The EU and the eurozone: its origins, limitations and frustrations

The EU is an economic/political union which traces its origins back to the 1950s. It comprises 28 member states operating as a single market, with a broadly standardised system of laws. As a consequence, passport controls have been abolished in some countries (the Schengen area).

The monetary union (the ‘eurozone’ or ‘euro area’) was established in 1999 and came into full force in 2002. It comprises 19 (of the 28) member states that use the euro as their legal tender and have the European Central Bank (ECB) as their central bank. Therein lays a key structural flaw of the eurozone: it is a monetary union only. Member states retain fiscal powers although Brussels (EU’s HQ) looks to impose, with some success, fiscal discipline across all states.

There has been a huge amount of material written on Brexit, most of which focusses on the future pros and cons of remaining in the EU. However, as the EU has now been in operation for some time, we believe voters will be more inclined to look in the mirror before they pick-up a telescope. That is to say, they will first ask what has the EU delivered for their country, and for them as individuals before they look ahead towards potential future rewards. While Britain ponders an answer, we examine this question for two of the three biggest eurozone members – Germany and Italy - to identify who else may re-think their EU membership.

Germany v Italy and eurozone economics: the good, the bad and the ugly

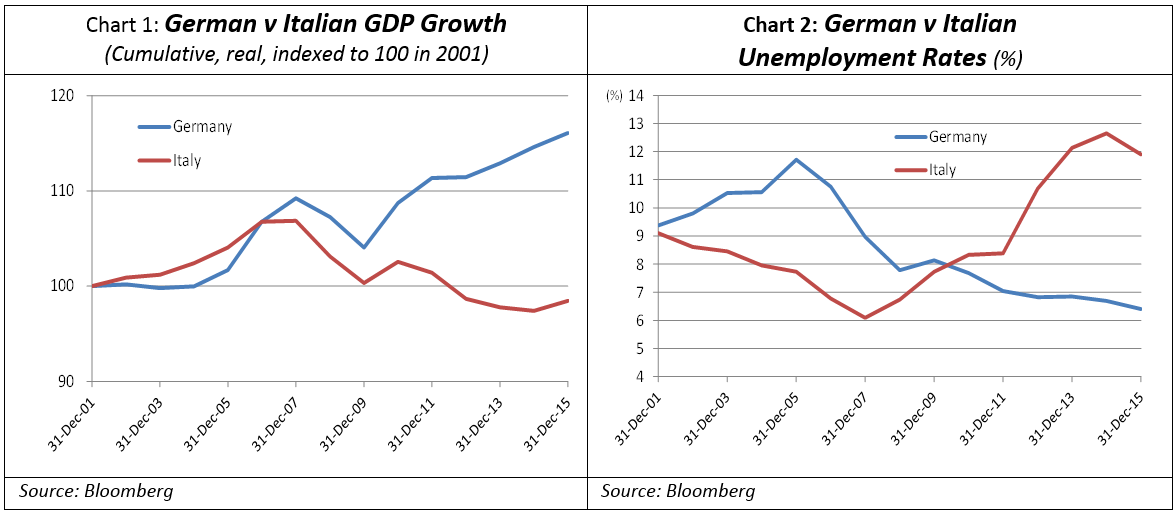

From an economic growth and employment perspective, EU membership for Italy has been very underwhelming relative to Germany. As is shown in Charts 1 and 2 below, GDP growth in Germany has far outstripped Italy since 2002 (the start of the eurozone). Italy has been in recession for five of the past eight years, while unemployment is currently nearly twice what it is in Germany.

