Over the past decade, investment allocations to private infrastructure have more than quadrupled from $129 billion to $582 billion [1]. This increased flow of funds into the asset class is expected to continue, driven by the continued inflow of capital into superannuation funds, pension funds, insurance companies and sovereign wealth funds; and their appetite for low volatility cashflow generating investments. Indeed, the allocation of funds to direct infrastructure is expected to exceed $1 trillion by 2023 [2].

An alternative to direct infrastructure investment is investing in infrastructure companies listed on global equity markets, either directly or through dedicated listed infrastructure managers. Listed infrastructure started to be recognised as its own asset class around 2005, with dedicated listed infrastructure funds like the 4D Global Infrastructure Fund becoming available to investors.

In this article, Senior Investment Analyst Peter Aquilina [3] and Global Portfolio Manager Sarah Shaw discuss why 4D Infrastructure believes direct and listed allocations complement each other in portfolio construction. They invest in the same type of assets – if not the exact same asset – while providing investors different ways to access the asset class depending on the investor’s appetite for asset concentration versus diversity, liquidity versus volatility, fees, execution risk, etc. With listed infrastructure allocations lagging direct infrastructure allocations, and with listed equity market valuations depressed, we believe a real opportunity has emerged in the listed infrastructure market.

1. Similarities and differences in infrastructure investment styles

Direct/unlisted infrastructure involves taking a direct stake(s) in infrastructure companies/assets (used interchangeably below for direct investment) which are not typically traded on public equity markets. The investor is often looking for control or management influence. These assets are revalued periodically at the discretion of the investor, or in line with accounting and regulatory standards. Direct infrastructure investors occasionally acquire holdings in companies that have securities traded on public markets. Usually this involves acquiring large stakes, often with positive or negative control provisions (e.g. the listed Vienna Airport is partly owned by IFM, a major player in the direct space).

Listed infrastructure involves investing in infrastructure companies which are traded on public equity markets. Relatively smaller shareholdings are taken in publicly traded shares, generally with no management control associated. As these companies are publicly traded, they are repriced daily by equity markets and can be bought and sold in a timely manner (providing liquidity).

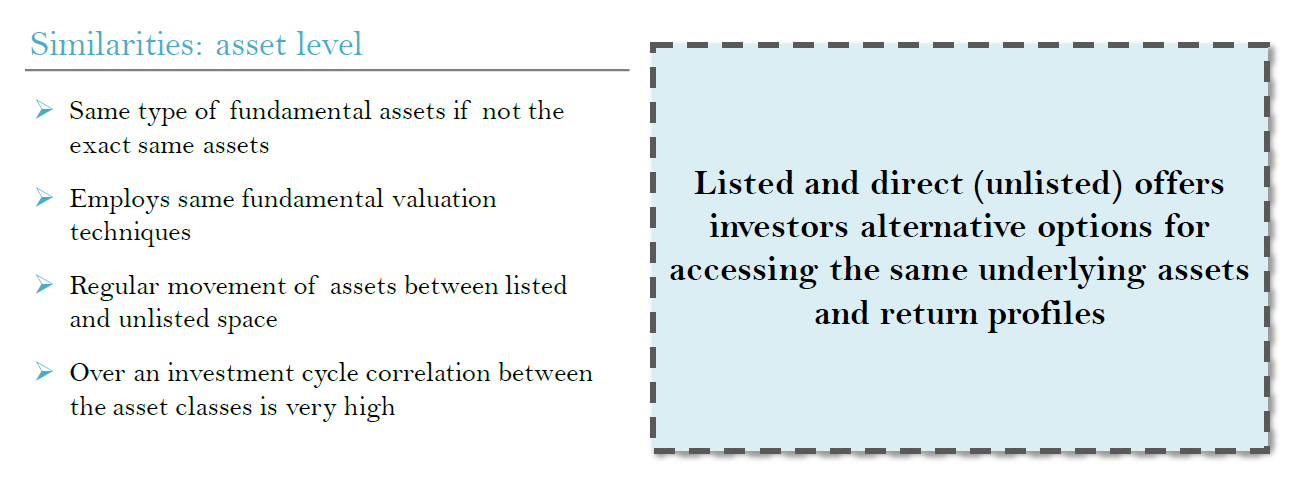

Similarities

Direct and listed infrastructure investors invest in fundamentally the same type of, if not the exact same, underlying assets. Their definition of infrastructure is the same or very similar, and they are both looking for real assets with infrastructure characteristics that underpin long-term visible and resilient earnings. At 4D, we believe direct and listed infrastructure exposure simply offers investors different means of accessing the same asset class.

