Post the global financial crisis (GFC) the level of public sector debt across the world is one of the major macro-economic risks faced today. However, when deteriorating population demographics in many developed countries are over-laid on debt levels the combined problem potentially becomes acute. To illustrate the issue we examine the debt and demographic problems facing three developed economies - Japan, Italy and France - together with some possible solutions.

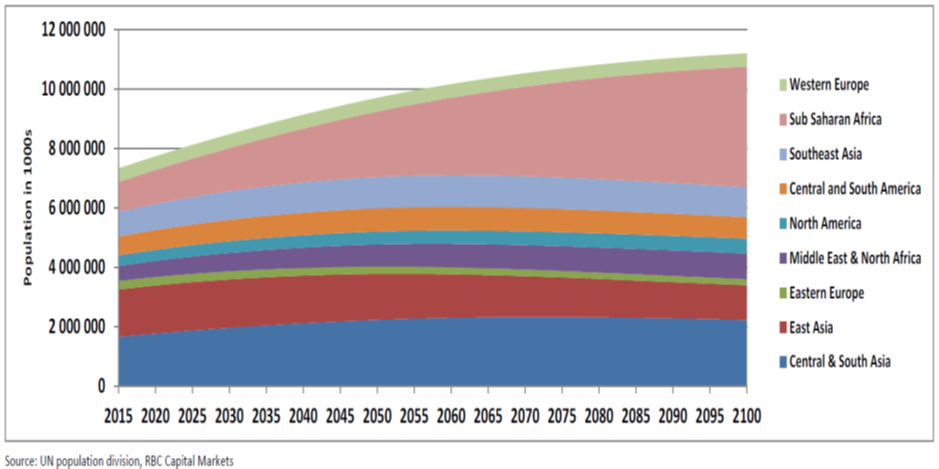

1. By 2100, the world’s population is expected to grow by 53%… but mainly in developing nations

At the turn of the 20th century the global population was ~1.65b people. By 2000 the number had jumped to ~6b+ and it is expected to grow by a further 53% by 2100.

Chart 1: UN forecast global population growth

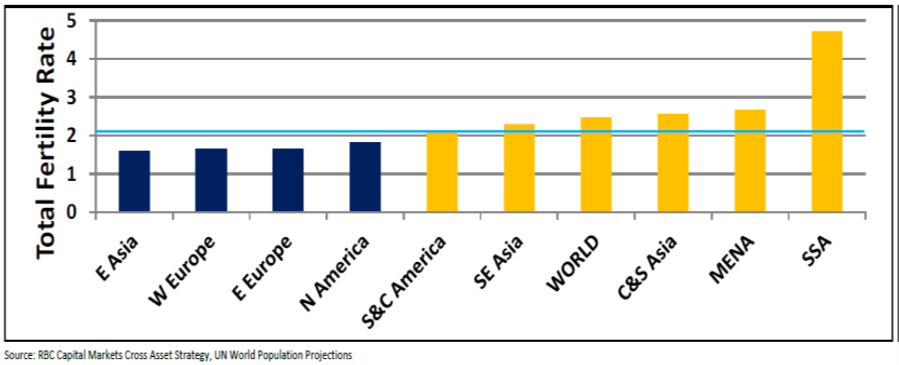

However, the expected growth will be heavily skewed to the Middle East and Africa where the UN population division expects populations to grow by 72% and 305% respectively. Western Europe’s population is expected to remain flat, while North America, bolstered by immigration, is expected to have the highest growth in the developed regions of 40%. These expected outcomes are also reflected in the forecast fertility rates shown below. In developed countries the required replacement rate is ~2.1 children/woman and that is not being achieved in Western Europe or North America.

Chart 2: Global Fertility Rates (GFR)

MENA: Middle East & North Africa: SSA: Sub Saharan Africa

2. Country specifics: combining government debt and population demographics

Combining existing government debt levels, with forecast demographics paints a worrying picture.

