Introduction

In May 2019, we published a Global Matters article titled The changing face of US midstream assets which outlined our views on:

- Whether the midstream oil & gas sector meets 4D Infrastructure’s (4D) definition of ‘infrastructure’ as an asset class

- Some of the mistakes that midstream companies’ management teams made leading in to the 2015/16 crude oil price crash, and

- Improvements made to companies to de-risk them post 2015.

We concluded that based on improvements made to midstream companies’ risk exposures, contractual protections and financing structures, the sector exhibited the defensive characteristics of infrastructure assets and should be included in the 4D core investment universe.

In March 2020, crude oil prices plunged dramatically on the back of a double shock – namely the global contagion of the novel coronavirus (COVID-19) and a demand/supply imbalance created by conflicting Saudi/Russian production targets. The midstream names share prices crashed with the crude price.

In this follow up article, 4D Senior Investment Analysts Peter Aquilina and Mark Jones revisit the North American midstream thesis, and stress test assumptions for a dramatically lower commodity price environment and an overall slower global growth scenario – to determine whether in reality the fundamentals/earnings will prove to be infrastructure (or not) and if this collapse represents a buying opportunity.

1. To recap, are midstream players infrastructure?

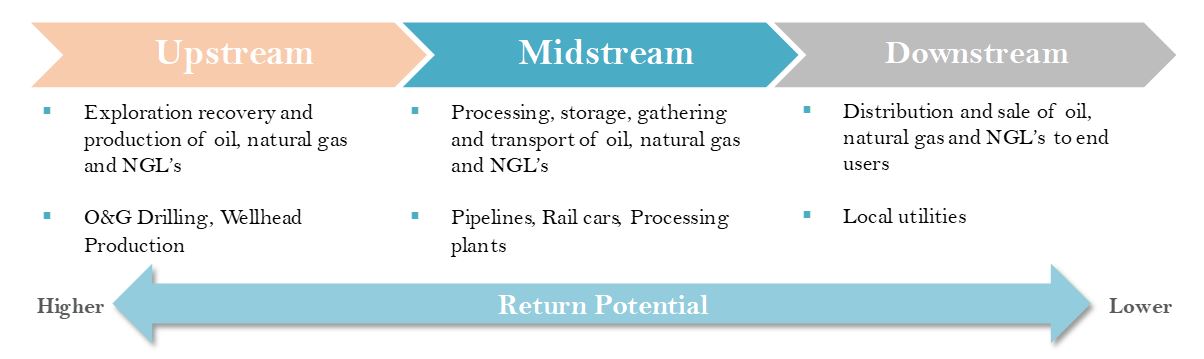

We at 4D define the ‘midstream’ sector as the infrastructure used in the transportation, storage, extraction and refining of natural gas, Natural Gas Liquids (NGLs) and crude oil. Midstream is the ‘glue’ between upstream exploration & production (E&P) and downstream refining / distribution.

The graphic below shows that there can be an extensive infrastructure value chain to transport commodities from the site of extraction via gathering lattice networks to processing plants, and to downstream markets via large volume transportation pipelines. At downstream terminals the commodities can be transported to the end customer via pipeline, rail or ship; refined at fractionation facilities; and stored or further manufactured.

