This is the abridged version of the article. To view full article including the Appendix, click here.

Investment in electricity transmission infrastructure is an essential prerequisite for facilitating a smooth energy transition. In Australia, the sector faces significant hurdles to enable essential transmission investment in a timely manner. This exacerbates network congestion and impedes the installation of new renewable generation capacity, which undermines progress towards the nation's overarching net zero objectives.

Key drivers of transmission investment

The phrase "no transition without transmission" is frequently used to underscore the crucial role of transmission infrastructure in facilitating the energy transition. Australia is not exempt, with a substantial and multidecade investment in transmission infrastructure paramount to ensure transition to renewable energy and increased electrification. The key drivers of the need for significant transmission investment are outlined below.

Electricity demand growth

Australia’s Integrated System Plan (ISP – see Appendix) forecasts that electricity demand will nearly double from just under 180 terawatt hours (TWh) per year today to approximately 320 TWh by 2050. Underpinning this demand growth is population growth, economic growth, and importantly, electrification (replacing of technologies or processes that use fossil fuels with electrically powered equivalents).

New generation capacity

Australia’s demand growth expectations, coupled with federal goals of achieving 82% renewable electricity generation by 2030 (up from about 35% today) and net zero by 2050, requires substantial investment in new renewable generation capacity.

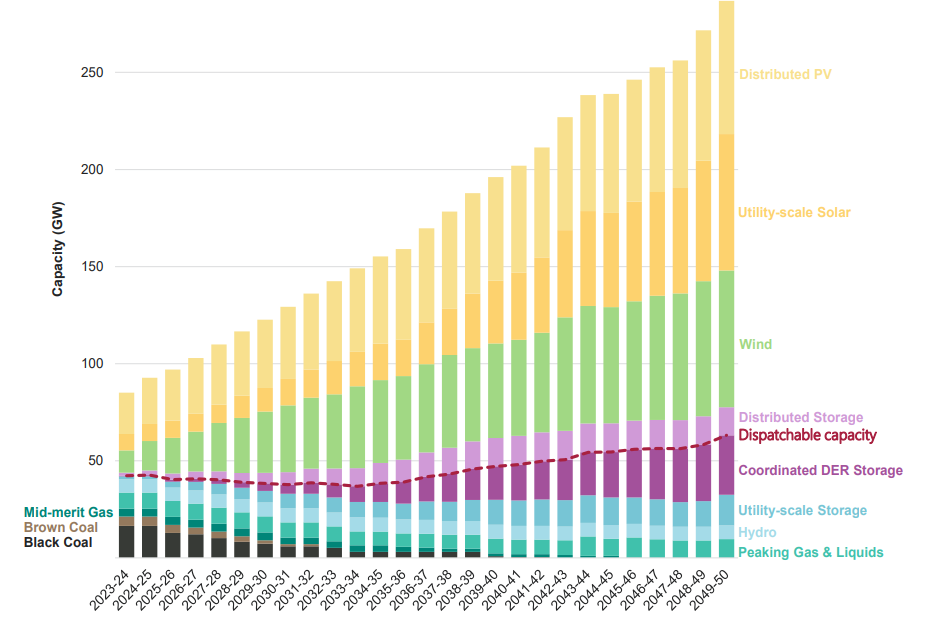

ISP forecast that these goals will need 120 gigawatts (GW) of additional utility-scale renewable generation, and at least 45GW of storage – that is a nine-fold increase in capacity from 16 GW of large-scale renewables in 2022 to 44 GW in 2030 and 141 GW by 2050. That’s over a doubling of capacity every decade. At the same time, Australian Energy Market Operator (AEMO) suggest firming capacity would need to increase to 63 GW by 2050. This renewable growth requires connection to the system, otherwise it’s largely meaningless. This connection supports security of supply and will require significant state interconnection if the national system is to operate efficiently.

