Sustainability and associated ESG issues are becoming increasingly important in global investment analysis.

At 4D Infrastructure, ESG assessments have always and will continue to play a key role in our investment process. We have a unique integrated process for investment, whereby country risk analysis is combined with individual stock analysis in a single analytical cycle. Put simply, a stock cannot find its way into our portfolio unless we are also happy with its country of origin as defined by its listing locality and/or primary sources of income. Because of this two-step integrated process, we complete ESG reviews at both a country and individual stock level. ESG analysis is conducted in house, with Institutional Shareholder Services Inc (ISS) providing an external data feed into our analysis.

In this article, Sarah Shaw (Global Portfolio Manager & Chief Investment Officer) looks at: (1) the current state of play with Environmental, Social and Governance (ESG) issues around the world; (2) corporate controversies that defined 2019; and (3) our approach to incorporating ESG factors into our investment process, demonstrating why ESG is so important to 4D.

(1) The current state of play with ESG around the world

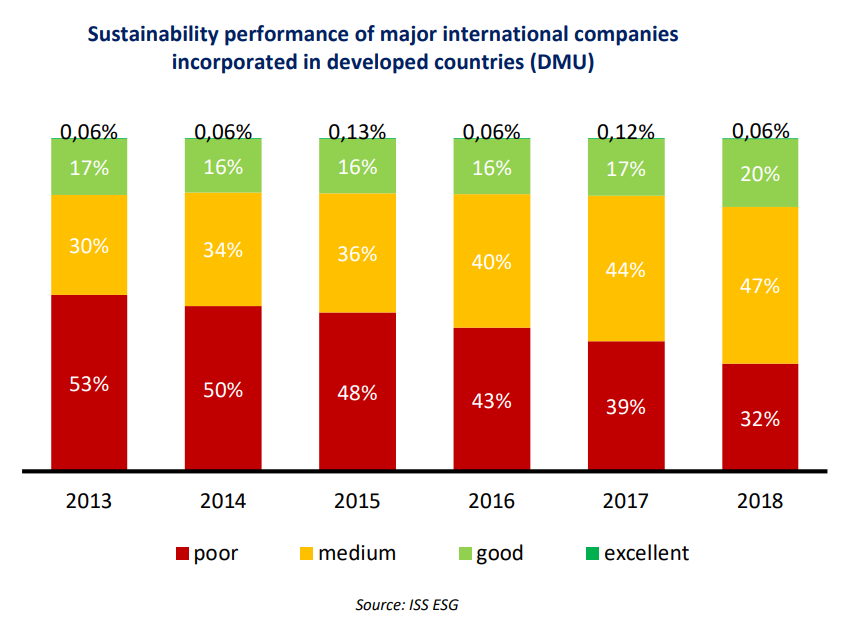

ESG continues to grow in importance across global capital markets as sustainable investing gains increasing favour. Institutional Shareholder Services Inc’s (ISS) ‘ESG Review 2019: The State of Play of Corporate Responsibility’ identifies that the share of companies with ‘good’ or ‘excellent’ ESG performance saw an unprecedented increase in 2018 reaching an all-time high of 20.4%, up from just over 17% in the previous year (see chart below). Together with ‘medium’ assessed companies, the group rated with ‘better-than-poor’ performance exceeds 67.5%. Similar patterns can be observed among companies incorporated in emerging markets (EM), but on a lower level.

ISS identifies the drivers of this increase in accountability as varied, but regulation features prominently:

- in March 2018, the European Union’s (EU) Action Plan defined 10 actions on sustainable finance;

- in May 2018, the European commission (EC) published four legislative proposals relating to taxonomy, fiduciary duties, and disclosure (ESG integration), low-carbon benchmarks, and ESG as part of financial advice (amendments to MIFID and IDD directives); and

- a Technical Export Group on sustainable finance (TEG) was also set up.

Voluntary initiatives are also important drivers of change. The Task Force on Climate-related Financial Disclosures (TFCD) and the Sustainability Accounting Standards Board (SASB) reporting standards continue to grow in importance.

The Paris Agreement: driving cultural change

The Paris Agreement is an agreement within the United Nations Framework Convention on Climate Change (UNFCCC) dealing with greenhouse-gas-emissions mitigation, adaptation and finance, signed in 2016. The language was negotiated by representatives of 196 states and adopted by consensus on 12 December 2015.

The Paris Agreement’s central aim is to strengthen the global response to the threat of climate change by keeping a global temperature rise this century well below 2 degrees Celsius above pre-industrial levels; and to pursue efforts to limit the temperature increase even further to 1.5 degrees Celsius. Additionally, the agreement aims to increase the ability of countries to deal with the impacts of climate change, and to making finance flows consistent with a low GHG emissions and climate-resilient pathway.