Source: 4D Infrastructure

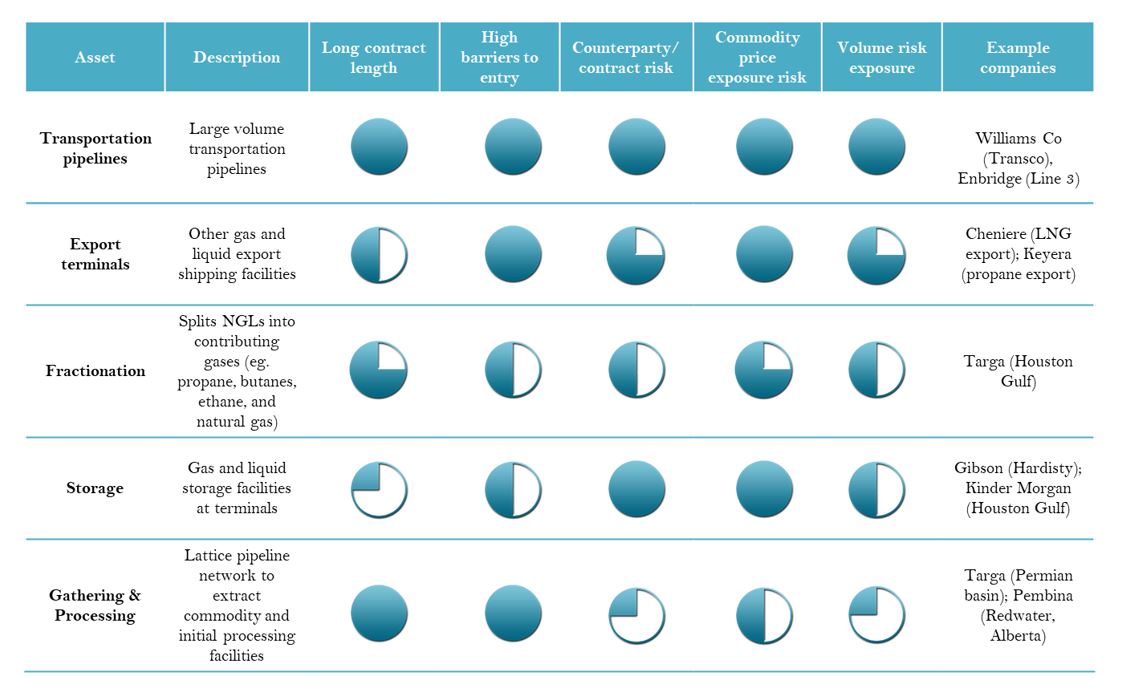

As shown in the table below, assets under the midstream umbrella perform a number of functions and have differing business risks and characteristics.

Source: 4D Infrastructure

Midstream assets are therefore heterogeneous by nature. For 4D, the investability of these stocks is determined by whether the asset characteristics meet our infrastructure definition.

As a recap, 4D defines ‘infrastructure’ as the owners and operators of regulated and/or user pay assets with the following attributes:

- monopolistic market position or one with high barriers to entry;

- inflation hedge within the business;

- visible and resilient earnings stream;

- strong cash generation;

- strong regulatory regimes or contracts;

- long dated assets;

- acceptable levels of gearing; and

- ESG considerations.

In our earlier article we assessed the players according to this definition, considering both pre and post 2015/2016 business models. We highlighted what had gone wrong for the midstream companies in 2015/2016 and how management responded in restructuring business models to a point that the assets exhibited many, if not all, the characteristics we look for in infrastructure assets.

We concluded that the ‘new’ midstream asset profile had many of the necessary characteristics; such as monopolistic market positions, visible and resilient earnings, strong cash generation, long dated assets and acceptable levels of gearing.

We also concluded that the listed market had not fully recognised the changes that had occurred in the structure of the midstream sector, and the stocks were still moving in sync with commodity prices. It was – and is – our belief that over time, the earnings disconnect of the midstream players with commodity prices should be recognised by the market, leading to a sector re-rating towards fundamental value.

In the same article, we identified a subset of midstream companies which represented strong investment propositions for investors with reasonable growth profiles and strong cashflow generation, and which had been under-appreciated by the market on a fundamental valuation basis. This included Cheniere and Kinder Morgan, with their low price and volumetric exposures to commodity prices, significant cashflow generation and undervaluation by the market.

So given little sector re-rating and more recently the dramatic sell off – what did we get wrong, or does the market still have it wrong?

2. The price collapse of crude approaching US$20/bbl

Factors impeding oil and gas demand – demand drivers

Through 2019, global oil and gas demand was maligned – in part as a result of the trade war between the US and China, and in part due to concerns of overall slowing global growth. The investment community thought there were signs of potential improvement when in January 2020 the Chinese and US governments signed Phase 1 of a trade deal between the countries, which reduced tariffs on some Chinese imports into the US in exchange for Chinese commitments to purchase more US agriculture, energy and manufacturing goods; and address some US complaints about intellectual property (IP) practices.

Unfortunately for the sector, following the announcement of Phase 1 of the trade deal, global demand for oil and gas remained maligned in Europe and Asia as a result of a relatively mild winter across the northern hemisphere; and the arrival of COVID-19 in China, which rapidly spread to other parts of Asia, followed by Europe and then the globe. As the Chinese government took drastic measures to curb the spread of the disease by shutting down entire cities, they also put a halt to industrial and commercial activity for a period, significantly impacting oil and gas demand. This was subsequently followed by other economies across the globe as the disease crossed borders and continents.