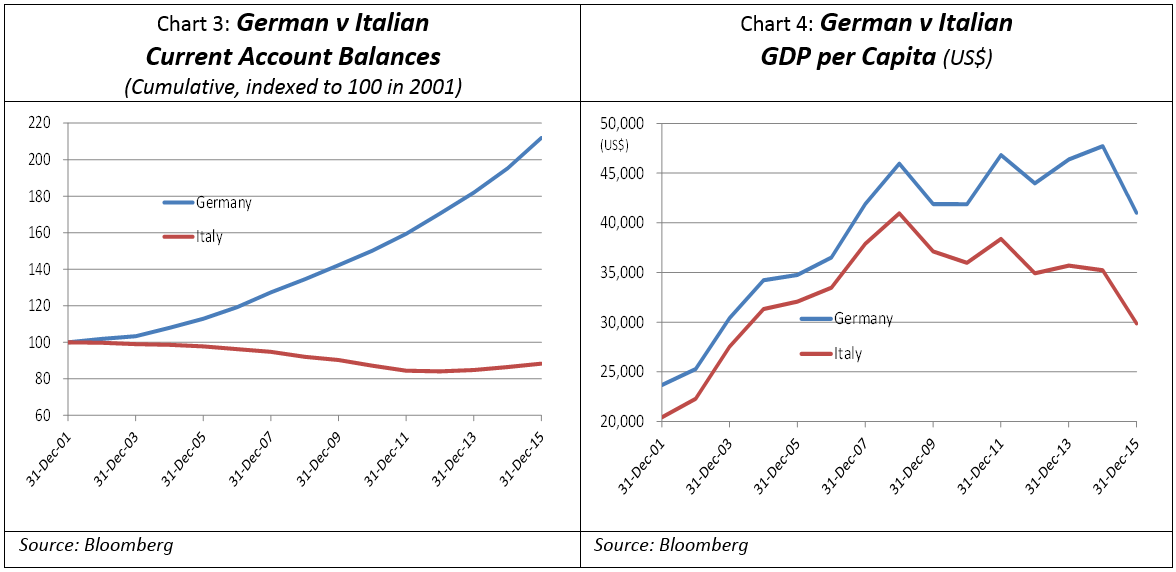

Looking further into the comparatives, the divergence in economic fortunes becomes even starker. Germany’s relative economic strength has allowed it to consistently run current account surpluses (Chart 3) relative to Italy’s decade of deficit, while GDP per capita, a broad measure of individual wealth, has also diverged sharply between the two countries (Chart 4).

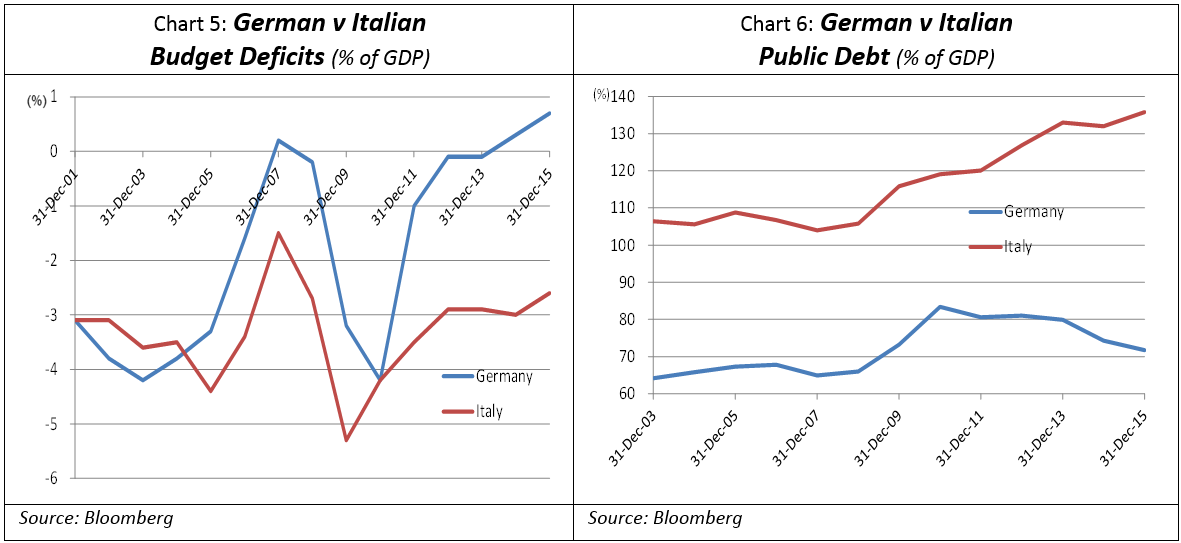

The public accounts of each nation tell a similar story. Whereas Germany has moved to a budget surplus (Chart 5) and has a stable, manageable public debt load, Italy remains mired in budget deficits with public debt at 130%+ of GDP and climbing (Chart 6). Are we starting to sense some unhappy EU punters in Italy?