Security of supply

As fossil fuel generation decreases in importance, and intermittent renewable generation starts to dominate, investment in low-emission firming and dispatchable capacity is also required. Currently, the National Energy Market (NEM) relies on 23 GW of dispatchable firm capacity from coal-fired generation, 11 GW from gas fired and liquid-fuelled generation, 7 GW from hydro generation, and 1.5 GW from other dispatchable energy storage. AEMO’s optimal development path calls for the NEM’s firming capacity to increase to 63 GW by 2050, including the replacement of coal-fired generation. This translates into approximately 43 GW of new firming capacity.

Forecast NEM capacity to 2050, Step Change scenario

Source: AEMO, 2022 Integrated System Plan (ISP)

Capacity constraints

Congestion occurs when overloaded transmission lines are unable to carry additional electricity flow without exceeding thermal, voltage and stability limits designed to ensure reliability and maintain the integrity of the system. Due to risks associated with overheating or system failure, the transmission system operator must instruct generators to adjust their dispatch levels to accommodate the constraint. Congestion has commercial consequences and, in particular, creates risks for all stakeholders, particularly the generators (project economics) and retailers (higher prices). Further investment in the transmission network is essential in alleviating congestion inefficiencies which are already in play.

Technology evolution

Technology poses another constraint as newer renewable energy projects, especially large-scale ones, often operate at higher voltages than the existing transmission network was designed to handle, resulting in a suboptimal utilization of power outputs. New investment in the transmission network is essential to alleviate potential bottlenecks and reconfigure existing lines to suit the emerging mix of renewable generation and storage.

Interconnection

The decentralisation of renewable resource and an increasing composition of renewable capacity to the generation fleet heightens intermittency risk. Energy production can fluctuate between various regions, hence greater interconnection is required to facilitate access to regions/states/territories, producing excess supply when the other is experiencing low energy output. Interconnection supports security and stability.

- On 28 September 2016, severe weather in South Australia damaged multiple transmission lines. Due to faults across the transmission network, nine wind farms activated a protection feature, resulting in the withdrawal of 456 MW of capacity in less than seven seconds. The reduction in wind generation caused a significant increase in imported power flowing through the Victoria–SA Heywood Interconnector, which subsequently became overloaded and activated a special protection scheme that tripped it offline. The SA power system became islanded (separated from the rest of the NEM), and with insufficient generation to match the demand load, the state was dealt with rolling blackouts with over 850k customers impacted.

- On 13th February 2024, severe weather damaged transmission lines in Victoria, which prompted the 2.21 GW Loy Yang A power (generates approximately 30% of Victoria’s power requirements) to drop offline. The Moorabool to Sydenham transmission lines tripped, and multiple other generators were disconnected from the grid. More than 500k customers were impacted and left without power. AEMO were forced to instruct AusNet Services, a transmission & distribution operator, to commence load shedding (an absolute last resort to protect system security and prevent long-term damage to system infrastructure). At the time of the outage, Victorian wholesale power prices increased to $16,600/MWh, compared to $60.39 in Queensland and $299.98 in NSW.

These incidents underscore not just the significance of transmission interconnection, but also the importance of ensuring appropriately sized capacity.

The Age, ‘Weeks to restore’: Half a million homes without power after extreme weather (February, 2024)

Topography

A key feature of energy transition is the replacement of centralised thermal generation. There is a vast geographic dispersion of renewable energy sources to demand centres and to existing transmission infrastructure, as renewable generators are often built in regional areas where solar and wind energy are abundant. The NEM is already one of the most dispersed and thinnest grids globally, which is not supportive of a fragmented generation topography.

Ageing infrastructure

Further compounding the issue is that over 75% of our existing transmission network is over 50 years old. There is not only the need to build new infrastructure, but our ageing network must also be upgraded or replaced. Upgrading the existing infrastructure will enhance its reliability, safety, and efficiency. Upgrades reduce the risk of equipment failures and power outages, and new systems help to better detect and respond to potential safety hazards, such as overloads.