OPEC response – supply drivers

In the context of a declining demand for oil, the Organisation of the Petroleum Exporting Countries (OPEC) held an Extraordinary meeting of OPEC countries on 5 and 6 March. However, the OPEC and OPEC+ countries, led by Saudi Arabia and Russia respectively, couldn’t come to an agreement on planned production cuts of 1.5 million barrels per day (Mbbl/d). There are a few suggestions as to why Russia would not agree to the production cuts, two of which are:

- It wanted to squeeze out of the market some of the higher debt-laden US shale drilling companies, taking production market share from the US; or

- It has internal budgetary pressures which require significant earnings from Russian E&P players, and a further cut to production in the context of continual demand declines would only result in reduced earnings in the short term.

Saudi Arabia reacted to Russia’s refusal to agree to the production cuts by launching a price war, lowering its official April crude export prices by $6-$8 per barrel. It also pledged to increase its own daily production to 12.3 Mbbl/d by April, up from around 9.7 Mbbl/d (a 27% increase in planned production). This resulted in US crude prices (as measured by West Texas Intermediate, or WTI) falling 26% to $31.13/bbl on 9 March (Brent crude prices fell to $34.36/bbl), the lowest level since February 2016, with fears that the crude price as measured by WTI could actually fall below $30/bbl – which it subsequently did on 16 March. This did not prove to be a floor, with subsequent falls on successive days. At the time of writing (20 March 2020), the WTI oil price was sitting at $22.63/bbl (Brent crude price at $29.00/bbl), having nearly touched $20.

Analysts believe that at these prices, neither Saudi Arabia, Russia or US players can be cashflow positive for extended periods of time. Some players may have short time mitigants which keep their drilling operations cashflow positive, such as utilising existing well inventory or having price hedges in place, but these dissipate over time. Therefore, economic rationalism translates this to a temporary, short-run ‘price shock’. So the question that no one can answer with certainty is who will blink first? Or when will the parties come back to the table to negotiate production cuts and improved crude prices?

3. If midstream is infrastructure, why has the oil shock hit so hard?

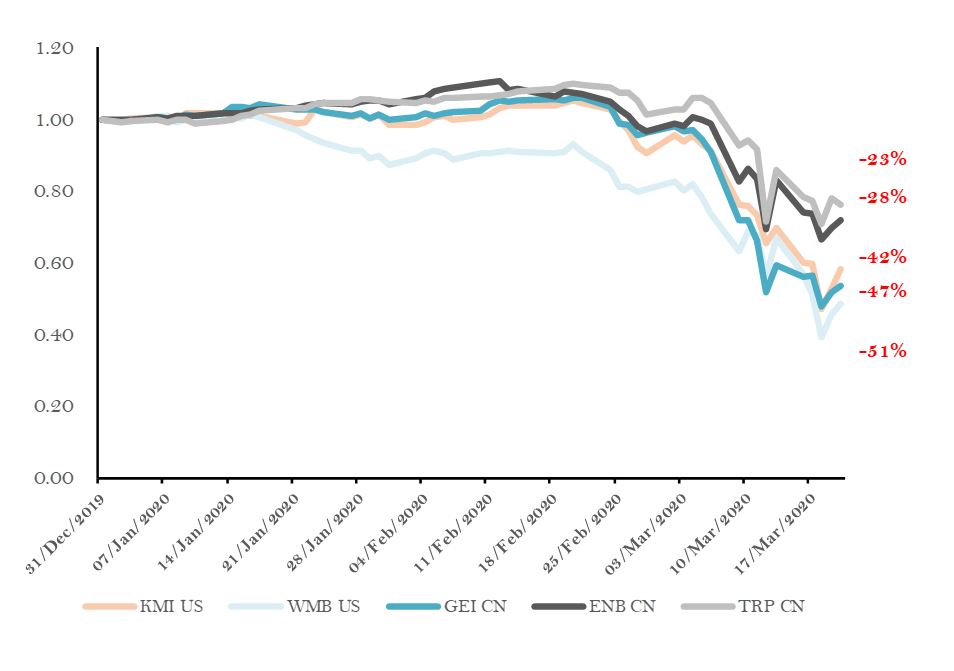

The combination of the demand side (COVID-19 and a mild winter) and supply side (OPEC fallout) impacts on oil and gas prices has resulted in significant declines in midstream share prices. A summary of share price declines for key players is depicted in the following chart.