The Paris Agreement requires all parties to put forward their best efforts through ‘nationally determined contributions’ and to strengthen these efforts in the years ahead. The Paris Agreement opened for signature on 22 April 2016 and entered into force on 4 November 2016. Since then 186 Parties (of 196 to the Convention) have ratified the agreement. [1]

New disclosure to be required from fund managers on ESG

Common reporting requirements are being developed under the Paris Agreement, and are to be available for review by the end of 2020. While the formats have yet to be finalised, set out below are illustrative examples of what potential reports may look like (as developed by ISS) together with comments on recent develoments in GRESB – the investor-driven global ESG benchmark for the infrastructure sector.

-

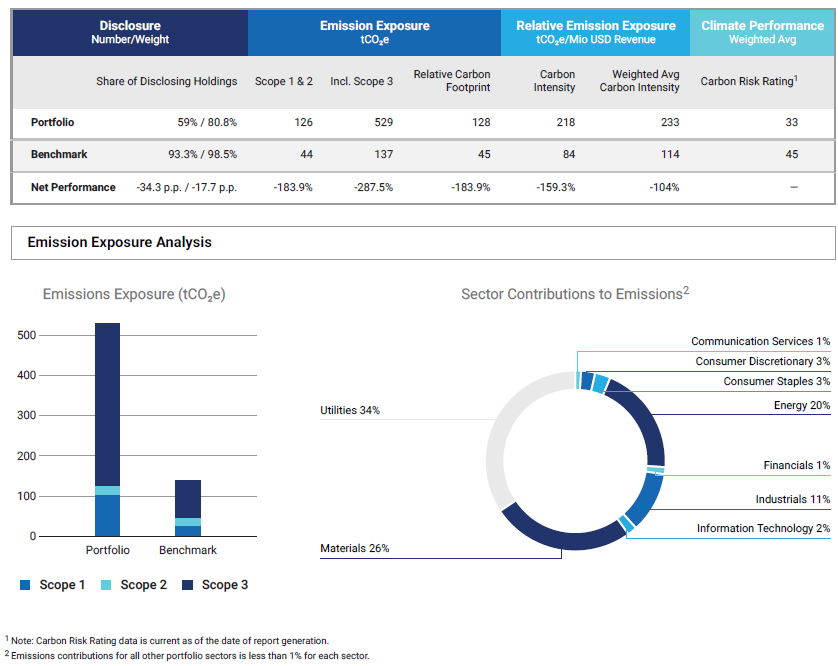

Portfolio overview versus a benchmark

This report provides a comparison of a fund manager’s portfolio on emissions grounds against a benchmark.

Source: ISS ESG

-

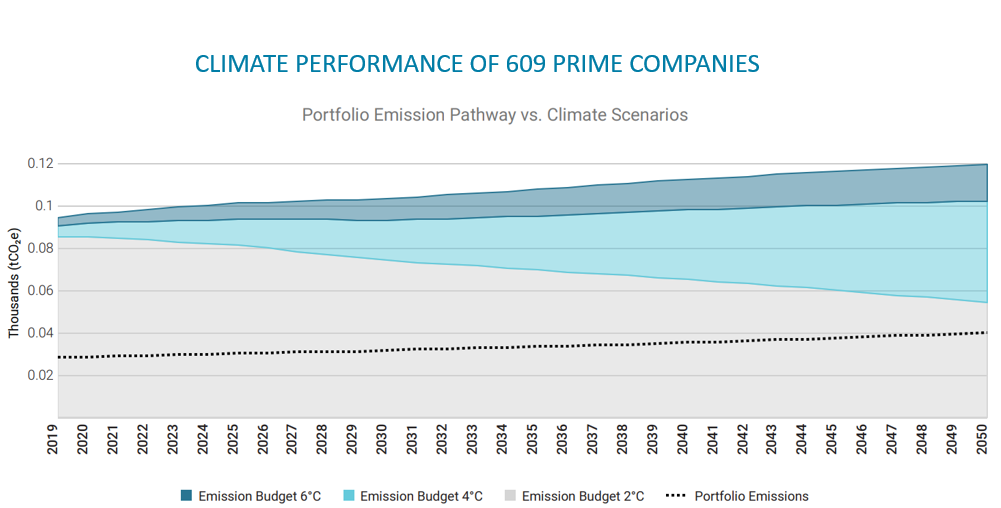

Ongoing portfolio compliance against the 2 degree target

This ISS report looks at a portfolio’s compliance with the 2 degree target. In the example below, it shows that a portfolio of 609 companies, rated as ‘Prime’ [2] by ISS on ESG grounds, would comply with the 2 degree target out to 2050.