Figure 1: Listed vs unlisted similarities

- Same type of fundamental assets if not the exact same assets – direct and listed infrastructure investors fundamentally invest in the same type of assets, and in some cases exactly the same asset – for example, when direct managers take a large shareholding in listed companies (e.g. as noted above, Vienna Airport is partly owned by IFM) or where assets are partly owned by a listed entity and an unlisted investor (e.g. the 407 ETR toll road in Canada is owned by both Canadian pension funds and the Spanish listed operator Ferrovial).

- Employ the same fundamental valuation techniques – direct infrastructure investors represent long-term investors, who are typically focused on cashflow generation and growth. This focus on cash is why direct investors generally utilise fundamental discounted cashflow (DCF) valuation techniques. Dedicated listed infrastructure investors also typically represent long-term investors, who are focused on the same cashflow generation of listed companies. The majority of these, including 4D, also adopt long-term DCF valuation techniques, supported by peer valuation metric analysis.

- Regular movement between the listed and unlisted markets – there have been a number of examples where private investors have acquired listed companies (some will be flagged later in this article) as well as where privately held assets have found their way into a listed operator’s hands. As outlined earlier, there are also a number of examples where direct infrastructure managers hold significant shareholdings in companies that are available on listed markets.

- Over a complete investment cycle there is a high correlation between the performance of the investment styles – as illustrated in Figure 3.

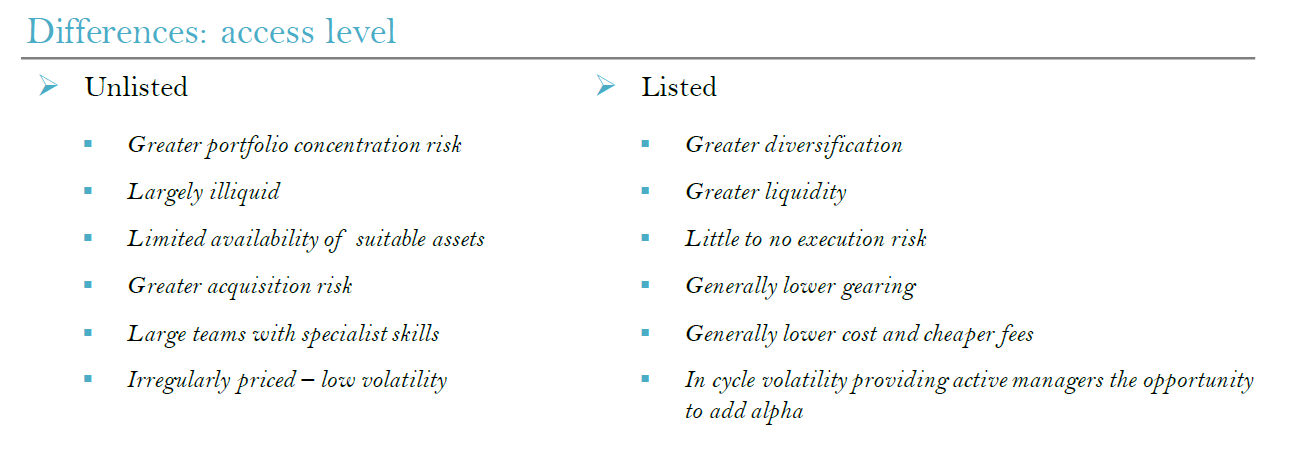

Differences

Even though the underlying companies/assets of both direct and listed infrastructure investments are fundamentally the same, how investors access the asset class can differ significantly between the two investment styles. These key differences are summarised below:

Figure 2: Listed vs unlisted differences

- Concentration vs diversification – direct investors generally take large stakes in infrastructure assets which often include ongoing management/control obligations. This means that often the amount of different investments that can be held in a portfolio is limited. Most co-mingled direct managed funds include 10-15 different investments. Listed infrastructure funds, by contrast, offer much greater geographic and asset diversity. As an example, we at 4D build a portfolio of 30-60 equity investments. The individual listed companies we hold will often own a portfolio of assets themselves (e.g. Transurban owns or has holdings in 24 individual toll road concessions).