While transmission systems can experience outages from severe weather, conversely transmission system failures can cause damage to the surrounding environment. Downed lines, vegetation contact, or component failures can produce fault currents and sparks that may ignite fires under hot, dry, and windy conditions. Observations around the world indicate that higher temperatures, heavily loaded lines, and ageing infrastructure mean that fire ignitions from power systems are becoming more prevalent. In our article, Extreme weather risks and their impact on investors, Peter Aquilina (Portfolio Manager - Sustainability) discusses how climate-related events can impact infrastructure operators and their investors.

Scale of needed transmission investment

According to AEMO’s optimal development path within the 2022 ISP, Australia needs to invest approximately A$30 billion in transmission infrastructure out to 2050. While this represents just 9% of the total A$320 billion forecast investment required in the electricity system out to the same period, it’s essential to ensure that the rest of the system targets can be realised. These new lines would represent around 25% of the length of the existing transmission network today and is more than twice the distance across Australia at its widest point (4,000 km).

Source: AEMO, 2022 Integrated System Plan (ISP)

The ISP’s actionable transmission investment consists of five key transmission projects in NSW, Victoria and Tasmania. Collectively, these projects will cost around A$14 billion, however, are forecast to deliver net market benefits of A$28 billion (returning in excess of two times their cost), enable energy transition by unlocking over 20 GW of new renewable generation capacity, and manage key risks identified above. The five projects (1) HumeLink, (2) VNI West, (3) Marinus Link, (4) Sydney Ring and (5) New England REZ Transmission Link, are all currently being assessed for regulatory approval, or should begin that process soon.

- HumeLink is 360 km of new transmission lines, and new or upgraded infrastructure which will connect Wagga Wagga, Bannaby and Maragle. The project is estimated to cost around A$3.3 billion[1]. HumeLink will provide capacity for circa 2.6 GW of additional renewable generation to connect to the network.

- VNI West (Victoria to NSW Interconnector) is a proposed new 500 kV double circuit transmission line connecting New South Wales and Victoria. The final route for the New South Wales section of the VNI West is yet to be finalised, however the total length of the project is expected to exceed 800 km and cost approximately A$3.5 billion[2]. The project will support upwards of 3.4 GW of new renewable generation capacity.

- Marinus Link is a A$5.1 billion[3] 340 km electricity and telecommunications interconnector between Tasmania and Victoria. Marinus Link will support 1.5 GW capacity, equal to the power supply for 1.5 million Australian homes.

- The Sydney Ring is a A$1.5 billion proposal to link New South Wales’ coastal load centres with the state’s various renewable energy zones. The project will link EnergyConnect, HumeLink and VNI West via new 500 kV transmission lines from Bannaby into the Sydney western suburbs connecting to the ‘inner’ 500 kV system, increasing transfer capacity by approximately 5 GW.

- The proposed A$1.3 billion New England Transmission Link aims to support the delivery of the New England Renewable Energy Zone (REZ) in the New South Wales New England region. The REZ has an intended network capacity of 8 GW and is expected to deliver up to A$10.7 billion in private sector investment.

Various sources suggest that the ISP’s A$30 billion transmission infrastructure investment is understated, representing but a fraction of the total transmission development actually required. Individual states and network operators also devise their own forecasts and assumptions for network plans separate to that of AEMO. Powerlink, Queensland’s electricity transmission system operator, for example, projects that the state alone will require investment of over 37,200 km of new transmission lines by 2050; enough to circle the earth.

Power struggle

Despite the obvious need, investment in Australia’s electricity transmission network has been woefully slow and could derail national transition targets. This is a function of the highly regulated nature of the business which has created obstacles from planning, through construction to operation.

