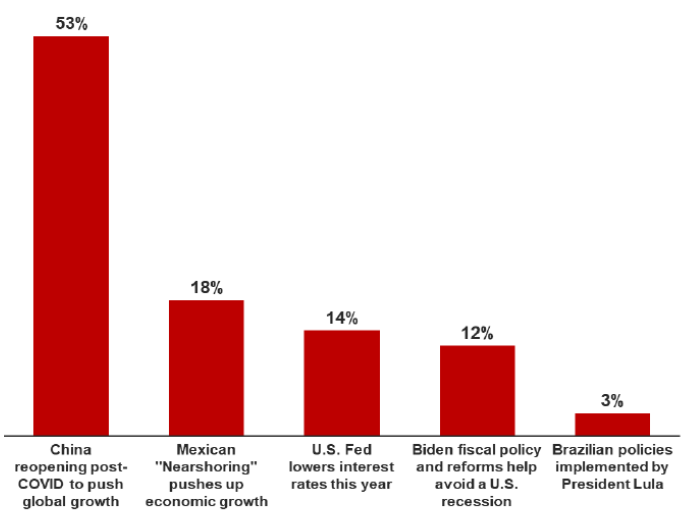

One of our key cyclical investment drivers for 2023 (see Global Matters: 2023 outlook and News & Views: China reopening post COVID) was also well supported by LatAM investors.

Question: What positive event do you expect in 2023?

Source: Santander Investor Poll – 206 responses

As we discuss key sector dynamics below, we touch on each of these issues.

Onshoring/nearshoring

Onshoring was a key talking point at this year’s conference, with the expectation that the return of manufacturing to domestic shores will drive activity and growth across the region, particularly in Mexico. This is receiving significant government support as they look to reduce exposure to China.

Interestingly, the average monthly manufacturing wage in China is currently ~US$840 while in Mexico it is just $480[2], so onshoring is viewed as a huge opportunity. The biggest hurdle to the return of commercial / industrial / manufacturing hubs is security of energy supply. Importantly, the government has recognised this and is working to reinforce energy positions and storage to support onshoring efforts. In our view, the biggest constraint to this is the domestic government’s ongoing commitment to control the energy space – we cannot see much-needed investment happening while this remains in play (see below).

As infrastructure investors we can capitalise on this thematic by way of general economic upside, but also through direct exposure to infrastructure operators well-positioned to capitalise on it, such as OMA Airport and KSU rail network (under offer from Canadian Pacific).

Mexican energy investment

The government remains focused on significant investment in renewables, supported by both domestic and foreign money. This investment supports growth, energy transition, security of supply, onshoring targets and the emergence of the middle class. However, this is a theme we are less inclined to buy into at this point considering the ongoing political intervention in the energy sector and the requirement for domestic government control of energy assets as a key policy.

The current government would like to see the foreign investment dollar as an equity/financial partner, not a controller. However, foreign industrial operators with the skillset to facilitate the investment are looking for control. The recent treatment of existing foreign operators has seen them halt investment in the space (e.g. Iberdrola is not allocating additional capital to the country at this stage, despite a strong commitment historically).

Until the framework is supportive of the investment dollar, we don’t see this changing significantly and so are less inclined to support this growth driver. We don’t believe the Mexican government and domestic operators (even with financial partners) can fully facilitate the investment, and unfortunately could see it hinder Mexico’s development.

Brazilian utilities

Utility conversations were somewhat fragmented, given the differing strategic priorities of individual players (e.g. CEMIG is focused on potential government sell down). However, a few common themes came through in meetings.

New Energy Minister

There is some sector uncertainty as Brazil has a new energy minister under the Lula government and, as he comes from a different sector, a learning curb is expected. However, ANEEL (the regulator) remains strong, independent and technical, so we are hoping for minimal sector disruption.

Concession renewals within the distribution sector were a priority, with the impacted operators not anticipating any issues as renewal is facilitated in the contract, there is precedent and the regulatory model ensures a regular recalibration of returns. However, until the renewal is resolved this remains a distribution overhang.

Inflation

We remain constructive on the Brazilian utilities in the current economic environment, with the names we spoke to net winners from inflation through tariffs. While delinquencies and losses have ticked up slightly due to affordability, the uptick is marginal while the inflation hedge on tariffs is across the regulatory base and compounded. Capex inflation has also largely been factored into budgets and is more than compensated by the regulatory construct.

Generation mix

Hydrology is finally looking good in Brazil after years of drought, and this is driving down power prices which is discouraging some from increased investment in the generation sector – over the next few years supply could outpace demand.