- Liquidity – short term liquidity is difficult to achieve for direct infrastructure investments as it generally requires investors to sell all or a portion of holdings in assets, which can take significant time and cost in advisory services. If liquidity needs are urgent this process can lead to distressed sale processes, which results in value destruction. Conversely, listed investors can liquidate positions relatively easily, particularly if the investment process involves liquidity screens at the outset. This access to liquidity becomes particularly important if there is a call on capital, or an asset fundamentally changes and an investor seeks a fast exit from a market (e.g. owning utility assets in the UK in 2019 during the Jeremy Corbyn utility nationalisation campaign – direct investors tended to weather the risk, while listed investors could exit until the situation was clarified).

- Availability of suitable assets – due to the illiquid nature of direct investments, investors typically target mature assets with strong cashflow generation from the outset of the investment. Listed investments include mature/operational companies as well as those involved in the development of new greenfield assets.

- Higher gearing – direct investors are generally more comfortable utilising higher leverage than their listed counterparts will tolerate. Leverage is also used by listed operators, but market pressures (particularly post the GFC) have seen management teams cap leverage at much lower levels than the direct market. This use of leverage can see direct investors achieving suitable equity returns based on higher investment valuations.

- Acquisition risk, and team size – the high levels of competition for suitable assets in the unlisted market means there is a risk that direct investors spend considerable time and money on unsuccessful acquisition processes. These investors also require large teams to undertake lengthy and complicated due diligence processes. Listed investors face little to no execution risk in acquiring shareholdings, and can operate with relatively smaller teams. They are also limited to publicly disclosed data so the due diligence, while still rigorous, is less detailed compared to direct investors.

- Fees and costs – as a result of smaller teams and given investors can access listed equity markets directly, listed infrastructure strategies generally offer lower investment fees than their direct counterparts. Fees for listed strategies offered to institutional clients range from 0.35% to 0.9% per annum, with a median of 0.6%[4]. Direct counterparts usually charge fees in excess of 1% per annum. In addition, the large costs associated with undertaking due diligence of potential targets can be passed on to investors, usually charged to funds, which is why execution risk for direct infrastructure investment can be so costly.

- Volatility – the low volatility of direct infrastructure investments is one of the most desirable attributes of the asset class to many investors. This is partly due to the underlying defensive/stable qualities of the underlying assets through economic cycles, and is supported by irregular valuation processes (usually quarterly) which are undertaken by third party valuers using financial models provided by the manager. Listed assets have the same stable characteristics, but are marked-to-market daily by equity markets, leading to greater in-cycle volatility. We believe this is a significant opportunity for specialist listed managers to use the market mispricing to add alpha. Over time the correlation of returns is quite high, so using volatility can be key to improved returns within the listed space.

