This is the abridged version of the article, which can be read in full here.

Several of the main risks going into 2026 carry over from 2025: heightened policy uncertainty, bond market sensitivity to governments' fiscal situations, the impact of tariffs on economies and the rewiring of global supply chains and trade networks. Geopolitical risk remains elevated, notably the US midterm elections, French & UK domestic politics, conflicts in Ukraine and the Middle East and increasing tensions with allied partners over Greenland.

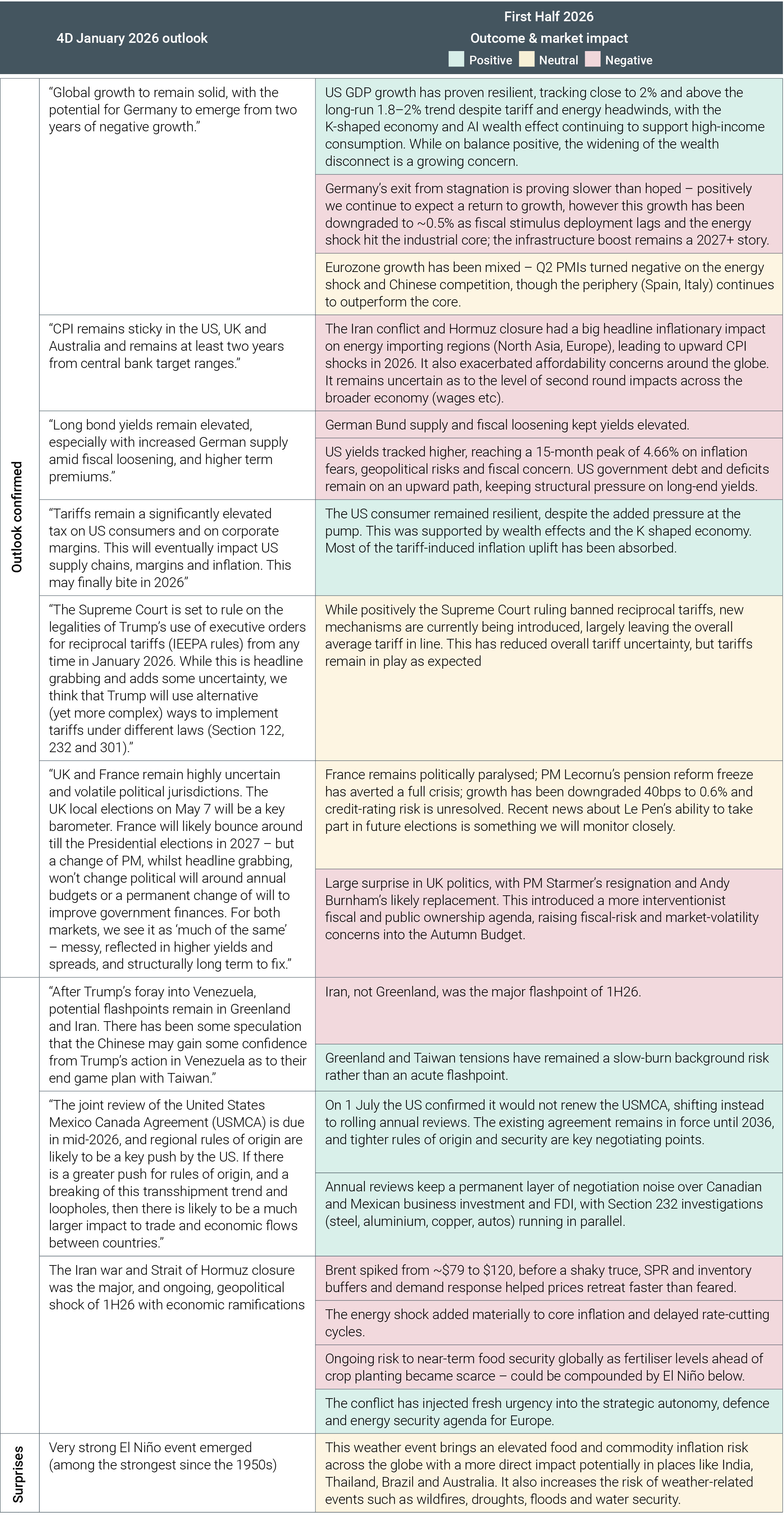

(4D January 2026 Outlook)

The first half of 2026 witnessed its fair share of shocks and surprises:

- A fresh Middle East conflict and a Strait of Hormuz closure, briefly cutting global oil supply and reviving energy security fears before a shaky June truce began to stem the damage.

- Inflation has been stickier, not softer – the energy shock added to already-elevated core CPI in the US and Europe, pushing price pressures further from central bank targets.