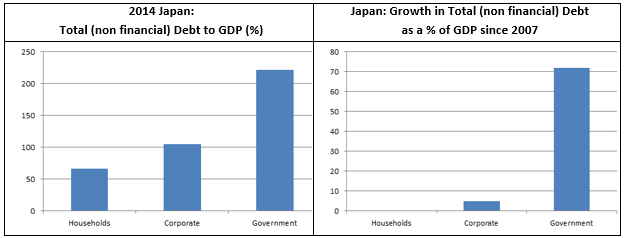

Japan

As shown in the charts below, most of Japan’s debt is at a government level (>200% of GDP), which has also been the fastest growing component since 2007. Japan continues to run fiscal deficits of ~6% of GDP meaning these debt numbers continue to escalate.

Chart 3: Japanese total debt by category

Source: Bank for International Settlements, Quarterly Review, September 2015 (A New Database on Government Debt)

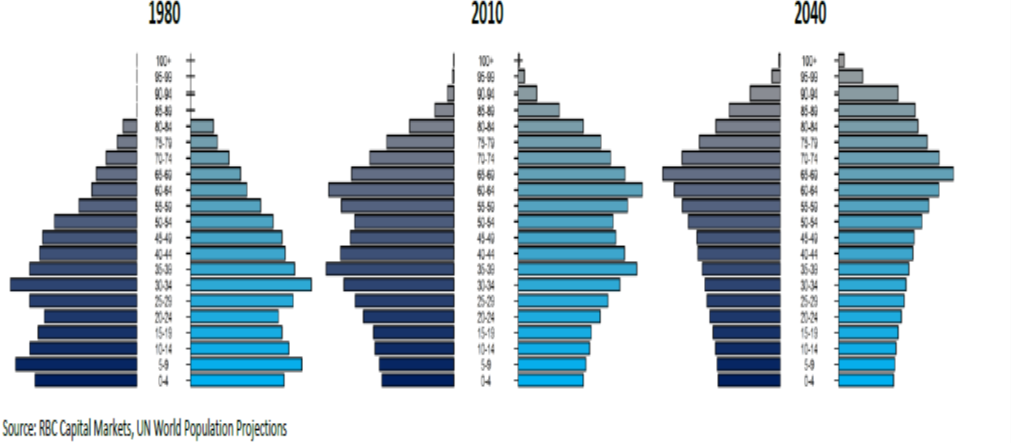

Japanese population demographics: an ageing, shrinking population

As reflected in the pyramids below, Japan has a very old population relative to global averages, a large portion is close to retirement age, and another 26% is already in retirement.

Chart 4: Japanese population pyramid (breakdown of population by age & sex (males: lhs))

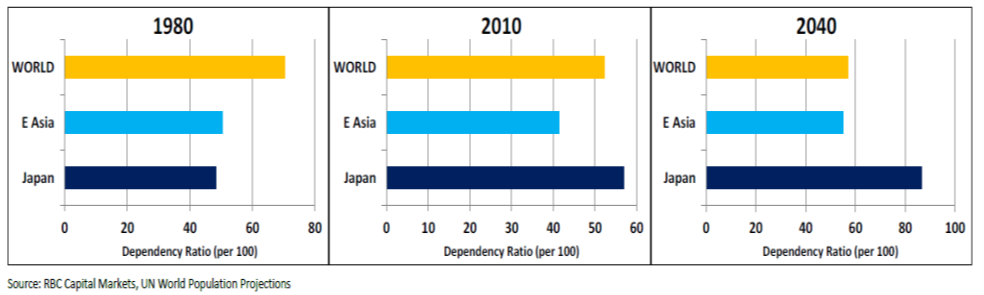

As Japan ages, its population demographics deteriorate in coming years. The total dependency ratio (TDR)[1] is expected to move from ~55%+ in 2010 to 80%+ in 2040.

Chart 5: Japanese TDR

What does this mean for public debt servicing in the future?

It is often stated that running fiscal deficits represents an inter-generational issue of ‘equity’. That is the current generation is continuing to consume borrowed public money at the expense of future generations who are left to repay the debt. What our analysis highlights in the case of Japan is that the deteriorating TDR, combined with ongoing fiscal deficits means that, unless today’s public debt is dealt with sooner rather than later, the financial burden on smaller, future, working generations will be huge.