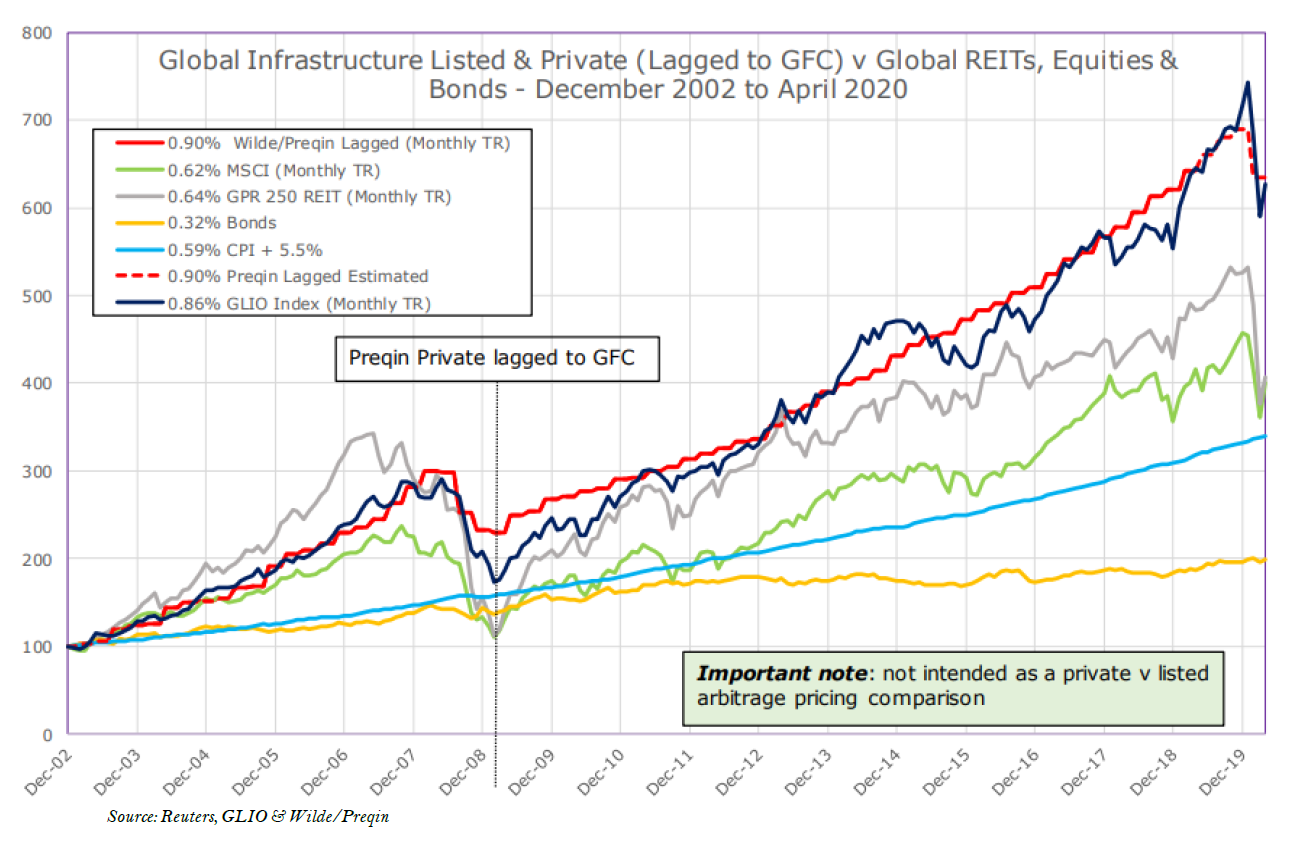

2. Return correlations between investment styles should be high

The performance correlations between direct and listed investments over an investment cycle has historically been high. Using available market indices as valuation proxies for listed and direct infrastructure markets, the correlation between the investment styles can be observed in Figure 3, with the direct infrastructure index (Wilde/Preqin – red line) highly correlated with the listed infrastructure index (GLIO – black line) over the long term. Figure 3 also shows that even though listed and unlisted market performances are closely aligned over time, short-term mispricing in listed infrastructure markets provides opportunities for active managers like 4D to deliver alpha.