Source: ISS ESG

-

New GRESB/GLIO infrastructure public disclosure dataset

In 2019, GRESB and GLIO released a new Public Disclosure dataset measuring the level of material ESG disclosure by the listed infrastructure sector. The dataset’s initial coverage will enable investors to evaluate ESG transparency levels across the entire global listed infrastructure universe.

The GRESB/GLIO dataset collection is unique in that GRESB originally gathers the information and subsequently provides each company with the opportunity to review and amend/correct the data.

(2) Corporate controversies that defined 2019

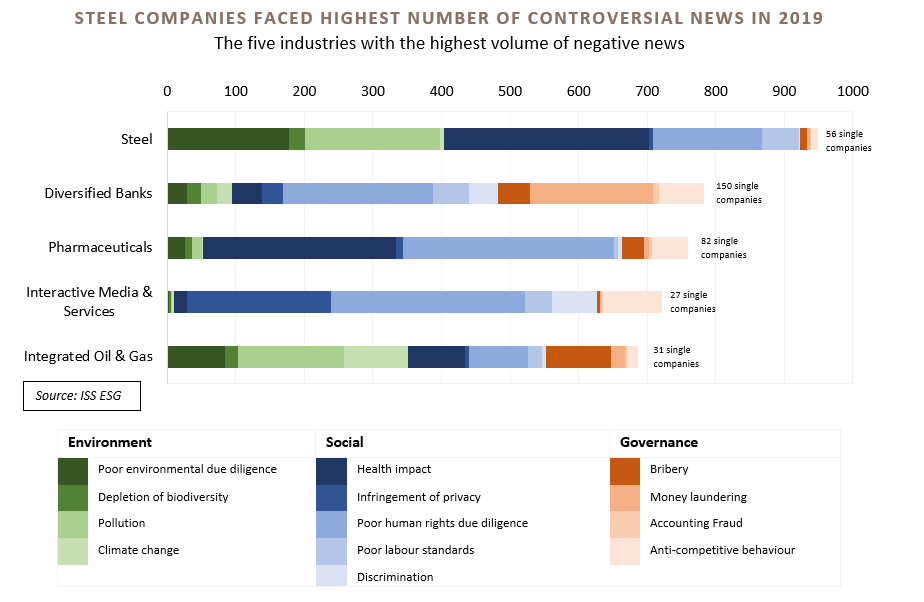

In January 2020, ISS published a paper ‘Corporate controversies that defined 2019’ in which they identify the five most exposed industries to ESG controversies.

Mining accidents in Brazil and the ongoing opioid crisis in the United States were two of the most serious controversies during 2019. These resulted in a high density of negative news revolving around steel and pharmaceutical companies.

The table below ranks industries according to the number of negative news items they generated during 2019, broken down according to different ESG categories. The human and environmental costs associated with dam collapses in Brazil contributed significantly to the high number of negative news items for the steel industry, which ranked as the most controversial industry.

The banking sector faced heavy media scrutiny during 2019 as several European banks were linked to money laundering schemes. The so-called Troika Laundromat scandal was among the most prominent cases, one which implicated several banks that are alleged to have laundered billions of dollars out of Russia. The case, which came to light in March following a data leak of 1.3 billion banking transactions, is estimated to have been responsible for funnelling US$4.6 billion into Europe and the US from questionable Russian sources. In Australia the Banking Royal Commission attracted a high degree of publicity. Separately, the banks are also being challenged by stakeholders for neglecting to assess their exposure to human rights violations and environmental damage through their investments.

Importantly, what you don’t see amongst the largest controversies for 2019 are infrastructure names or sub sectors within this space, despite the ongoing spotlight on climate change.

(3) 4D’s approach to ESG: integrated at the country and stock level

4D’s investment process involves an integrated macro (Country Reviews) and micro (Stock Reviews) approach.

-

Country Reviews: ESG assessment is an integral part of the process

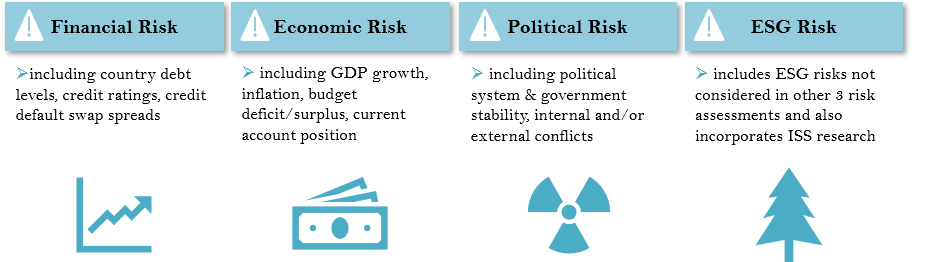

4D’s Country Review process involves assessing each country based on the four key sovereign risks identified below.

