4D Infrastructure is a boutique asset manager investing in listed infrastructure companies across all four corners of the globe. It was established in April 2015 by principals Sarah Shaw and Greg Goodsell in partnership with Bennelong Funds Management, and the team now manages the 4D Global Infrastructure Fund and the 4D Emerging Markets Infrastructure Fund. Their aim is to identify quality infrastructure companies trading at or below fair value with sustainable, growing earnings combined with sustainable, growing dividends.

The COVID-19 pandemic has presented challenges the likes of which individuals, businesses and governments have never experienced before. The impact of this was to push an otherwise pretty robust global economy into recession, force lockdowns and create social dislocation on a previously unimaginable scale.

Despite these 2020 challenges, we remain optimistic about both the global economic outlook and the infrastructure asset class for 2021 and beyond. Infrastructure, in all its forms, will be integral to the economic recovery and returning society to ‘situation normal’. We’ve said it before – there is no global growth recovery without roads, railways, pipelines, power transmission networks, communication infrastructure, ports and airports.

Just what is infrastructure?

Infrastructure provides basic services essential for communities to function and for economies to prosper and grow. For us at 4D, this equates to the publicly listed owners and operators of essential services (regulated utilities in gas, power and water); and user pay assets (toll roads, airports, ports, rail where a user pays for the service).

These assets are characterised by:

- monopolistic market positions, or ones with high barriers to entry;

- returns underpinned by regulation or contract;

- a largely fixed operating cost base;

- high up-front capital costs and then very low ongoing maintenance spend; and

- inflation hedges within the business.

These characteristics together provide long-term, resilient and visible cash flows which underpin a yield or potential yield.It is because of these characteristics that infrastructure is known as a ‘defensive asset class’, with generally lower volatility of earnings and higher yields than broader equities. It is these attributes that attract investors, including ourselves, to the asset class.

Why we’re so optimistic

Listed infrastructure is an equity, and can be caught up in market volatility (as we saw in March 2020). But this market volatility can also present significant opportunity for investors to capitalise on the long-term infrastructure thematic (that is, defensive characteristics with structural growth), and we believe that time is now.

COVID-19 vaccines: a demonstration of human ingenuity in a crisis

Since early in 2020, some of the world’s best and brightest medical research minds have been focused on developing vaccines.

In an endorsement of how creative humankind can be in a crisis, a number of vaccines were developed in record time and are being deployed across the world. This is truly remarkable, and should see the virus gradually tamed. As CSL CEO Paul Perreault said recently: ‘Often a crisis breeds trailblazers and ingenuity, and the acceleration of solutions to treat and prevent COVID-19 has been truly inspirational’[1].

Stimulus will continue to propel global economic growth

We believe the global economy will ultimately emerge stronger for this experience, with the huge amount of fiscal and monetary stimulus still to be fully felt in economic terms. All this investment will be a strong positive for the global economy over coming years, improving efficiency, productivity and output. In addition, we believe many of the operational changes that have been forced on businesses by the pandemic will lead to a stronger, more efficient economic environment post the virus.

A substantial percentage of this fiscal spending is focused on infrastructure reinvestment and replacement. Industry participants suggest that for every $1 of infrastructure investment, an economy gets a boost of anywhere between $3-$5. That’s a significant economic boost as a result of the infrastructure investment dynamic.

Increased public sector infrastructure spending is a clear positive for the listed infrastructure sector, as it:

- boosts economic growth and labour efficiency, which is good for all businesses but especially those infrastructure businesses which form the ‘arteries’ of an economy;

- creates potential new opportunities for the private sector to co-invest alongside government or invest in place of governments; and

- on a longer-term basis, potentially provides a bigger pool of privatisation candidates.

The long-term structural opportunity remains intact

Infrastructure offers defensiveness with economic diversity. These attributes, coupled with a significant growth pipeline, create a very attractive long-term thematic for the sector despite the near-term concerns of COVID-19. There is a huge and growing need for infrastructure investment globally, as a result of decades of underspend and the changing dynamics of the global population.

Replacement infrastructure spend

There has been a chronic underspend on critical infrastructure in virtually every nation over the past 30 years, if not longer. This has largely been due to governments having other spending priorities. For example, during the GFC the priority was saving the global banking system – not replacing water mains. During COVID-19 governments have prioritised social support – not road repairs.