Security of supply in the longer term remains an issue though, and sector investment dollars are going into transmission, piloting green hydrogen and further diversification of generation mix (under contract).

Transmission

This is a significant opportunity for many years to come – there is a need to connect a huge amount of new generation to the grid while managing hydrology risk and other intermittent technologies.

Further auctions of new lines are coming this year and operators are expecting it to be competitive considering how attractive the sector outlook is. CPFL also highlighted significant brownfield transmission line opportunities from more than one seller, which could be more attractive in the current market than the new auctions.

Capital allocation

As a sector, the core operators have strong balance sheets supporting not only their growing investment budgets but solid dividend policies. As interest rates in Brazil turn, these yields will look increasingly attractive offering another level of support for well-managed players (e.g. CEMIG has a 9% dividend yield on a 50% payout ratio).

Mexican airports

The Mexican airport group, in our view, offers the gold standard in airport operations, capitalising on strong regulation and long-term thematics. Not only have we seen passenger recovery beyond 2019 levels with little signs of momentum slowing, but margins have expanded and, with under-leveraged balance sheets, the bottom-line growth has been extraordinary.

The 3 Mexican airport names offer different catalysts moving forward and we remain overweight.

- ASUR: Significant play on international tourism complemented by attractive international exposure to Puerto Rico and Colombia, and a net cash position supporting ongoing expansion, capital allocation and M&A

- GAP: The most balanced mix of tourism, international and domestic traffic with the Tijuana cross-border model – unique and unable be replicated. Also offering significant expansion potential and attractive international exposure in Jamaica

- OMA: Slowest to recover post COVID given significant exposure to domestic business travel, but now the largest beneficiary of the onshoring thematic. Recent change in strategic ownership a positive with Vinci entering with a controlling block.

Despite being sector outperformers in 2022, we remain buyers of the 3 names for the following reasons:

- Strong, robust and tested dual till regulation: 5-year forward looking resets that support investment and allow for re-calibration in COVID-like events

- Good traffic mix of domestic, VFR (visiting friends & relatives), tourism and business pax across the group

- Traffic has already rebounded well above pre-COVID levels and momentum remains strong

- Inflation hedged tariffs and a natural USD hedge in regulation as well

- Big beneficiary of the emergence of the middle class both in terms of passengers and non-regulated spend

- Capacity to expand airports to accommodate ongoing passenger growth

- Beneficiary of onshoring particularly OMA

- Beneficiary of China’s reopening

- Very strong balance sheets supporting growth and capital allocation

Having met with the airport operators, nothing has derailed this fundamental viewpoint and, in fact, we see upside to our forecasts with:

- GAP guiding to a further 6-8% passenger growth this year, despite already being back at pre-COVID passenger levels. This is driven by seat availability and trends being observed, business travel starting to ramp up and launch of new airlines and routes.

- ASUR was also very positive on the outlook, with traffic resilience to any economic slowdown and new markets keeping momentum strong.

We are also seeing further commercial upside in parking, retail and food & beverage with operators adapting to the changing demand.

Brazilian concessions

The focus within the transportation space was growth, with an underlying hope that the market would recognise the fundamental upside being realised.

Concession pipeline

While it is widely believed that the new project pipeline is intact, a new government could see some delays in the process. There has been some suggestion that the model will be restructured to remove the concession fee while lowering tariffs, which would not only benefit users but hopefully attract competition for the assets. Also, in an effort to improve the competitive dynamics, large concessions (capex requirements of ~R$8-10bn) could be split into smaller concessions that are less complex.

Any delay could actually prove to be a positive for the incumbent operators (CCR and Ecorodovias), who have both won significant projects over the last few years and could do with some time to focus on delivery, execute on planned capex and move recent wins to profitability. This would then rebuild their investment capacity ahead of the next wave.

The operators don’t anticipate the competitive environment to ramp up significantly as, unlike historically, there are still more opportunities than players (even with new entrants like Vinci) so they are expecting 3-4 bidders for each project. This will also allow the operators to be more selective in their targets.

Capex profile

2023 will be a significant year of investment for all the Brazilian concession operators as they execute on committed capex for recent wins (eg. CCR and Ecorodovias) or approved expansions (Rumo and Santos Brasil). While some delays are expected as a result of the approval process, every concessionaire will be working hard to execute with associated earnings growth in years ahead.

Good news not priced in

There is some frustration from operators that a number of positive wins in 2022 have not yet been reflected in their share price. The fundamental catalysts are in play, but belief is that the economics (interest rates) need to turn before investors look to equity markets again. When they do, though, the re-rating will be fast.