Figure 3: Listed vs unlisted asset performance over time

3. Is there a valuation dislocation between direct and listed infrastructure investments?

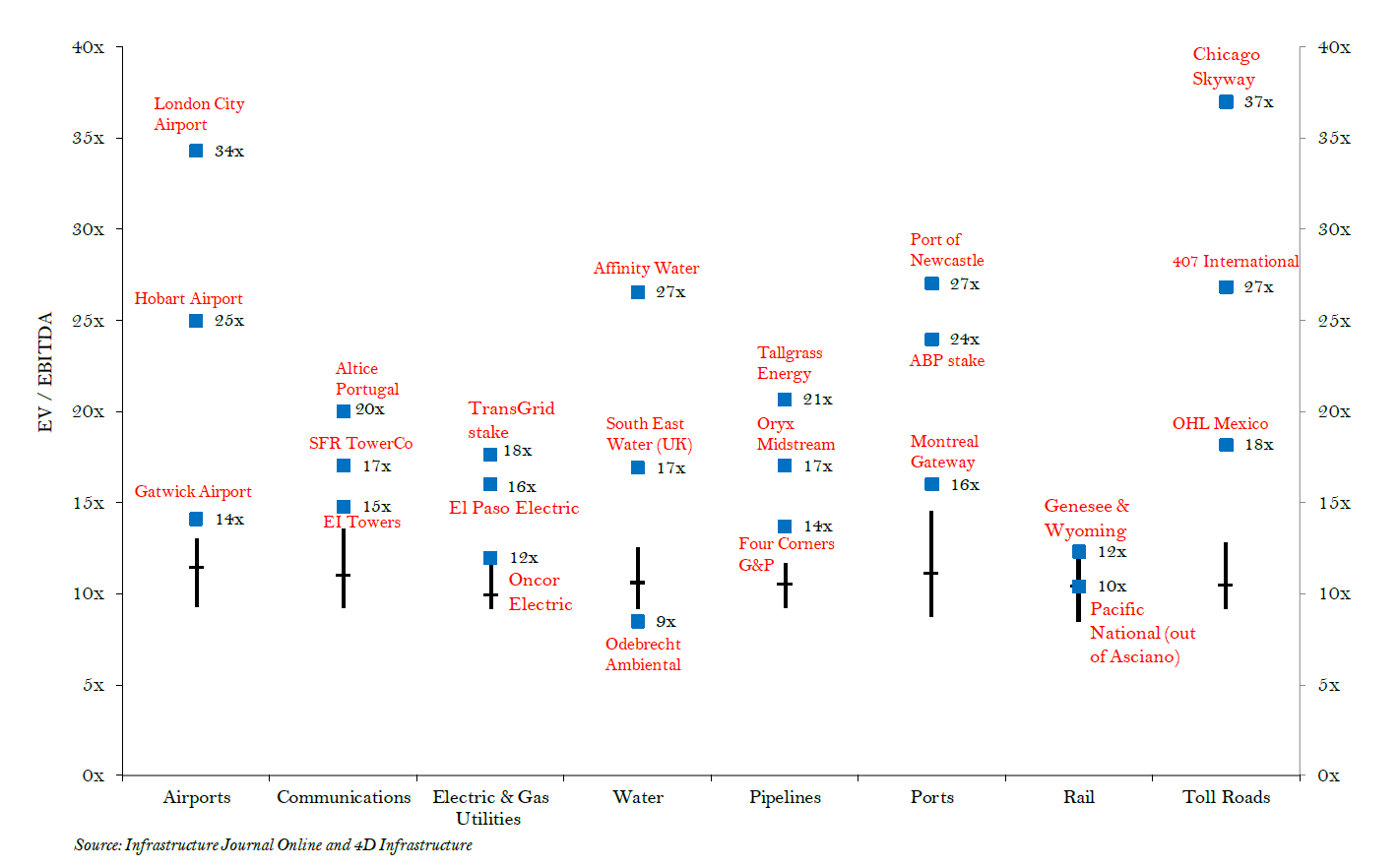

Anecdotally it feels that the intense competition for private infrastructure acquisitions over the past 10-15 years has resulted in execution valuation metrics in excess of that of trading peers. We have looked to test if there is any validity to this by analysing EV/EBITDA transaction multiples against the average of trading peers across infrastructure sub sectors. In Figure 4 we have plotted the average implied EV/EBITDA multiples by sector over the past five years for listed infrastructure by sector, against the same implied multiple for select direct investment transactions across sectors over the same timeframe. Our key takeaway from this analysis is that there appears to have been a clear valuation dislocation between listed trading multiples and direct infrastructure transactions, across all infrastructure sectors over the analysed period.

Figure 4: Listed vs unlisted valuation multiples: 2015 - 2020

We then looked to analyse the relative valuations between listed infrastructure stocks and market transactions within specific sectors. We compared the average trading range within the airport (user pay) and water (utility) sectors over the past 10 years with direct investment transaction multiples within those sectors. Figure 5 confirms our view that the vast majority of private transactions occur at multiples towards the top end or above the range of listed valuation multiples.