Population growth & environmental considerations

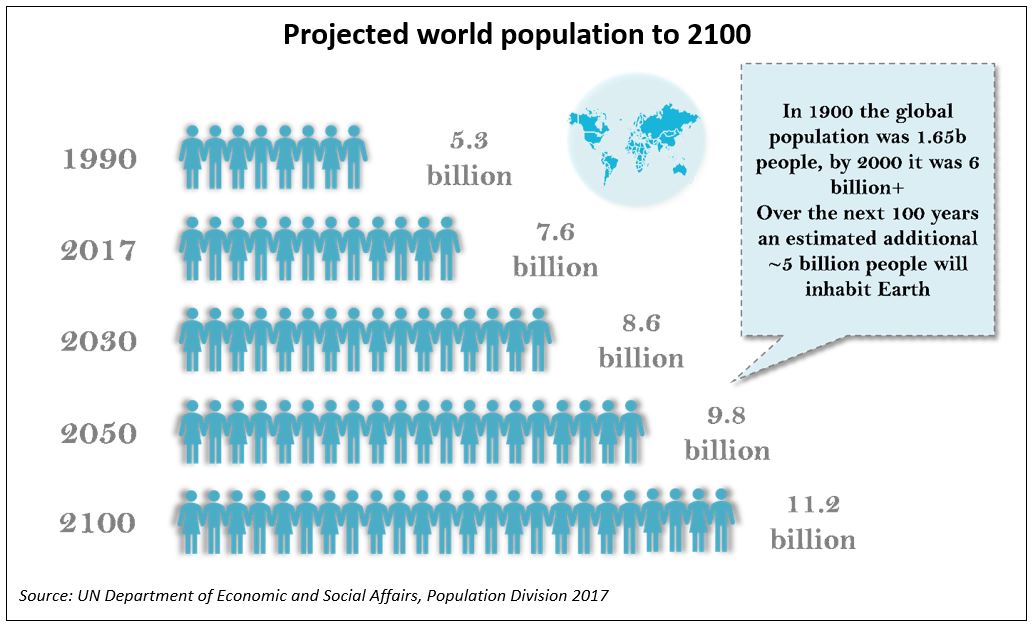

The second driver of the need for infrastructure investment is population growth. In 1900 the global population was approximately 1.65 billion people, and by 2000 that number had grown to almost 6.1 billion – keeping in mind that some of the infrastructure we are still using today was built to service that 1.65 billion. By the turn of the next century, the global population is expected to be over 11 billion, underpinning the need for yet more spend. As a society we need to first play catch-up, and then invest for the future generations.

This population growth has also raised a number of environmental and climatic challenges that underpin the need for even more spend on infrastructure to ensure the sustainability of the planet. Infrastructure investment is core to the climate solution; and without significantly increased investment in infrastructure, the globe has no chance of reaching the Paris Agreement goal of Net Zero carbon by 2050. While the speed of ultimate decarbonisation remains unclear, there appears to be a real opportunity for multi-decade investment as every country moves towards a cleaner environment. Energy transition and decarbonisation of the power sector is an obvious thematic and will have the greatest impact on countries looking for Net Zero. However, other forms of infrastructure, namely transportation, also have a key role to play.

Demographic trends support infrastructure investment

Longer-term global demographic trends further support the infrastructure asset class and the need for investment. The emergence of the middle class, particularly in emerging markets (EMs), is a theme we believe will provide enormous opportunity for investors. Given the potential size of the middle class in EMs (China, India and Indonesia alone account for 40% of the global population), changes in spending and consumption patterns will have significant implications for global business opportunities and investment for decades to come.

Importantly, one of the clear and early winners of the emergence of the middle class is infrastructure, which is needed to support the evolution.

Current investment opportunities are attractive

As an equity asset class, listed infrastructure wasn’t immune to the COVID-19 market selloff – and as yet, hasn’t fully participated in the subsequent cyclical market bounce. We believe this has created a very attractive and unique investment opportunity in global listed infrastructure.

Separating the equity market moves from the investment fundamentals, the earnings of the asset class have proven to be far more resilient than the share price sell-off implies. Through a tumultuous 2020, the asset class has proven its defensive characteristics with solid earnings momentum underpinned by strong balance sheets. This is a significant disconnect – and we believe it’s only a matter of time before the market recognises the infrastructure opportunity.

So, what does support the investment thesis in the current environment?

The key to success

Firstly, infrastructure comprises two quite distinct and economically diverse subsectors. Essential services are the regulated utilities in the power, gas and water space, and are largely immune to economic shifts (up or down) as a function of them being a basic need. They are more immediately adversely impacted by rising interest rates/inflation and are slower to realise the benefits of economic growth – and at the same time, are less exposed to economic contraction and benefit from lower interest rates. These assets are attractive overweight portfolio positions in depressed economic environments as they can offer earnings growth and yield support. In contrast, user pay assets such as airports, toll roads, rails and ports are positively correlated to GDP growth and inflation. These stocks capture GDP growth via volumes, but with inflation protection through their tariffs. As such, these assets are well suited to growth environments or the recovery phase of an economic cycle.

Secondly, infrastructure investment also offers geographic diversity. This allows investors to capitalise on in-country domestic demand, in-country stimulus and position accordingly.

Finally, as discussed above the structural infrastructure growth opportunity remains intact. The advent of COVID-19 hasn’t changed this dynamic. We believe the long-term infrastructure investment themes have actually been enhanced by the current pandemic – government stimulus programs are fast-tracking infrastructure investment, increasingly stretched government balance sheets will see a greater reliance on private sector capital, and a ‘lower for longer’ interest rate environment is supportive of infrastructure investment and valuations.

Meanwhile, solid well-managed infrastructure companies are in robust financial positions. Balance sheets were in strong starting positions, and few have reported any liquidity issues as a result of COVID-19. Management teams are also taking advantage of open credit markets and low market interest rates to secure attractive, long-dated debt financing to ensure ongoing liquidity and support growth profiles. Despite near-term uncertainty around economics and the duration of the pandemic, the underlying fundamentals of these assets remain attractive to debt investors, which should go some way to reassuring equity investors.

We believe the combination of attractive investment fundamentals, long-term structural thematics that remain intact, the COVID-19 response and currently very attractive stock prices represents a unique buying opportunity for listed infrastructure – an opportunity we are looking to capitalise on as we move into the economic recovery phase.

[1] Australian Financial Review, ‘We are more resilient and adaptable than we ever imagined’, 18 Dec 2020

Like this article? Want to know more?

- Subscribe to receive our regular insights

- Learn about our funds and how to invest

- Get in touch for more information