For example, in 2022, CCR saw:

- Toll road traffic above 2019 levels

- Rebalancing approved

- Barcas concession resolution with compensation agreed

- New concession wins in road (RioSP), metro (Lines 8&9) and airport space (South Block, Ventral Bock and Pampulha), and

- Sale of TAS.

However, the stock was down 7% in 2022 with the justified upside discounted on near-term interest rate sensitivity.

Capital allocation

The priority is to execute on significant capex programs while managing leverage levels within target ranges. Dividends are in play, but taking a back seat to growth at this stage. Considering the quantum of opportunity available at the moment, we are supportive of this strategy.

Conclusion

Despite a difficult global macro backdrop and even with some potential domestic political headwinds, the trip reinforced our overweight position to the region. We have factored in all potential risks and believe the value proposition of the quality infrastructure names is too great to ignore. Further, some of our key investment themes for 2023, both cyclical and thematic, are supported by the regional operators.

Cyclical

- Re-opening trade: 2023 is China’s year and Brazil and Mexico will benefit.

- Macro evolution and positioning: buoyant Mexican outlook and Brazil turning a corner which is a catalyst in itself.

Core long-term thematics

- Emerging markets: population growth and an emerging middle class.

- Energy transition: a global phenomenon with Net Zero requiring emerging market buy-in. Importantly, it is nice to see we are not alone in our thinking.

Importantly, it is nice to see we are not alone in our thinking.

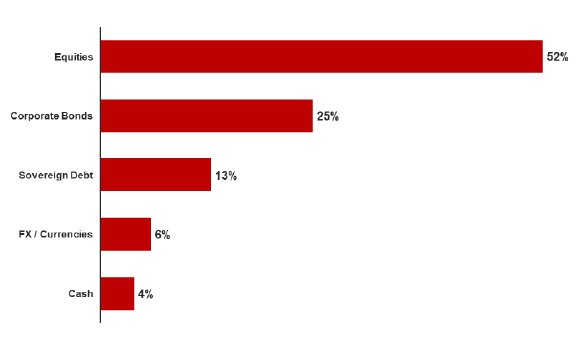

Which LatAm asset class will provide best return in 2023?

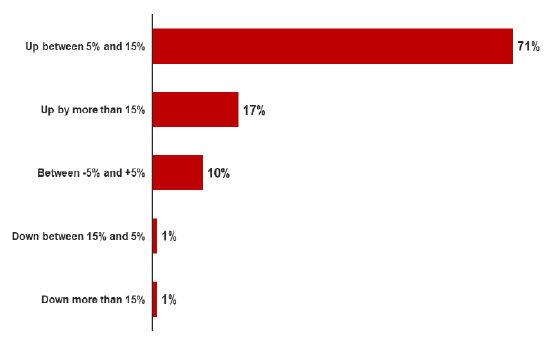

MSCI LatAm upside (US$) for y/end 2023?

Source: Santander Investor Poll – 204 & 182 responses respectively

At a sector level, in summary:

- Brazilian infrastructure: equity markets discounting a worst-case scenario and infrastructure names are not reflecting fundamentals in their share prices. We expect some positive catalysts this year in terms of macro news which should support a re-rating in high quality, well-managed, attractively-valued names.

- Brazilian utilities: improved generation conditions see a sector focus on distribution and transmission to support the ongoing build out of a diversified generation mix and ensure security of supply. The operators are largely insulated from the current macro environment and despite significant capex opportunity are offering attractive dividend yields, supporting share prices.

- Mexican airports: well insulated from the current macro environment and offering attractive value on a strong outlook.

- Mexican energy space: the one sub-sector still on watch for us, despite commitment from the government to build out. We are not yet comfortable with the government ownership/control stance.

- Other: the US economic outlook is anyone’s guess, but we are not currently in the camp of a hard landing. We are positioned in stocks exposed to inflation such as electricity and gas, pipelines and communications.

As always, at 4D we maintain a diversified portfolio of high quality infrastructure names globally. At the moment, we believe LatAm is offering a great mix of quality and value despite near-term headwinds.

[1] A term used to refer to the country's inward-looking development strategy that produced sustained economic growth in the 1960s. It is considered to be a golden age.

[2] China National Bureau of Statistics, China Ministry of Commerce, INEGI, Trading Economics. All data is for 2021.

The content contained in this article represents the opinions of the authors. The authors may hold either long or short positions in securities of various companies discussed in the article. This commentary in no way constitutes a solicitation of business or investment advice. It is intended solely as an avenue for the authors to express their personal views on investing and for the entertainment of the reader.