4D sovereign risk assessment

Source: 4D Infrastructure

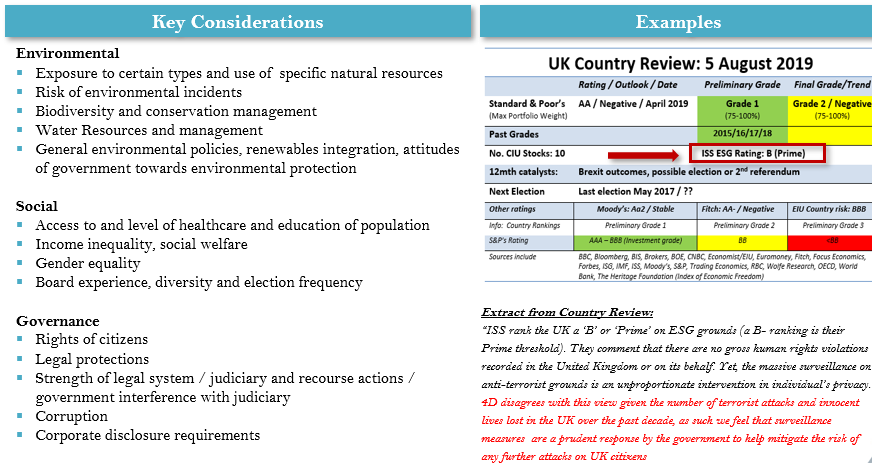

Within an ESG context, our key considerations are set out below. While it is the ‘E’ in ESG that currently attracts the most attention and publicity, as shown below in our Country Reviews we place equal importance on the ‘S’ and ‘G’. For example, Governance is key to our reviews as it goes to the quality and reliability of infrastructure concession contracts, and how strong the judicial system is in supporting the sanctity of those contracts. Similarly, levels of corruption are also important together with how well the judiciary is tackling the issue. For example, in Brazil the so called ‘Carwash’ corruption investigation has been ongoing and far reaching, but this is exactly what has helped us get more comfortable with that sovereign. No one is denying that a degree of corruption exists, but the judiciary has been persistent and diligent in its pursuit of wrongdoing at all levels of society.

We also subscribe to dedicated ESG research from ISS and incorporate that into our Country Review process. ISS ESG research conclusions are reflected via a ‘Prime’ or ‘non-Prime’ country rating. Note while this research is an important part of our process, we may not always agree with the ISS view. This is illustrated in the UK Country Review summary page shown below. The UK is rated ‘Prime’ by ISS, but we disagreed with some of their criticism.

4D ESG considerations at a country level

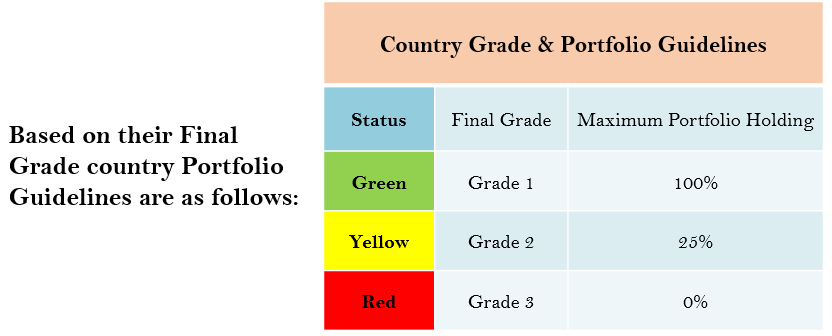

Based on our assessment of the four risks above, countries are then given a grade (1-3) and a traffic light status (green/yellow/red) as depicted in the chart below. The relative country grading determines the maximum portfolio exposure to stocks from that country grade.