For example, it took nearly a decade for Project EnergyConnect, the interconnector connecting NSW and South Australia, to reach financial investment decision and begin construction. In particular, securing approval for the Regulated Investment Test for Transmission (RIT-T – see Appendix) took four and a half years alone. The project was budgeted at about A$1.5 billion when it went through a cost-benefit analysis, however, is now expected to cost A$2.4 billion. Another example is the Central West Orana renewable energy zone, where the price of transmission infrastructure and preliminary works to connect the zone to the broader network had originally been costed at about A$400 to $800 million per the 2020 ISP, however, is now expected to cost about A$3.2 billion.

The key challenges to execution of this much-needed transmission investment are outlined below.

Regulatory framework

Appropriate market design is a key parameter in creating incentives for efficient transmission investment. The existing regulatory framework for assessing transmission investment was not designed for the unprecedented scale and complexity of major transmission projects, nor the pace at which the energy transition is progressing, with the transmission development process taking up to six to ten years. This leads to protracted timeframes for planning assessment and project approval, and/or hinders project economics.

Specifically, the framework places too much emphasis on the affordability aspect of the energy tripod (reliability and sustainability being the other two). The RIT-T takes an overly narrow and arbitrary view on the disproportionate costs incurred by customers of the respective Transmission Network Service Providers (TNSPs) to fund these projects, rather than a more balanced approach towards accounting for the total benefits, which will flow to customers in other networks, provide the ability to unlock/connect new renewable generation capacity and improve the overall network stability.

Costs and financing

AEMO's actionable ISP projects alone are estimated to cost significantly more than the current transmission regulatory asset bases. Concessional funding, project-based assessments and other initiatives are being explored to support development and construction.

Supply chain

The tight labour market and supply chain price shocks could further hinder project economics and timely delivery of transmission projects. Network operators have more recently grappled with increased lead times for essential components required to build large scale transmission infrastructure (reactors, transformers, line conductors and steel). Additionally, labour and skill shortages are a significant factor challenging the build out of renewable generation and transmission infrastructure, especially in regions with tight labour markets.

Social license

The successful development of transmission projects relies heavily on obtaining social license and community support. Issues such as impacts on local economies, the environment, fire risks, and opposition to overhead lines can derail investment in transmission infrastructure. Therefore, transmission businesses must make a serious effort to engage with and address the concerns of communities, First Nations people, and landholders. Without social license and careful consideration of impacted communities, projects may face delays, leading to missed consumer benefits such as reduced future energy costs, maintained energy system security and reliability, and support for the transition to net zero emissions.

Powering transmission

While there’s no silver bullet, recent consultations from industry, government and community bodies have outlined several recommendations to address the transmission investment gap:

Regulatory reforms

The Australian Energy Market Commission (AEMC) reviewed the Australian Energy Regulator’s (AER) RIT-T to help facilitate key enablers of investment, such as an appropriate economic assessment framework. This includes cost estimation accuracy and alternative economic remuneration methodologies on a project-specific basis, financeability, streamlined permitting processes, and social licence. Additionally, the AER recommended greater certainty of early works cost recovery (through a separate contingent project application). More and earlier planning activities could also reduce delays to later project stages by improving the building of social licence, economic assessments and earlier identification of potential project barriers.

Furthermore, there should be more regular reviews of the appropriate regulatory framework to ensure that it’s evolving with the continuously changing generation mix, generation supply and patterns of consumption.

Government funding and support

Mechanisms to support investment include lower-cost/concessional funding sources, leveraging government credit ratings, and/or potential community buy-in. In addition to the stat- based renewable/emissions targets, recent initiatives and developments across the market include:

- Federal: Labor’s ‘Rewiring the Nation’ program - investing A$20 billion to modernise the electricity grid and infrastructure. Recently announced (in November 2023) capacity investment scheme, targeting 32 GW of new capacity nationally.

- NSW: the state’s Electricity Infrastructure Roadmap - intended to coordinate investment in transmission, generation, storage and firming.

- Victoria: seeking tenders for six renewable energy zone (REZ) projects and announced plans to launch Australia’s offshore wind industry.

- Queensland: committed to develop three REZs across the state.