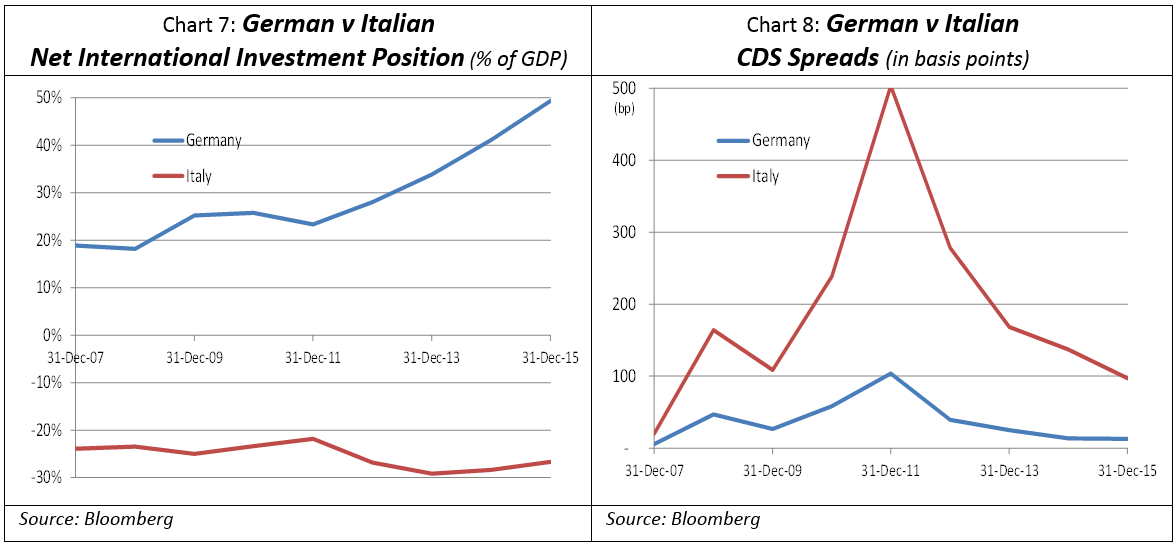

For our final point of comparison, we turn to financial markets. As shown in Chart 7, the difference in the two countries’ Net International Investment Positions [1] (NIIP) could not be more dramatic. Germany has a NIIP of +50% of GDP and growing, which means it is a substantial net creditor (lender) to the world. Conversely Italy’s NIIP is ~-25% of GDP, which means it is a significant net global borrower.

All of the metrics above are reflected in each country’s Credit Default Swap [2] (CDS) spread shown in Chart 8. Italy’s have been very wide (500bp in December 2011) and currently reside at ~120bp, or almost seven times those of Germany. Similar to a credit rating, these spreads reflect the relative credit standing and borrowing costs of each nation.

Has the EU really been that bad for Italy…and what was that structural flaw mentioned earlier?

Of course it is far too simplistic to attribute the differing economic fortunes of Italy and Germany to EU membership alone. Many of Italy’s issues predate the eurozone while other contributors to that divergence are the differing history and culture of each nation.

However, a number of important observations can be made from our analysis:

- The Italy/Germany economic disparity can’t be ignored: Given the EU and eurozone has been in place for well over a decade, it would be easy for an Italian voter to associate their country’s economic malaise with EU membership. As they glance north across the Alps at their far more prosperous, contented neighbours in Germany, the simple answer for an Italian voter asked whether EU membership has been worthwhile could be ‘No’.

- The eurozone’s structural flaw – monetary not fiscal union: There is a structural flaw in the eurozone which helps propagate the unequal economic outcomes described above. That weakness is that, unlike say the United States, the UK or the Commonwealth of Australia, the eurozone is only a monetary and not a fiscal union. This means that, while individual members control their own spending and taxation policies (with oversight from Brussels), they remain inextricably linked via a single currency – the euro. As a result, individual nations do not have the benefit of independent monetary policy or a free floating national currency which can act as an economic ‘shock absorber’ in times of economic difficulty, helping countries to adjust and retain international competitiveness, and a ‘brake’ in times of prosperity.

A recent example of this is how the A$ has depreciated from +$1 to ~73c against the US$ as the mining boom receded. This has helped reinstate the export competiveness of the Australian manufacturing and service sectors. However, the single currency eurozone does not facilitate this. If a country is relatively uncompetitive against its eurozone peers, its main option is to try and improve productivity, primarily via labour market reform. As we are witnessing with the national strikes currently sweeping France, protesting against exactly these types of labour market reforms, such changes are politically very difficult to achieve.

- Winners are grinners: Then of course there are the economically stronger countries such as Germany, who made many of the tough structural changes to their economy early on. The composite euro currency is clearly to their benefit as their superior economic performance is not rewarded by as significant a currency appreciation as might have been the case had a single currency deutschemark still been in circulation. The weaker euro means Germany has continued to benefit from very strong export dynamics (hence the substantial current account surpluses noted above) and is a very significant beneficiary from EU membership. This is a key reason why Germany works so hard to maintain the union - as evidenced by its efforts to keep Greece afloat and inside the tent.

- National security is not the issue: Finally, a growing issue in the Brexit vote, and any subsequent referendum, is border security and sovereignty. This matter is outside the scope of this paper but one observation is worthwhile. The issue in-play in Brexit largely revolves around the European refugee crisis. It does not relate to national security which in Europe remains within the ambit of the North Atlantic Treaty Organisation (NATO), which is a good thing given an increasingly restless Russia.

Conclusion

To Brexit or not to Brexit is the question facing UK voters on June 23. It will be a defining moment for Britain and the European Union, potentially a major macro event and have significant longer-term ramifications for global equities.

Looking to who may be next, based on their relative EU experiences Italy has clearly been a poor cousin relative to Germany. While this divergence in fortunes cannot be attributed to EU membership alone, it is still likely to be a very relevant and prevalent factor in deliberations in Italy should the Brexit vote conclude in the affirmative, thereby raising the inevitable question as to who is next.

[1] NIIP: is a country’s stock of external (foreign) assets minus its stock of external liabilities. It provides an indication of whether a country is a net creditor (lender) to the world (ie. where the NIIP is positive relative to GDP) or a net debtor (borrower) indicated by a negative NIIP. A positive NIIP is a sign of external financial strength.

[2] The credit default swap (CDS) spread is a measure of credit risk. A CDS is a financial swap agreement where the seller of the CDS insures the buyer against a reference loan defaulting, and charges a fee or spread for doing that.