Source: Bloomberg as at 20 March 2020

Assuming economic rationalism prevails, current crude prices are a short/medium term phenomenon. The impact of this still generally raises the following concerns for midstream companies:

a) Counterparty risk (e.g. financial distress of producer customers operating in low productivity basins)

b) Direct impact of (lower) crude oil prices

c) Indirect impact of prices on (lower) crude oil volumes, and

d) Deferral of growth capital.

In our previous article, we outlined that following the restructuring of companies post 2015/16, recommended core investment holdings are in a much better position to withstand the risks created by a short-term commodity price slump. Therefore, it is our view that for the reasons discussed in detail below, the prevailing market share price reductions depicted in the chart above are an overreaction and don’t properly reflect the sector’s ability to withstand short-term oil and gas price shocks.

4. Stress testing the sector

Mitigants to counterparty risk

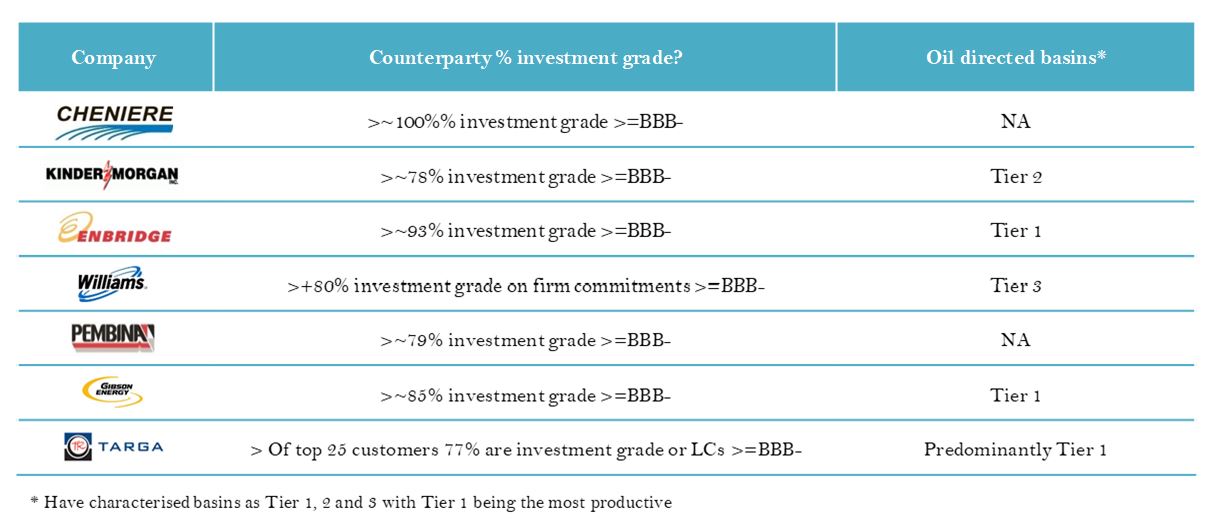

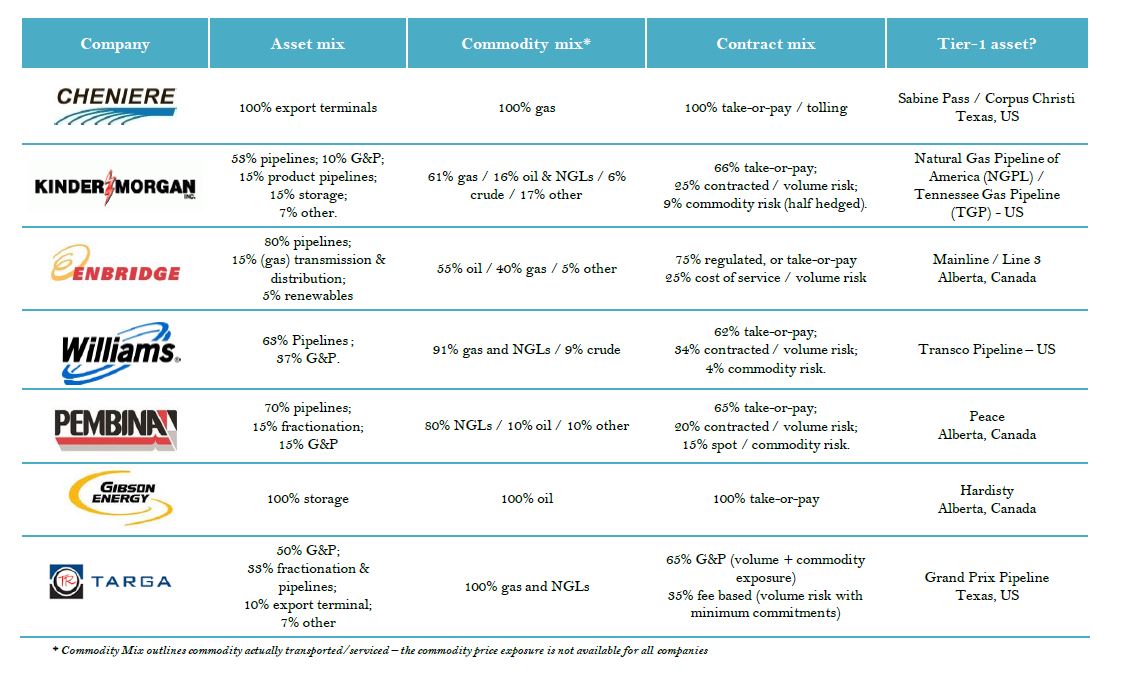

We revisited our midstream companies to assess the credit quality exposure of their counterparty customers; and the quality of basins that the midstream companies operate in, as determined by the production cost to drill oil and/or gas (lower cost – higher quality). This information is summarised in the table below.

Source: Company presentations and 4D Infrastructure

On balance, we believe many of the midstream investment companies are not significantly exposed to poor credit quality customers. During historical crude price collapses like 2015/2016, when midstream counterparties have encountered financial distress and/or filed for bankruptcy, if those counterparties operated in lower production cost (higher quality) basins (Tier 1 and Tier 2), the bankruptcy administrator has continued drilling operations through the process. With time, another E&P player has taken over operations with little to no detrimental contractual impact for the midstream operator.

The outlier above in terms of basin quality is Williams Company, operating in a Tier 3 oil directed basin. However, oil directed drilling only contributes a small percentage to overall gross margin (14% or less); so while a portion of this margin is at risk, the overall contribution to value is small and has been more than factored into current share prices.

Midstream companies have limited direct crude oil price linkage