System planning

Enhanced coordinated planning across the entire energy sector and system requirements will allow for a synchronous delivery of transmission infrastructure, new renewable and storage capacity, and withdrawal of the fossil fuel fleet. Development of a national plan, or even more detailed state-based plans, will assist in progressing key development and operational milestones across the sector. Ongoing refinement would allow for the plan to adapt to any changes or hurdles that may arise.

Community engagement and compensation

Social licence is essential for communities to support energy infrastructure impacting their lives. Stronger stakeholder collaboration, working with the affected communities, establishing a feedback loop and providing adequate compensation to relevant parties aim to address factors that can speed up project delivery.

Global investment opportunity

Following the privatizations of Spark Infrastructure (2021) and AusNet (2022), the opportunities for direct investment in the domestic networks have become limited. However, the investment itself is crucial for a number of listed operators with renewable pipelines, as we believe transmission infrastructure could be the biggest inhibitor to execution.

We recently attended a Lenders and Investors Day in November 2023, held by renewables operator Acciona (ACE SM). Management echoed our concerns, flagging one of the key inhibitors to progressing its 13 GW pipeline in Australia (target to develop 7 GW by 2030) was access to transmission infrastructure and adequate network capacity.

Similarly, Spanish utility company, Iberdrola (IBE SM), as part of its November 2023 submission towards the parliamentary inquiry into the feasibility of transmission infrastructure for renewable energy projects, flagged that “transmission infrastructure needs to be built now if we are to significantly increase the connection of additional generation required to replace the coal-fired generators”. Without adequate investment, this could “lead to blackouts, reliability issues and increased energy bill prices”. Interestingly, in recent conversations with renewable developers across Europe, it was flagged that the pace of transmission investment in Australia was seeing them re-think strategic allocations to renewables in the country until there’s greater certainty in connection.

The substantial investment requirement in transmission infrastructure is not a new phenomenon, nor is it unique to Australia, albeit we do seem to be lagging much of Europe and the USA at the moment. In its World Energy Outlook 2022, the International Energy Agency (IEA) estimated that, globally, 1.6 million km of transmission lines will be constructed by 2030 and a further 4 million km by 2050. Per the IEA’s “Electricity Grids and Secure Energy Transitions” (October 2023), the required investment in transmission infrastructure to 2030 is forecast at over US$600 billion per year. This investment in transmission infrastructure is essential to connect at least 3,000 GW of renewable power projects waiting in grid connection queues.

Across the collective energy sector, the IEA estimates that to reach net zero emissions by 2050 annual clean energy investment worldwide will need to more than triple by 2030, to around US$4 trillion. We see several listed infrastructure operators looking to capitalise on the unprecedented transmission infrastructure investment requirement, distribution network investment, and renewable operators with deep development pipelines. At 4D, we favour those countries and companies capitalising on the vast and very attractive network investment opportunities, but within a framework that facilitates timely investment. These include National Grid, Iberdrola, Enel in Europe, multiple integrated utilities in the US such as American Electric, Sempra and Edison, and utility players across Brazil such as TAESA.

Source: Emkay Research

Conclusion

Efficient and timely investment in transmission networks is essential for unlocking new renewable capacity, and is a key enabler of other areas of the energy transition and the ultimate electrification of Australia. A concerted effort from government, regulatory bodies, private investors and communities towards developing transmission infrastructure is required, as the cost of inaction will compromise achieving more affordable, reliable, and cleaner energy for all Australians.

At 4D, we’re following this closely. Without viable investment timelines, global renewable operators in Australia may look at risk and utility (renewable and network) opportunities elsewhere, which looks much more attractive.

To view full article with Appendix, download it below.

[1] https://infrastructurepipeline.org/project/humelink

The content contained in this article represents the opinions of the authors. The authors may hold either long or short positions in securities of various companies discussed in the article. This commentary in no way constitutes a solicitation of business or investment advice. It is intended solely as an avenue for the authors to express their personal views on investing and for the entertainment of the reader.