Figure 5: Airport and water transaction multiples: 2010-2020

4. Why is the direct infrastructure market paying more for assets than listed?

Based on our conclusion that direct infrastructure investments have been transacting at significant premiums to their listed counterparts, the key question is: why does this dislocation exist?

- Scarcity of operational assets (brownfield and cashflow generating) – as outlined above, the illiquid nature of direct infrastructure investment, coupled with a more concentrated asset portfolio, means these investors target assets with immediate cashflow generation capability. Greenfield/development projects represent a huge growth opportunity for the infrastructure sector. However, these assets don’t generate immediate cashflow, so are less attractive to the direct investor.

- Continued massive flows of investor capital looking for deals – investors are continually drawn to the low volatility, cash yielding characteristics of direct infrastructure which sees a growing queue of capital looking for a deal. Direct investors need to put this capital to work, so could be willing to accept a lower return or utilise higher gearing in structuring a deal in order to generate returns for this cash queue.

- Lower return thresholds in low interest rate environments – low global interest rates have lowered required returns for all investors (both direct and listed), facilitating higher multiples being paid to acquire assets. For listed operators, while return benchmarks have also lowered, they remain higher than direct return thresholds due to the requirements of their listed investor base (market equity risk premiums) and as such the lower cost of capital and higher valuations paid by direct infrastructure investors may be somewhat justified.

- Paying a premium for management control or influence – it’s not clear if this adds value to the investment, but it certainly appears that direct investors are willing to pay for it. Due diligence of management teams is important for listed investors, whereas direct investors may look to install their own teams or influence management from Board positions.

- Ability to gear up an unlisted asset further – post acquisition, direct investors have utilised higher gearing levels to improve equity returns (as mentioned they are more tolerant of higher gearing than listed investors). While listed operators have historically utilised the same structuring, many came un-stuck in the GFC as a result of equity market falls (e.g. Babcock and Brown) and the practice is now less aggressively utilised.

- Possibility that direct infrastructure investors and managers have a better appreciation of the defensive qualities of infrastructure assets than listed market investors – there are still very few listed infrastructure companies with share registries that are majority comprised of industry specific listed infrastructure managers. Instead, registries are dominated by a broader, generalist equity investor pool including infrastructure specialists. In contrast, direct infrastructure investors are specialists in the asset class, which arguably gives them greater confidence in the premium valuations paid compared to generalist equity investor valuations. We believe this represents a real opportunity for dedicated listed infrastructure managers to add significant alpha both on a relative and absolute basis.

5. COVID-19 compounding the valuation gap

The COVID-19 pandemic pushed the international economy into recession and cut a swathe through global equity markets. From 21 February through to the end of March 2020, the US S&P 500 equity index was down 23.2% and the MSCI World index was down 23.1%.

Listed infrastructure was certainly not immune to this value erosion, with the recognised infrastructure indices down 18-32% over the same period. This price volatility could continue for a while yet, until it becomes clearer that health authorities around the world are getting on top of the outbreak. However, it is important to remember that infrastructure is a very long duration asset with a 5-10+ year investment horizon. Once we move past the worst impacts of the virus and the world’s economy returns to a more stable environment, all forms of infrastructure will be integral to the economic recovery and returning society to ‘situation normal’. There is no global growth recovery without roads, railways, pipelines, power transmission networks, communication infrastructure, ports and airports [5].

Unlisted infrastructure players have also recently assessed the impact of COVID-19 and adjusted their asset valuations down, but by a much smaller percentage than the listed market falls. For example, the media has reported:

- Australia’s Unisuper has cut the value of its holdings in unlisted infrastructure by 6% (this investment portfolio includes the Brisbane and Adelaide airports); and

- AustralianSuper, the nation's largest super fund, has cut the value of the unlisted assets on its books by 7.5% (which includes infrastructure).

We believe the real fundamental valuation impact of the COVID-19 pandemic on these assets is more closely aligned with the unlisted valuation shift. There is clearly a significant near-term earnings impact for some of the infrastructure sectors, namely airports, toll roads and other User Pay sectors that justifies a cut to valuations. However, the longer-term fundamentals of the stocks/sector suggest the listed market has completely oversold these assets on what we consider to be an event-driven earnings shock. We believe this will prove to be a buying opportunity for these assets if investors can look through the near-term earnings hit.