3. Japan is not the only developed nation in this predicament

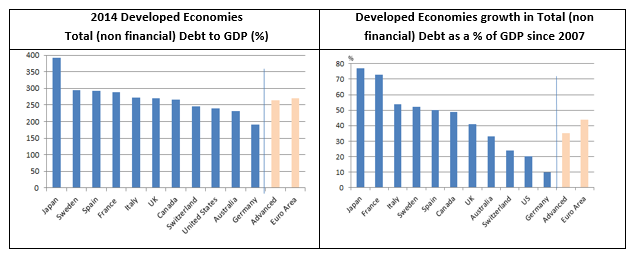

As shown in the chart below, debt levels amongst developed economies have risen sharply post 2007 as governments looked to spend their way out of the GFC.

Chart 6: Developed economies (non-financial) Debt to GDP% as at 2014

Source: Bank for International Settlements, Quarterly Review, September 2015 (A New Database on Government Debt)

Similarly, as we illustrate in Chart 2 above (GFR), like Japan, many other regions have a fertility rate below replacement, and hence a deteriorating demographic profile. For example, let’s look at France and Italy.

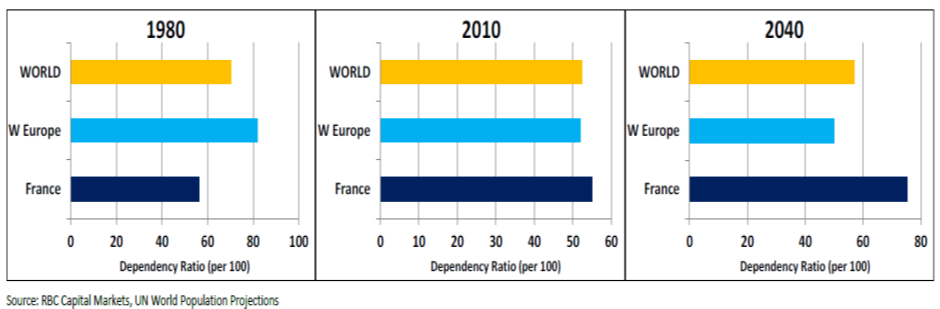

France: an ageing, shrinking population

France has government debt-to-GDP of ~100%+, continues to run fiscal deficits of ~4% of GDP, and has a TDR moving from ~50%+ of GDP in 2010 to ~70%+ by 2040 (see below).

Chart 7: French TDR

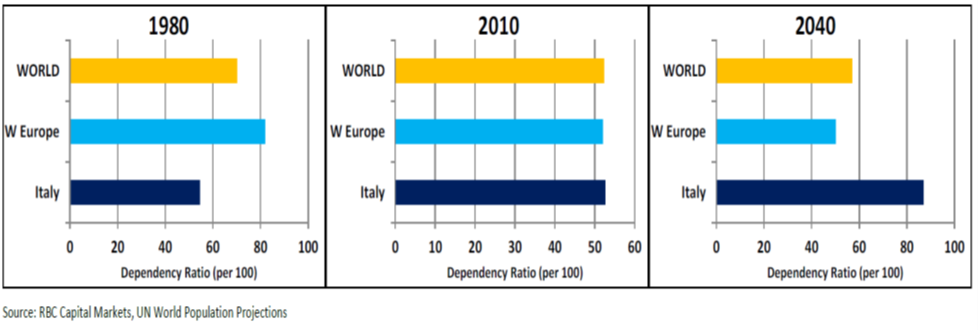

Italy: an ageing population with little or no growth

Italy has government debt-to-GDP of ~150%+, continues to run fiscal deficits of ~3% of GDP and has a TDR moving from ~50%+ of GDP in 2010 to ~80%+ by 2040 as its population either grows very slowly or begins to decline (see Chart 8 below).

Chart 8: Italian TDR

Clearly, without any policy intervention, collectively the children of inter alia, Japan, France and Italy will be burdened with a huge future financial obligation.