- A sharp turn in the interest rate narrative – from 'flat to cut' across the board to a genuine two-way debate, with several central banks already raising policy rates and others expected to do so before year end.

- Political upheaval in the UK (Starmer's resignation and Andy Burnham's ascent) and continued paralysis in France, keeping European political risk elevated.

- In the lead up to the November US midterms, consensus is building around a divided Congress.

- China's growth is holding up on export strength, even as domestic demand and the property sector remain weak.

- The continued reordering of global supply chains and trade networks around security of supply rather than efficiency (exacerbated by the energy shock).

Despite all of this, risk assets have proven relatively resilient, supported by strong corporate earnings, and an AI investment cycle that continues to run ahead of expectations. By contrast, despite very strong fundamentals and a good start to the year, real assets have lagged broader markets. We believe this is a buying opportunity for select infrastructure names.

What's happened so far in 2026

We review below the main parts of our 2026 Outlook that were confirmed in the first half, and their impact (positive, negative or neutral), as well as several surprises that arose. Our assessment below is purely on the economic impact, while we discuss whether our infrastructure names are detrimentally impacted or can mitigate or capitalise on these themes later on.

We expand on a few of these developments with our favourite charts in the full version of this update (link below), across the following themes –

- Theme 1 – GDP estimates down and CPI up

- Theme 2 - Higher inflation but for how long?

- Theme 3 - Changing interest rate outlook

- Theme 4 – Heightened geopolitical calendar

- Theme 5 – USMCA uncertainty

- Theme 6 - China's dual track

- Theme 7 – Energy and resilient supply chains

- Theme 8 – Revisiting AI; still the tailwind but power and debt are the restraints

What is next for 2H 2026?

At a global level, 4D believes the following will drive markets through year-end:

- Iran truce implementation – a genuine de-escalation, but Strait traffic has yet to normalise and inventory buffers are thinner than in February; if it holds, energy risk fades to a base effect and the rate debate can refocus on growth.

- The Fed and the credibility test – under new Chair Warsh we expect rates on hold rather than hikes, though pricing has swung 75bps; core inflation above 3.5% and real wages turning positive are the key triggers to watch.

- November 3 US midterms – consensus is building around a divided Congress; employment and affordability are the key swing metrics, and pre-election weakness could prompt stimulus.

- Political posturing in the UK, France and Brazil – expect populist rhetoric into elections, but most will be noise given fiscal constraints.

- El Niño into 2027 – one of the strongest events since the 1950s, layering food and agricultural inflation risk (India, Thailand, Brazil, Australia) on top of the energy shock, a key upside inflation tail for 2027.

What does this mean for infrastructure?

Infrastructure, interest rates and inflation are commonly linked, but often in an incomplete manner that does not reflect the full story of their correlation - perceived negative economic surprises can prove value accretive for infrastructure given certain assets' ability to mitigate or capitalise on economic shifts.

User Pay assets (toll roads, airports, ports, rail) are geared to GDP growth with embedded inflation protection while within Regulated Utilities the return model matters more than the label – real rate utilities (Europe, Brazil) pass inflation and rates through to earnings, while nominal rate utilities (historically the US) have been the true bond proxy. Active management across this spectrum is how we smooth the impact of persistent inflation and higher-for-longer rates.

Even the US – historically the bond proxy trade – is being reshaped by the AI investment super-cycle, with data-centre demand lifting utility earnings well above trend and decoupling share prices from the tight inverse correlation with the 10-year Treasury yield seen in 2022-23. We remain invested in select high-quality US names, while watching execution, financing and affordability risk.

Listed infrastructure offers truly global exposure across developed Asia, Europe, North America and emerging markets, letting an active manager capitalise on in-country cycles while diversifying away from any single macro outcome.

Below is how we see our main 2026 macro themes and risks playing out by region and sector, given 1H26 developments:

North America

The Iran war and the repricing of US rate expectations have pushed long bond yields higher for longer, weighing on utility valuations that lack a formulaic pass-through of inflation and rates. However, the AI-driven investment super-cycle continues to dominate the earnings story, with hyperscaler capex tracking toward US$1 trillion and boosting rate bases. The return spread to bonds may be compressed, but earnings growth remains elevated on stronger investment needs.

Affordability is becoming the key swing factor: rising residential bills from data-centre-driven grid investment are increasingly political heading into the November 3 midterms, and we favour states with lower relative bills, higher socioeconomic demographics and constructive regulators. Gas utilities offer some diversification, carrying less affordability overhang than electricity.