Our midstream investment companies have limited direct price exposure to either crude or gas prices. The contract structures through which most companies are remunerated are fee-based, often with minimum volume or take-or-pay provisions. Where companies do have direct price exposure, there is a policy to reduce this exposure through the utilisation of financial hedges. The ‘Commodity mix’ column in the table below outlines our investment companies’ contractual exposure directly to commodity prices, and indirectly to volumes serviced.

Source: 4D Infrastructure

The contractual terms are a key component to our midstream ‘infrastructure’ thesis, as they underpin the earnings resilience of the assets even in volatile commodity environments. The types of contracts commonly used in the sector to immunise from commodity prices are summarised below.

- Take or pay – a contract provision obliging the buyer to pay for a certain minimum quantity of product, whether or not the buyer actually takes that quantity during the stated period. Usually stated in terms of an absolute quantity, or a percentage of total contract quantity, over a specified period of time.

- Cost of service – a contract provision representing total cost of providing service, including operating and maintenance expenses, depreciation, amortisation, taxes, and return on capital / rate base. Generally the cost of service is the same as its revenue requirement. Importantly, lower throughput or revenues lead to higher tolls as the pipeline’s costs are shared by the remaining shippers on the system.

- Fee for service – a contract provides for a fixed fee per unit of production sold or service provided, not subject to commodity price risk but subject to volume risk.

- Fixed toll – a contract which does not vary with changes in throughput. Usually based on fixed costs and throughput for a test year.

Midstream sector has largely maintained oil/gas volumes and earnings through historical commodity price weakness

Although the midstream oil/gas sector does have indirect volumetric exposure to crude prices, during historical periods of crude oil price weakness the sector has experienced relatively minor volume and earnings reductions, if any at all (company dependent). Crude price weakness in 2015/2016 concluded a crude price super cycle that began in the early 2000s, and was contributed to by increasing supply from the US shale boom which began around 2010/2011. During the 2015/2016 period of price weakness, the WTI crude price fell as low as US$24.45/bbl and the period of sub US$50/bbl prices lasted for approximately 12 months. Through this period, most midstream companies maintained volumes serviced or experienced only small declines.