4. What are the policy options?

There are policy responses available for this looming crisis… but there is no silver bullet, and none are easy to implement. A co-ordinated policy response will be required.

- Foster GDP growth (ideally with a small dose of inflation):this is an obvious solution and most nations are endeavouring to achieve this via both expansionary fiscal and accommodative monetary policy. However, there needs to be ongoing spending discipline in order to moderate fiscal deficits which are the source of the growing debt pile. A modest level of inflation would also help deflate debt levels in nominal GDP terms.

- Privatisation programs:privatisations can be an important source of capital for governments provided the proceeds are used to repay debt, or reinvested in GDP enhancing expenditure.

- Increased birth rates and/or immigration:at the core of the problem faced by developed nations is a fertility rate below replacement levels. In the past, fiscal incentives have been offered to have more children (eg. Australia’s baby bonus) but the short-term impact is to worsen budget deficits and debt levels. Immigration could also present part of the solution, boosting population numbers and adding to GDP growth. However, as current difficulties in Europe highlight, large scale immigration can be problematic.

- Is fiscal policy just too important to leave in the hands of elected politicians?:Commencing in the early 1990s, governments around the world began delegating monetary policy to their independent central banks. This policy has been clearly successful over the past 2-3 decades with general price stability and economic growth the dominant thematic.

So is it time to look at something similar for fiscal policy? Some countries already have. In 2001 Chile introduced a ‘structural surplus’ rule which ties government spending to cyclically adjusted revenues, and directs government to save any surplus in a stabilisation fund. The result: Chile runs a counter cyclical fiscal policy, surpluses in boom times and modest deficits in down times, has public debt-to-GDP of ~17%, has built a substantial sovereign wealth fund, and has an S&P credit rating of AA- despite depressed commodity (eg. copper) prices.

To a similar intent, in 2003 Switzerland introduced its ‘debt brake’ rule, which lead to the EU’s 2012 ‘fiscal compact’. While the Chile and Swiss rules have been more successful than the EU’s, all would seem to offer constructive lessons in how the world can better administer fiscal policy.

- Could ‘helicopter money’ take-off?: An even more radical solution could be ‘helicopter money’ – monetary policy where central banks ‘print’ money to fund government spending, or give people cash (eg. via tax concessions). It effectively blurs the line between fiscal and monetary policy. How could it help the debt and demographics problem? It could facilitate expansionary fiscal policy to drive economic growth, while not leaving a sovereign debt hangover: sounds perfect… or crazy… maybe both?

Policy makers are aware of its merits. It got its name from an essay by Milton Friedman in 1969[1] while former US Federal Reserve Chairman Ben Bernanke earned the nickname ‘Helicopter Ben’ after referring to it in various speeches[2]. ECB President Mario Draghi was recently quoted as saying: ‘… we haven’t really thought… about (helicopter money)… (but) it’s a very interesting concept’[3]. However, and possibly guided by Argentina’s recent hyper-inflation experience, Australia’s RBA and German’s Bundesbank oppose the idea. The risks lay in the uncertain consequences of such a radical policy, in particular its impact on money supply and inflation.

5. Conclusion

What is generally well understood is that the GFC, and subsequent period of low global growth and modest inflation, has left many nations with excessive levels of public sector debt. While low interest rates are currently offering a buffer from the full pain of such a debt load, the debt trajectories of many countries remain upwards, driven by chronic fiscal deficits.

What is less well appreciated is that deteriorating (ie. ageing) population demographics in many developed countries over the next 30 years will focus the residual public debt burden onto a potentially shrinking portion of the population. The consequences of this could be dire in terms of necessary tax and spending adjustments. It is imperative therefore that governments act now to address this issue in order to preserve the lifestyle, freedoms and inter-generational equity of the children of the future.

[1] The TDR is: (The Young (aged 0-14) + Elderly (65+)) / Working Age (15-64)). It is designed to reflect the national financial burden borne by the Working Age group

[2] Wall Street Journal, 21 March 2016

[3] The Economist, 23 April 2016

[4] CNBC Europe News as quoted to Reuters, 21 April 2016