US rail remains most exposed to tariff-related disruption, though tighter trucking capacity from immigration enforcement is a structural tailwind for pricing. Midstream pipelines stay largely insulated near-term on multi-year contracted volumes, though Venezuela-related supply uncertainty and new LNG export terminals are reshaping the medium-term outlook for heavy crude flows. US towers is the sector least insulated – valuations squeezed by elevated yields and earnings by inflation, without an offsetting investment pipeline.

Europe

Europe benefits clearly from the shift toward real rate utility models as inflation stays higher and stickier, with the ECB's first hike since September 2023 validating formulaic, inflation-linked returns. Networks and grid operators with approved investment plans offer low-risk access to Europe's electrification and energy security capex super-cycle. The UK and Italy remain our preferred regulated network jurisdictions, supported by inflation protection, proactive regulators and, in the UK's case, strong RAB growth. We remain confident in UK water fundamentals but more cautious given near-term government intervention risk.

Despite the ongoing Middle East conflict, select European airports remain attractive. Our recent trip alleviated concerns around jet fuel supplies and confirmed buoyant summer demand. European airports also benefit from inflation pass-through into 2027; we favour Spain and Greece on relative growth and passenger mix.

Germany's fiscal build-out – the €500b infrastructure fund and defence-spending debt-brake exemption – remains supportive medium-term, though execution runs behind expectations, with public investment only reaching 3.6% of GDP by 2027 and near-term industrial weakness from the energy shock and Chinese competition. France's fiscal paralysis directly impacts concession names via higher taxes; despite value, we stay cautious on France-exposed names. We remain positive on Greece, driven by its economic renaissance, EU fiscal stimulus and strong government support for infrastructure investment, with Gek Terna one of our highest-conviction positions.

Asia

In China, strong export volumes have supported port throughput, but a weak property sector, elevated household savings and soft consumer confidence continue to weigh on domestic-demand-linked names. Our exposure is limited to names capitalising on the export/AI upside, while we remain cautious on those linked to domestic demand and property, such as gas utilities.

Elsewhere in Asia, exposure in Malaysia and India is capitalising on the long-duration growth thematics supporting the infrastructure investment super-cycle, largely insulated from the current macro outlook through regulation and policy support.

Latin America

Brazil remains a core overweight, even with rate cut expectations pushed into 2027. Every infrastructure asset carries an explicit annual inflation hedge, many compounding over the asset life – meaning the current backdrop of GDP upgrades and elevated inflation can be value accretive despite higher rates. We expect volatility ahead of the October 2026 election, but the market has largely priced in a Lula victory and valuations remain attractive. We remain exposed to selective high-value transport names and utilities undergoing transformative power and water/sanitation investment.

Brazil is a key country to watch regarding El Niño, which historically brings high rainfall and flooding in the South and severe drought in the North – constructive for electric utilities given the resulting demand growth. The agricultural sector is more two-sided: a lower global yield could benefit export markets and rail/road transporters, though severe crop losses would hurt volumes broadly. Given Brazil's importance in global soybean and corn supply, any impacts carry wider economic and food-security implications. The base case remains record 2026/27 crop levels, but this is something we are monitoring closely.

Elsewhere in Latin America, we remain constructive on the Mexican airport space despite a difficult start to the year, with passengers weaker than expected due to slower Pratt & Whitney aircraft returns, cartel violence, Trump immigration policies and record sargassum disrupting tourism. We see these impacts as short-term, with a robust longer-term demand outlook, supportive regulatory environment and attractive valuations.

Conclusion

The first half of 2026 has been a reminder that infrastructure's old 'bond proxy' label was never the full story. Today, the portfolio remains diversified across geographies and sectors, with a heavy bias to quality – strong balance sheets, superior management teams, and companies actively capitalising on the long-term growth thematics supporting the asset class for decades to come.

In an environment of resurgent inflation and higher-for-longer rates, we continue to favour User Pay assets geared to GDP growth and inflation pass-through, and real rate utilities (Europe & Brazil) that are more demand-immune but pass through inflation and rates. We retain select high quality US utility exposure to capture the AI driven investment super-cycle, while recognising that this thesis carries execution, financing and affordability risk if growth disappoints or rates stay elevated for longer.

We remain acutely aware of in-country cyclical and geopolitical risk and are actively managing the portfolio to protect and capitalise as conditions evolve. Should the Middle East stabilise further and the current fragile equilibrium hold, we would expect broad-based support for the infrastructure asset class as a whole. Should it not, active management of the User Pay/Regulated Utility and real/nominal rate splits remains our primary tool for navigating the divergence.

Download the full article below.

The content contained in this article represents the opinions of the authors. The authors may hold either long or short positions in securities of various companies discussed in the article. This commentary in no way constitutes a solicitation of business or investment advice. It is intended solely as an avenue for the authors to express their personal views on investing and for the entertainment of the reader.