Using an airport as an example, short-term investors valuing an airport on a one-year price-to-earnings (PE) multiple will be slashing their target prices as the one-year earnings outlook is dramatically cut as a result of the COVID-19 driven grounding of flights. However, infrastructure is a very long duration asset class, which should be valued with a recognition of its implicit longer-term cashflow generation. As discussed, 4D values these assets using a long-term DCF methodology to determine intrinsic fair value. While a one-year earnings (cash flow) hit will impact this valuation, with asset lives of 50+ years a one-year hit does not justify the significant drop in value that equity markets have attributed. We believe that while COVID-19 is causing significant disruption and earnings impacts globally, it will resolve and life will return to a new normal. We also believe the long-term structural opportunity for airports remains intact and very strong – traffic will recover and with it, earnings and cashflow.

We believe this widening value disconnect between listed and unlisted valuations represents a significant opportunity for listed infrastructure investors.

6. The competition for assets could prove to be a sector overhang

Infrastructure as an asset class is increasingly on the radar of investors and their advisers. Its defensive attributes, coupled with a significant global growth opportunity as a result of decades of underspend and the changing dynamics of the global population, create an attractive long-term thematic for the sector which is intact despite the near-term concerns of COVID-19. Despite the huge investment need, competition for operational assets remains strong and in the near term could prove to be a sector overhang, which is something we are monitoring closely.

As outlined at the start of this paper, the capital flow from institutional investors to direct infrastructure is expected to surpass $1 trillion by 2023. The 4D defined listed infrastructure universe by market capitalisation is also growing rapidly, from <$2trn in 2006 to ~$4trn at the end of 2019, as more and more specialised operators look to capitalise on the asset fundamentals and build for the future in supportive low interest rate environments like the present. Examples of infrastructure managers which have raised significant capital over the past 12 months include:

- Ardian announced it raised US$19 billion blind pool and co-investment in June 2020

- Brookfield announced it raised US$20 billion in February 2020

- Blackstone announced it raised US$14 billion in July 2019

The amount of capital competing to be invested may come with an increase in investor risk, and potentially increasing activity within and between the direct and listed investment pools. This could result in sub-optimal outcomes for investors, namely:

1. Capital may get stuck in long commitment queues as managers can’t put it to work (estimated by the Global Listed Infrastructure Organisation (GLIO) at +$100 billion);

2. Management teams look to invest in opportunities outside their core business strategy. This is often to drive growth to achieve financial remuneration incentive targets, when core business growth drivers are more difficult to come by;

3. Management teams/managers starting to look further up the risk/return spectrum for acquisition targets due to high competition for core infrastructure investments:

a) “Core +” and “Core ++” assets can generate immediate cashflow but expose investors to greater and different risks than they would expect from traditional infrastructure (examples include bus networks; service stations; waste management (garbage trucks and dumps); data centres; land titles businesses; and student accommodation)

b) New builds which carry greenfield risk (construction and ramp up risk) with a lag to cash flows; and

We are very conscious of the increased competitive dynamic and see it as a core risk to the asset class, particularly given the ease of access to plentiful and cheap capital. As such we assess each stock in our universe on strategy and capital discipline to ensure our investors are gaining exposure to what we consider to be core infrastructure characteristics acquired at valuations that earn a viable return over the asset life.

Conclusion

Both direct and listed infrastructure investment styles offer benefits to investors in their defensive, predictable earnings through economic cycles, low volatility, stable cashflow generation, and long-term growth. They both invest in fundamentally the same assets (if not exactly the same assets). Direct infrastructure investment offers investors lower volatility and greater management control, which is very attractive to some institutional investors like superannuation/pension funds and sovereign wealth funds. However, this lower volatility and management influence comes with illiquidity, higher gearing levels, higher costs/fees and more concentration. By contrast, listed exposure provides investors liquidity, increased asset and geographic diversity, and lower fees – but with significantly higher in-cycle volatility.