Source: 4D Infrastructure

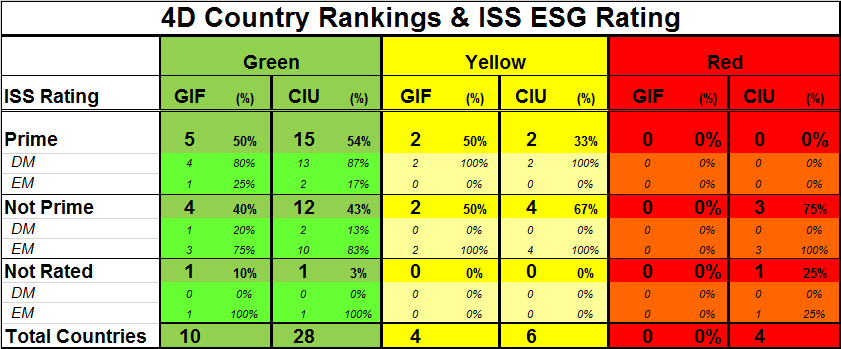

As shown in the table below, developed market (DM) countries ranked green by 4D have very strong ISS ESG rating profiles. Of DM countries with stocks in the 4D Global Infrastructure Fund (GIF), 80% are rated Prime by ISS, with that percentage increasing to 87% in our broader Core Investible Universe (CIU). Similar results occur for our yellow ranked DM countries where 100% of the Prime rated countries come from DMs.

However, symptomatic of EM countries generally not being as strong on ESG issues, only 25% of our green ranked EM countries are Prime according to ISS. This is not surprising, and we expect that as these countries evolve and migrate towards DM status their ESG ratings will improve accordingly.

Source: 4D Infrastructure

-

Stock Reviews: individual company ESG ratings

At 4D, we assess stock quality and value quite separately. Our company quality grading involves assessing each company based on the following broad criteria:

- Industry Structure;

- Asset Quality; and

- Management Performance

Our stock ESG assessment is part of the Management Performance assessment and an individual score is assigned to ESG factors as one of the four subcategories within the management assessment.

At a stock level we assess each stock based on the following ESG considerations. We also again employ independent ESG research from ISS to help determine our ESG company score.

4D ESG considerations at a stock level

Source: 4D Infrastructure

As is the case with our Country Reviews, we place great importance on the ‘S’ and ‘G’ as well as the ‘E’ in our Stock Reviews.The key considerations in these assessments are set out above. For example, under Governance we look closely at Board and management compensation structures to ensure an alignment with shareholders’ interests.

-

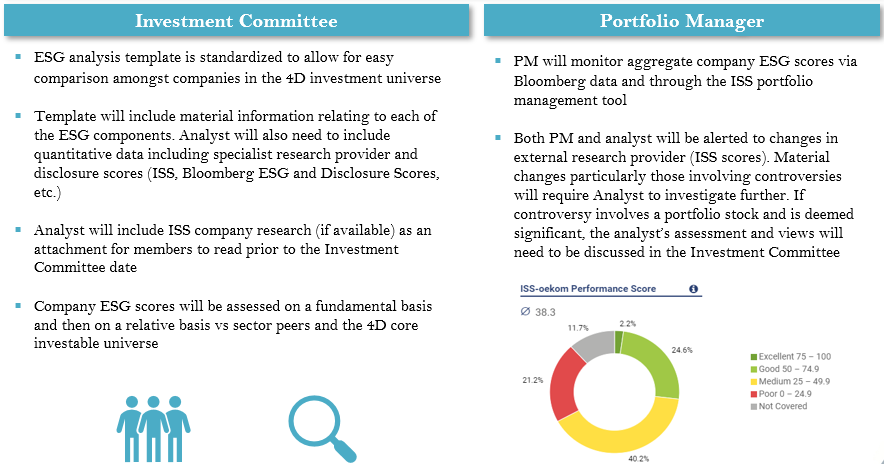

ESG at an Investment Committee/Portfolio Manager level

Finally, ESG is reviewed at the Investment Committee/Portfolio Manager level as summarised below.

4D ESG considerations at the porfolio construction and management phase

Source: 4D Infrastructure

Conclusion

ESG is growing in importance around the world as the next stage of implementation of the Paris Agreement approaches. At 4D we view each of ‘E’, ‘S’ and ‘G’ as a fundamental and critical investment factor that is only going to grow in importance in the future. Accordingly, we have integrated ESG assessment into all stages of our investment process and believe we are positioned to perform well in an increasingly ESG-focused investment environment.

Appendix: Case study in 4D ESG rankings

Source: 4D Infrastructure

[1] United Nations Framework Convention on Climate Change (UNFCCC). Source ISS ESG

[2] ISS uses a broad ‘Prime/Non-Prime’ approach to rating countries and companies in terms of ESG as well as individual entity gradings on an A-D basis.

The content contained in this article represents the opinions of the authors. The authors may hold either long or short positions in securities of various companies discussed in the article. This commentary in no way constitutes a solicitation of business or investment advice. It is intended solely as an avenue for the authors to express their personal views on investing and for the entertainment of the reader.