Historically, companies have largely been able to maintain oil/gas volumes serviced.

- Oil E&P players respond to the price weakness by:

- lowering marginal cost of production by increasing volumes (e.g. optimising / increasing production on existing wells);

- optimising costs (e.g. negotiating better rates with oilfield service companies and consolidating volumes to third-party infrastructure); and

- de-leveraging balance sheets (e.g. divesting non-core infrastructure).

- Midstream volumes are supported by:

- utilising a fully integrated value chain – being the only solution to transport and service crude volumes from the supply basin to the demand centre;

- contractual terms, which may include take-or-pay of Minimum Volume Commitments (MVCs); and

- new producers taking up displaced volumes in economic basins of financially distressed E&P players.

We expect the E&P players will again instigate optimisation methods and in the absence of the entire sector going bust, volumes of those financially stressed E&P players will eventually find a home elsewhere – as long as the cost curve is met by prevailing crude prices, which varies depending on the basin drilled.

Deferral of capital growth projects

Midstream sector assets are capital intensive / long-lived, with capital allocation based on long run return requirements. Companies are likely to target stronger cashflow generation through deferral of growth projects, or alternatively reviewing existing projects with higher return requirements. This is to sure up cashflows in this uncertain time, and strengthen the balance sheet in a period of plateauing or even falling operational earnings.

To date we have already seen a number of midstream companies announce cuts or deferral of growth capital projects. Pembina announced it was deferring C$0.9 - $1.1 billion in capital projects in 2020 (representing 40-50% of 2020 forecast capex) to support free cashflow generation in the year. Similarly, Targa Resources announced it was cutting its 2020 capital investment guidance by US$400 million (representing 30-35% of budget), and also significantly cutting its dividend.

Despite cuts to capital projects, E&P companies are still incentivised to endorse midstream sector capital investment due to:

- economies of scale / lowering unit cost – midstream companies are able to consolidate assets in the gathering, processing, transportation and sometimes fractionation/export of commodities to provide a ‘one-stop’ solution for E&P players at minimum cost;

- access to new markets (e.g. export terminals) – midstream companies often provide additional demand markets for the E&P players commodity, which can include different domestic trading/demand centres or international markets; and

- increasing value of product (e.g. propane dehydrogenation) – through additional servicing of the commodity at the more downstream end of the supply chain, midstream players can extract additional value out of the commodity on behalf of the E&P player.

5. Specific analysis of 4D’s recommended midstream companies

In light of the market sell-off of energy and midstream companies resulting from weak crude prices following the expected short-run demand/supply imbalance, we have reviewed the extent to which our investment companies are exposed to the weak commodity price; and undertaken downside scenario testing to understand the potential for financial distress and resulting valuation impact. Our conclusions are as follows.

- Our initial thesis that these assets do exhibit the fundamental characteristics of infrastructure assets remains intact. However, we continue to consider this on a case by case basis or asset by asset assessment to ensure we are exposed to the names offering the highest quality/value opportunity.

- The sector will be subject to ongoing price volatility until the market can recognise the disconnect between select company earnings and commodity pricing, which should play out over time. For example, Pembina reaffirmed its FY20 EBITDA guidance post price shock.

- Certain sub sectors of the midstream value chain have greater earnings exposure to crude price downside than others (e.g. G&P, marketing), while others are largely immune (pipelines).

- Factoring in worst case scenarios, regardless of where a company operates along the value chain, the sector has been oversold.

- The current market seems to be pricing in a significant probability of financial distress – none of our analysed companies appear at significant risk of this scenario in the immediate future.