The infrastructure asset class continues to experience large capital inflows from institutional and retail investors alike. This capital flow has increased competition for suitable investment targets in both direct and listed markets. Investors need to be wary of perverse outcomes as managers of capital struggle to find suitable investment opportunities that fit the investment criteria of infrastructure. These include capital being held up in long commitment queues; managers looking for investment/growth outside the core definition of infrastructure; and assets transitioning between listed and private markets to the detriment of one investor type.

We at 4D believe that both direct and listed infrastructure offer compelling investment attributes that make them both suitable as a long-term allocation for investors. We also believe that a balance between direct and listed exposure is optimal in portfolio construction. This provides investors with the same infrastructure exposure, but with a balanced mix of complementary style-specific qualities.

In the current environment, with listed infrastructure prices offering very attractive value as a result of the depressed equity market conditions, we believe timing supports allocations to listed infrastructure markets. In this market, specialised managers like 4D have the opportunity to generate alpha returns as a result of the market dislocation.

Download a copy of the article here.

Appendix

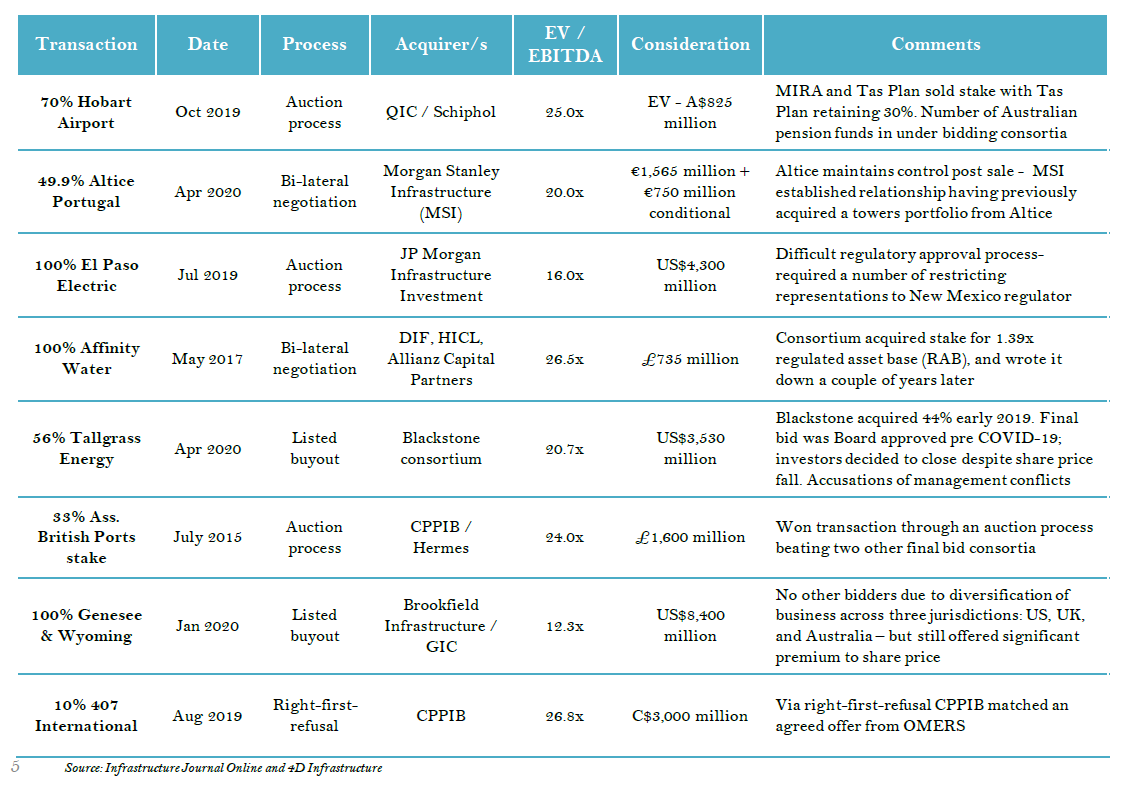

Below is more detail on a selection of the direct infrastructure transactions identified in Figure 4.

[1] Preqin 2020 Global Infrastructure Report – In Focus: How Big Will Infrastructure Get?

[2] Preqin 2020 Global Infrastructure Report – In Focus: How Big Will Infrastructure Get?