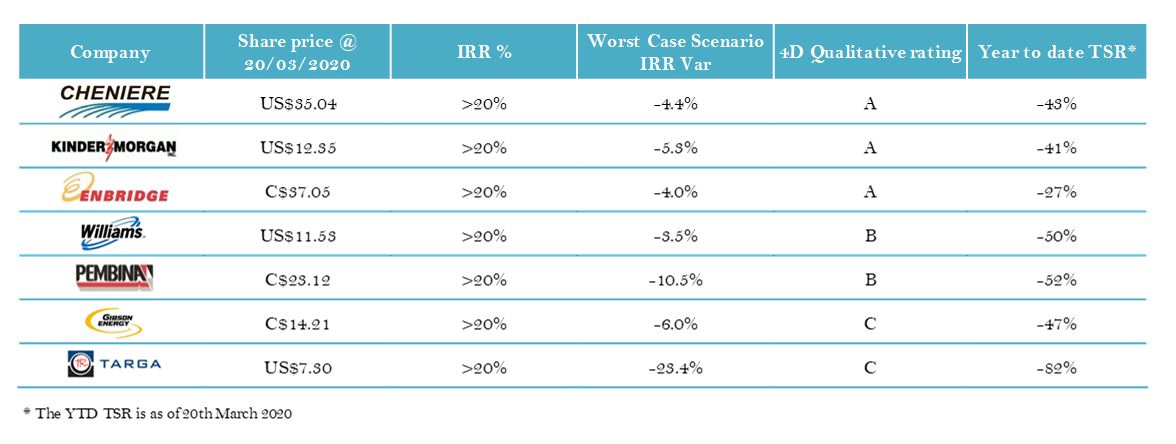

- Considering revised base case scenarios and prevailing share prices, all companies represent five-year IRRs in excess of 20%. This makes them a Strong Buy according to 4D’s valuation methodology.

- A significant near-term risk to achieving these returns exists if private investors with significant capital and longer-term investment horizons opportunistically bid for these companies at their depressed share prices. A ‘healthy’ premium could get a transaction done, but still represent a significant discount to fundamental valuation. This is a real concern for us at these levels. Company boards and management teams hopefully exercise strong governance and good judgement in insisting that real fundamental value is recognised and paid by potential acquirers.

A summary of YTD return performance and resulting quantitative and qualitative ratings under revised base cases are summarised in the table below. We have also included return analysis of worst-case scenarios against base cases.

Source: 4D Infrastructure

We also conclude that none of our portfolio names are at a significant probability of financial distress unless this irrationally low crude price is maintained well into 2022. The most at risk is Targa Resources, and even though the worst-case scenario shows an IRR variance of more than -20%, the company is still investible in this scenario and avoids financial distress.

Appendix

We have undertaken detailed case studies for a selection of the midstream names. Our fundamental analysis, stress testing and conclusions can be found here, but a summary follows.

- Cheniere Energy – highly contracted business model with substantial expansion opportunities. Strong management team has placed the company as a first mover in the industry. Its fundamental value is not significantly impacted by the current market dynamics and it remains a Strong Buy on fundamental earnings quality.

- Kinder Morgan – a key player in the transport of energy from production to demand centres across the US, with earnings significantly underpinned by volume protected contracts. Offers cashflow stability during commodity price volatility – the worst-case scenario still offers an attractive valuation.

- Enbridge – a diversified infrastructure player based in Canada with a focus on crude transportation pipelines and gas transmission/distribution networks. Minimum volume protections supporting 94% of 2019 EBITDA. We conclude that Enbridge’s sensitivity to crude oil price shocks is minimal due to diversity of earnings and quality of assets / contractual agreements, which are considered significantly undervalued at current market share price.

- Williams Co - vertically integrated midstream natural gas company that is central to the provision of gas to demand centres on the east coast of the US. Owns and operates a set of irreplaceable natural gas pipeline assets including Transco. We believe Williams Co is potentially a ‘winner’ as a result of the recent cuts to global crude prices by OPEC, which is supportive of natural gas prices. It remains a Strong Buy.

- Pembina – primarily focused on NGL processing, transportation, fractionation and storage, with assets located in Tier 1 basins in Canada. We believe Pembina’s demonstrated capital discipline and stronger contractual terms of its assets (relative to NGL midstream peers) are not being recognised by the market. Maintain Strong Buy.

- Gibson Energy – a Canadian midstream player primarily focused on crude storage assets. Oil storage in Canada is based on operational flexibility rather than speculation (e.g. contango / backwardation), and therefore portrays low volatility. We believe Gibson will be insulated from low crude prices as its oil storage assets in Hardisty and Edmonton offer an essential service protected by ~10 year take-or-pay contractual terms. It remains a Strong Buy.

- Targa Resources – key positions in some of the lowest production cost oil & gas basins in the world in the Permian and Bakken basins, and is able to capture fees throughout its integrated vertical supply chain. We believe the current uneconomic level of commodity prices (especially crude) will recover in time for Targa to continue its growth trajectory and de-gear its financial structure, although there is a concern if crude prices stay this low for an extended period of time. Arguably the riskiest position in the current environment, but worse case more than priced in.

Download a copy of this article here.